"Life insurance players clocking strong growth in protection policies")

The June quarter (Q1) results of HDFC Life, ICICI Prudential Life Insurance Company, Max Financial Services and SBI Life indicate these four major listed life insurance players are focusing on protection products, which provides impetus to their profitability. From a stock perspective, too, analysts see gains for most of these companies.

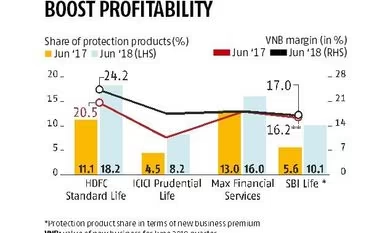

Life insurers’ profitability is measured in terms of value of new business (VNB) margin, which is VNB as a percentage of the present value of future premium. Protection products are seen as more profitable. The value of new business margin at HDFC Life and ICICI Life expanded 370 bps and 680 bps, respectively, over a year. While the metric for Max inched up 10 bps, the gains were restricted on account of high cost overrun due to sales seasonality and investment in the proprietary channel. Though the June 2017 quarter margin figure is not available for SBI Life, its margin in Q1 of FY19 rose 80 bps, as compared to FY18.

Except SBI Life, the other three, on a year-on-year basis, reported 300-710 bps expansion in the share of high-margin protection products, in terms of annualised premium equivalent or APE (see graph). APE is the measure of ascertaining business sales in the life insurance industry. SBI Life’s protection share, in terms of APE, is not truly comparable due to change in product structure. But, in terms of new business premium (NBP), its share of protection products moved up 454 bps over a year to 10.1 per cent.

The firms are likely to sustain focus on growing the proportion of protection products in overall sales. “We’ll continue to strive for pushing the protection business in each of our channels in an aggressive way,” HDFC Life’s management said after the June quarter results. The management believes growth opportunity in the protection space is very large.

“Lower penetration of protection products and highest margin would create upward thrust for such products,” says an analyst with a domestic brokerage. Protection products should grow 30-33 per cent annually, the analyst said. Such a trend would help improve margins, despite expectations of slower increase in APE.

Though migration of household savings to financial assets augur well for insurance firms, APE growth of many private ones, as observed in Q1, might grow at a slower pace, thanks to high base of last year. Yet, this is perceived as healthy as after demonetisation, people had invested in insurance products in the past financial year.

“The sector will continue to grow, albeit at a slower pace, mainly due to the high base. Though growth of Ulips (unit-lined insurance products), which depend upon the markets’ movement and that of savings products could get tepid, share of protection products would continue to rise, improving earnings potential of the sector,” says Avinash Singh, analyst at SBICAP Securities.

Further, profitability would get support if persistency ratio in the 61st-month bucket improves. This ratio is the percentage of policies renewed after a specific period (bucket), such as after one year or three years, etc, thus reflecting customer stickiness. The persistency ratio for most of these companies improved in Q1, barring this cohort. Thus, how the 61-month persistency plays out would be interesting to watch, as it is quite challenging, say an analysts.

In this backdrop, analysts expect 31-43 per cent upside in these stocks, except for HDFC Life, due to an already high valuation (4.3 times the FY20 expected embedded value versus 1.7-2.5 times for peers), over the next year, and believe it offers good opportunity for long-term investors.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in