"Govt guarantees 8.30% to seniors for 10 years")

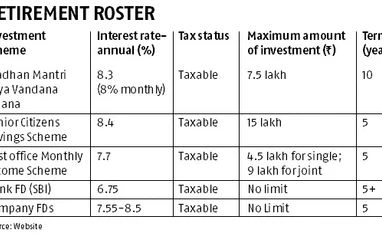

The newly launched Pradhan Mantri Vaya Vandana Yojana (PMVVY) ticks many of the boxes that investors seek in a pension product. It offers a guaranteed return of 8 per cent monthly (effective rate of 8.30 per cent annually) for 10 years. But, the maximum investment limit of Rs 7.5 lakh will prove grossly inadequate for most middle-and upper-class senior citizens. Hence, financial planners suggest it should be used by them in combination with other income-yielding products.

The effective guaranteed return of 8.30 per cent for 10 years is the biggest advantage of the scheme, given that interest rates could decline over the long term. But the investment limit of Rs 7.5 lakh is applicable for an entire family, comprising the pensioner, spouse and dependents. In comparison, the Post Office Senior Citizens Saving Scheme (POSCSS) has a limit of Rs 15 lakh. So a retired couple can in aggregate invest Rs 30 lakh in it. The POSCSS offers 8.4 per cent interest, currently. But the rate is subject to a reset every quarter and could come down in future. “One advantage of the POSCSS is that you get tax deduction benefit under Section 80C at the time of investment, which PMVVY does not offer. So, pensioners should first utilise the limit under the POSCSS and then invest in PMVVY,’’ says Steven Fernandes, a Mumbai-based certified financial planner.

The income from the PMVVY is not exempt from income tax. However, the maximum monthly interest income possible from it is Rs 5,000 (Rs 60,000 annually). Being taxable, it is better suited for people who don't have any taxable income or are in the lowest tax bracket. “This scheme is suitable for those in the lowest income bracket and for those who want an income payout. It is not targeted at those looking to create a corpus," says Riddhi Agarwal, vice-president, My Financial Advisor.

Ideally, a senior citizen planning for income after retirement should look at a bouquet of investment products. "The combination of instruments you choose should offer different features, which include fixed benefits, market-linked returns, liquidity, etc.," points out financial planner Gaurav Mashruwala. “The PMVVY on its own will not suffice. The maximum monthly pension is low. However, it has a few other benefits like you can take a loan against it, it offers some liquidity, and it also offers the return of purchase price,’’ he says. Adds Manoj Nagpal, chief executive officer, Outlook Asia Capital: "At a time when a corporate fixed deposit with AA rating is offering around 8.5 per cent, this scheme offers the government-guaranteed annual return of 8.30 per cent. So, pensioners should definitely take advantage of it to the extent possible.”

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in