"Citibank launches home loan product linked to an external benchmark")

Citibank has launched a home loan product linked to an external benchmark. The development assumes significance in the light of the Reserve Bank of India (RBI) appointed Janak Raj Committee's recommendation last year that all banks should link their loans to an external benchmark. While Citi's new home loan is a very transparent product, customers opting for it also need to be prepared for frequent changes in their tenure or EMI.

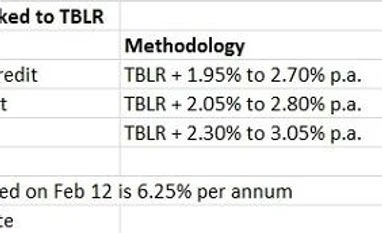

Citibank's new home loan will be benchmarked to the three-month treasury-bill rate. The benchmark is called treasury-bill benchmark linked lending rate (TBLR). It will be provided by Financial Benchmarks India Private Limited (FBIL), an independent benchmark administrator recognised by the RBI. Home loan rates will be reset once every quarter on the first of March, June, September, and December. The three-month T-bill rate on a specific date of the month will be used as the benchmark: the bank has mentioned the 12th on its website.

The current TBLR is 6.25 per cent. The spread charged above the benchmark rate will remain constant throughout the loan tenure. Customers who are currently on the MCLR or base rate can shift to the TBLR-based home loan without any charge.

According to experts, Citi's product will bring in much-needed transparency into home loans. The Janak Raj committee report had pulled up banks for arbitrariness in calculating the base rate and the MCLR. The panel had also found problems with the way banks calculate the spread over the MCLR. When the MCLR was falling, banks would increase the spread to reduce the pass-through to customers. A product like this will take care of such issues. Manipulating the benchmark will not be possible since it is linked to a publicly published rate put out by an independent entity.

"The treasury bill linked home loan is in line with global best practices, local and regulatory expectations on the use of external benchmarks, and also offers clients a better experience," says Shinjini Kumar, country business manager, global consumer banking, Citi India. Independent experts said that the spread remaining constant throughout the loan tenure is another sign of transparency. According to experts, the current interest rates being offered by Citi are also competitive (see table).

The flip side that customers need to watch out for is that their home loan rate will change more frequently (every quarter), than when it was reset every six months or every year.

Borrowers will need to track interest rates closely. "Most people take a home loan based on the EMI they can service today. They don't factor in what it will be in nine months or a year. With a product like this, they will have to borrow conservatively, especially now, when rates appear to be headed upward," says Arvind A Rao, financial planner and founder, Arvind Rao and Associates.

For young borrowers, a more volatile rate may make less of a difference since the bank is likely to increase their loan tenure. Over a 20-year span, the upward and downward movement of interest rate could well even out. But in case of borrowers close to retirement, banks don't extend the tenure beyond the retirement date. Instead, they hike their EMI. Such borrowers will need to be more cautious. Furthermore, when interest rates begin to move upward, they can keep on rising for two-three years and by as much as 2.5-3 percentage points. Borrowers should factor in that kind of rise when deciding on their loan amount.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in