"Approach alternative investments with care")

Unlike the wealthy, retail (individual) investors have limited options to invest in high-risk, high-return alternative instruments. The ticket size of such products — private equity, exclusive wines and paintings — are too high for small investors. But, in recent times, more avenues have opened that allow retail investors to make risky bets in assets other than stocks.

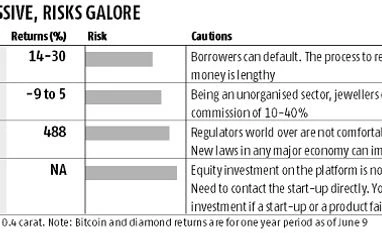

For example, bitcoins is one such asset that younger investors are looking at. The price of this virtual currency has gone up from $579.13 a year back to $2,825.03 — a return of 488 per cent. “Increasingly, millennials are getting attracted to bitcoin because of high returns. They also like the fact that it’s a global, transferable virtual currency and beyond the control of any government or institution,” says Saurabh Agrawal, co-founder of ZebPay, an app-enabled bitcoin wallet provider.

When investing on such non-traditional avenues, investors tend to only look at the returns. They also need to realise these are riskier than traditional instruments such as equity. They should only put in investible surplus or up to three to five per cent of the portfolio in these, as they are volatile and can significantly erode the capital.

Peer-to-peer lending: Tarun Arora, 41, had started by lending on peer-to-peer (P2P) lending platforms around one-and-a-half year ago. The lure was the prospect of 18-20 per cent returns when bank fixed deposits offered eight per cent. “I knew if I lend on a P2P platform, the borrower could default. I, therefore, started small and with few investments,” says Arora, who works with a bank. He has given loans to around 80 borrowers with an average size of Rs 20,000 each. The average return on his portfolio is 28 per cent.

He says many investors equate P2P lending with fixed deposits. That isn’t the case. Defaults can happen despite taking precaution to get borrowers only who have repayment capabilities. Faircent selects around 1,000 borrowers a month from the 20,000 applications it receives. “If you have Rs 1 lakh to invest, spread it across 20-30 borrowers. Lenders should build a portfolio over time,” says Gandhi. Study the borrower’s profile and how they use your money before lending. “If I have to choose between a person borrowing money for credit card settlement and another taking a loan for home improvement, I would go for the latter. I also prefer married individuals with kids over singles, as I think they would be more responsible,” says Arora.

Precious stones: The market for diamonds is still largely unorganised, but sellers are becoming more transparent about the pricing and quality. Investors can now compare prices on the internet based on different features and take a more informed call.

To boost buyer confidence, companies such as Divine Solitaires have started their price index which publishes diamond rates every month. If a buyer wants to resell, the company claims the jeweller must give at least 90 per cent of the value shown in the index. If the jeweller will not, the buyer can approach the company directly. The prices of diamonds fluctuate. They can rise 10-15 per cent in a month or remain stable for a year. “For investments, don’t opt for the highest quality of diamonds. Instead, opt for medium quality and that are between 0.3 and 0.8 carats. There are chances of making higher returns in medium-quality diamonds,” says Jignesh Mehta, managing director, Divine Solitaires. The price of a diamond depends on colour, clarity, cut and carat weight. The quality of colour ranges between D (best) and K (low) and clarity has six parameters — IF, VVS1, VVS2, VS1, VS2, SI1 and SI2 in descending order of quality.

After a person purchases a diamond, ensure the serial number in the certificate is also inscribed. A buyer should not compromise on certification and opt for one that charges a lower fee.

Crowdfunding platforms: You cannot directly expect returns if you make a “donation” in a campaign. “Regulations don’t allow us to run campaigns where a company or an individual promise any returns,” says Varun Sheth, chief executive officer and founder of Ketto.org. Increasingly, investors are looking at campaigns on crowdfunding websites and approaching start-ups directly to buy an equity stake.

Investors approached Leaf Wearables after seeing a product campaign on a crowdfunding platform. It needed Rs 1.5 crore for a jewellery that had a women safety feature built into it. “Investors saw the product on the crowdfunding website. It was quite successful as donors had shown high interest. Some approached us directly and invested a few lakhs,” says Paras Batra, co-founder, Leaf Wearables.

Investors get to own a very small stake in the company and have no say in decision-making. If the company or the product is successful, the returns are manifold. But, only one among thousands is able to sustain their business over the long term and make profits. Sometimes, a start-up could fail or the product doesn’t see the light of the day. In such events, investors lose all their money.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in