"Health insurance policy: Don't include parents in family floater plans")

Some companies have started offering family floater health insurance plans that allow individuals to include their parents in the same policy. While such policies offer the convenience of paying a single premium for the entire family, buying a separate family floater policy for parents is more cost-effective.

An individual should only include parents in a family floater if they are unable to get a separate policy. “If seniors apply for health insurance on their own, their chance of getting a cover is limited, especially if they have pre-existing diseases. In a family floater plan, their chances of getting a cover improve,” says Arvind Laddha, deputy chief executive officer, JLT Independent Insurance Brokers.

Max Bupa and Aditya Birla Health Insurance offer this option. “In the Max Bupa Heartbeat Family First plan, a person can cover up to 20 relationships in a single policy. There is no age cap for any relationship,” says Ashish Mehrotra, managing director and chief executive officer, Max Bupa Health Insurance.

In Aditya Birla Health’s plan, customers earn points for keeping fit. These can be used for health-related expenses such as paying for diagnostic tests, day care treatment, outpatient expenses, alternative treatments (traditionally excluded), or even to pay for future premiums.

Including parents is expensive: A family floater plan's premium is usually based on the age of the oldest family member. Adding parents would mean an individual pays higher premium for a lower sum insured. “It, therefore, makes more sense to opt for two family floater policies — one for the parents and the other one for the son and his family,” says Rahul Mohata, chief operating officer, 121policy.com.

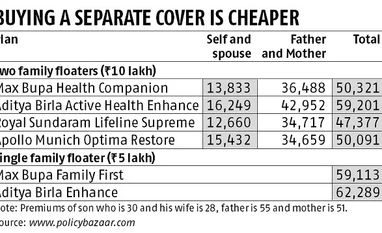

Consider a family of four. The son, who is taking the insurance, is aged 30. His wife is 28. Mother and father are 51 and 55, respectively. For a Rs 5-lakh family floater of Max Bupa Family First, the premium is Rs 59,113, and for Aditya Birla Health Insurance Enhance, it is Rs 62,289. These are the premiums considering everyone is healthy.

If you were to buy separate plans for the parents and for the son and his wife, you would get double the sum insured for almost the same price. If the individual opts for Max Bupa Health Companion and buys two separate family floaters with a cover of Rs 10 lakh each, the total premium for the same profile would be Rs 50,321. Similarly, for Aditya Birla Health Insurance Active Health Enhance, the total premium for the two plans would come to Rs 59,201. As these plans are different from those where parents are included, some features would differ.

If you consider the earlier example, you can get Rs 40-lakh cover in two separate family floater plans, helping you to keep pace with medical inflation. In the same example, if the plans that allow you to include parents also offer restoration benefit, for the same premium you will only get a cover of Rs 10 lakh.

Problems of including parents: If you take a family floater that gives the option of including your parents, they may be required to undergo pre-policy medical check-ups. Depending on the results, an insurer could even reject your application or put special conditions. If there’s a loading due to illness, the premium will rise.

Also, insurance companies offer no-claims bonus (NCB) if the customer does not file a claim. You get a discount on next year's premium. If you include your parents, there is a possibility of frequent hospitalisation, and you will lose out on the NCB. In two separate family floaters, at least your policy will be eligible for an NCB, even if your parents’ is not.

You can, however, make full use of the income tax deduction under Section 80D, even if you buy a family floater that has parents. The income tax law offers a deduction of up to Rs 25,000 on premium paid for self, spouse, and children. Also, there’s a deduction of up to Rs 30,000 if you pay premiums for parents who are above the age of 60. “There are no separate fields for self and parents in the ITR forms. A person cannot bifurcate the premium. The total premium paid towards health insurance policy, including expenses towards preventive health check for self and parents can be an input in a single field provided to claim a deduction,” says a spokesperson of Aditya Birla Health Company.

When to include: There are times when insurance companies might not be willing to give a policy to your parents if they suffer from pre-existing illness. However, an insurance company may agree to insure one or two cases it feels are risky if they come with healthy individuals. Family floater policies that allow inclusion of parents are designed to consider such cases. “At Max Bupa, we believe in easing those approaching their senior years from their worries of being devoid of health insurance cover when it is most required. We understand the importance of providing the elderly with affordable yet quality health care solutions,” says Mehrotra of Max Bupa.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in