"Don't let this festival season get taxing for you")

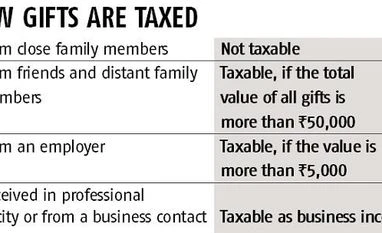

If you have a generous employer like Savji Dholakia, the Surat-based billionaire diamond merchant famous for gifting flats and cars to his employees on Diwali, it could get taxing while filing returns next year. Employees need to pay tax on any gifts received from an employer that has a market value of over Rs 5,000.

“Such gifts are added to income from other sources. The employer deducts tax at source based on the applicable tax slab and deposits it with the income tax department. If the value of the house is Rs 50 lakh, the receiver needs to pay Rs 15 lakh as tax,” says Chetan Chandak, head of tax research, H&R Block India

But if a salaried receives a mobile phone, a tablet or any other gadget that is a trendy gift at present from a vendor or client or business contact, he doesn’t need to pay tax on those. The income tax department has specified the gifts that attract tax if they are not from a close relative.

These include immovable property, shares and securities, jewellery, archaeological collections, drawings, paintings, sculptures, or any work of art.

For those in business or engaged as a professional, taxation of gifts is treated differently. “Any gift they receive is considered as business income,” says Naveen Wadhwa, general manager, Taxmann.com. In this case, gifts are considered as professional receipts or compensation over and above the money paid for the services rendered. These should be added to the income and taxed according to the slab.

Section 28 of the Income-Tax Act lays down what is taxed as business income and includes “the value of any benefit or perquisite, whether convertible into money or not, arising from business or the exercise of a profession”. The receiver of such gifts needs to find their market value before declaring them to the tax department.

If the donor is a friend and the gift is received in personal capacity, taxation changes again. Gifts from personal contacts or distant relatives are exempt from tax up to Rs 50,000. The Income-Tax Act lists 10 gifts that need to be declared and the receiver needs to pay tax on these if given in personal capacity. These include cash, bullion, jewellery, shares, financial securities, drawing, paintings and immovable property. These have to be declared under the head ‘income from other sources’ and taxed accordingly.

You also don’t need to pay tax on gifts received from close relatives, irrespective of their value. Close relatives mean immediate family including parents, siblings, spouse and children. Also, spouse’s parents. Gifts from brother’s or sister’s spouse are exempted. If an individual receives a gift from parent’s siblings, it’s not taxable either. “One should be careful of the definition of a close relative as it can get confusing. A gift received by nephew from his uncle is not taxable but it can be vice versa,” says Wadhwa.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in