"Made an error? File your revised tax returns within stipulated timeline")

Taxpayers are typically cautious and exercise due care while filing income tax (I-T) returns. But very often, in the rush to meet deadlines, many of them end up making errors. Some of these include not claiming deductions, not reporting losses, incorrect or total lack of reporting of income. These mistakes could occur due to lack of knowledge of the provisions of tax laws or due to lack of accurate information at the time of filing the original return. Lawmakers are mindful of such situations and, hence, have made provisions for an opportunity to file a revised return, in case an omission or wrong statement is discovered after filing of the original tax return. However, this task must be completed within a specific time frame.

Timelines are crucial

The first point that the taxpayer must remember is that if he changes the income declared, the tax officer could levy additional tax and interest on it. Any additional tax liability on account of change in income reported or change in tax deducted at source (TDS) would attract penal interest on account of delay in payment of such additional taxes. A tax return can be revised any number of times, as long as there is no wilful concealment of income by the taxpayer and is filed within the prescribed time limit.

The time frame available to an individual taxpayer for filing revised tax returns is crucial. The tax law has been changed in recent times regarding the timeline for filing revised returns for assessment year (AY) 2016-17, which is, financial year 2015-16 (FY) and onwards.

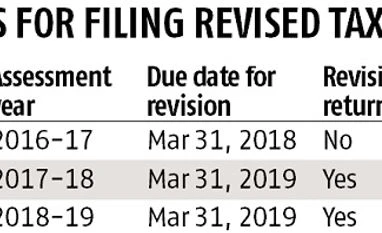

For FY 2015-16 (AY 2016-17) and FY 2016-17 (AY 2017-18), revised return can be filed before the end of one year from the end of the relevant assessment year or before the completion of the assessment, whichever is earlier. In other words, for FY 2015-16, the deadline is March 31, 2018, and for FY 2016-17, it is March 31, 2019. The point of difference here lies in the revision of the return filed after the due date (belated return). For FY 2015-16, a belated return cannot be revised. But for FY 2016-17, a belated return can be revised at any time before March 31, 2019.

For FY 2017-18 (AY 2018-19), revised return can be filed before the end of the relevant assessment year or before the completion of assessment, whichever is earlier - the last date to file the revised return will be March 31, 2019. A belated return for FY 2017-18 can be revised at any time before March 31, 2019 (see table for the summary of timelines for filing revised tax return for different years).

Timelines are crucial

The first point that the taxpayer must remember is that if he changes the income declared, the tax officer could levy additional tax and interest on it. Any additional tax liability on account of change in income reported or change in tax deducted at source (TDS) would attract penal interest on account of delay in payment of such additional taxes. A tax return can be revised any number of times, as long as there is no wilful concealment of income by the taxpayer and is filed within the prescribed time limit.

The time frame available to an individual taxpayer for filing revised tax returns is crucial. The tax law has been changed in recent times regarding the timeline for filing revised returns for assessment year (AY) 2016-17, which is, financial year 2015-16 (FY) and onwards.

For FY 2015-16 (AY 2016-17) and FY 2016-17 (AY 2017-18), revised return can be filed before the end of one year from the end of the relevant assessment year or before the completion of the assessment, whichever is earlier. In other words, for FY 2015-16, the deadline is March 31, 2018, and for FY 2016-17, it is March 31, 2019. The point of difference here lies in the revision of the return filed after the due date (belated return). For FY 2015-16, a belated return cannot be revised. But for FY 2016-17, a belated return can be revised at any time before March 31, 2019.

For FY 2017-18 (AY 2018-19), revised return can be filed before the end of the relevant assessment year or before the completion of assessment, whichever is earlier - the last date to file the revised return will be March 31, 2019. A belated return for FY 2017-18 can be revised at any time before March 31, 2019 (see table for the summary of timelines for filing revised tax return for different years).

As can be seen, for FY 2015-16, the taxpayer can file a revised return by March 31, 2018. For FY 2016-17 and FY 2017-18, he will have to file by March 31, 2019. Revision of belated return is not permissible for FY 2015-16, whereas the same can be done from FY 2016-17 onwards.

To illustrate, ‘A’ filed his original tax return for the FY 2015–16 on July 20, 2016, ie, within the due date (July 31, 2016). Later on, while going through his banking records he realised that he had inadvertently missed reporting interest income from a fixed deposit. In this scenario, since his tax return was filed within the due date, ‘A’ has the option to rectify the aforesaid error by filing a revised tax return on or before March 31, 2018. If he hadn’t filed his original return within the due date, he would have lost the right to revise his return.

For FY 2016-2017, if ‘A’ files his original tax return on August 10, 2017, which is after the due date (July 31, 2017), he will still be entitled to revise his tax return on or before March 31, 2019, since the law has been amended to allow revision of a belated return for that year. Therefore, from FY 2016–17 even if the tax return is filed after the designated due date, one has the option to revise his tax return as per the earlier mentioned timelines for the respective financial year.

Challenges for expatriate employees

With the change in the timeline for revision of tax returns, expatriate employees will face several challenges while claiming tax credit for taxes paid in overseas country. One, the reduction in time limit for revising the tax return may deny the benefit of such relief, especially where overseas tax returns are not filed or are not available by the end of the time lines as discussed in the above table. Two, filing of Form 67 will also be a challenge in the absence of documentation substantiating the claim of such relief.

These challenges are elaborated with an example. ‘A’, an Indian citizen, goes on an assignment to the US on December 1, 2017 and his residential status for FY 2017–2018 in India is Resident and Ordinarily Resident. Hence his global income is chargeable to tax in India for the aforesaid financial year.

He files his original return on the basis of his income information available before the due date, which is July 31, 2018. The return can be revised up to March 31, 2019. In order to offer his actual US income and claim the credit of the US taxes on the same in his India tax return, he requires his US return for the year 2017 and 2018.

Since the US follows the calendar year and has a due date of April 15 for filing the return, which can also be extended, it is unlikely that his US return for the year 2018 would be available before March 31, 2019. Therefore, A will be unable to claim the accurate or complete credit of foreign taxes for the year 2018 by the due date of March 31, 2019. Given the above challenge, one will have to wait and watch if the government provides any relief for this class of individuals.

While it is always better to be cautious and have all information available so that accurate details are reported while filing tax returns, one can still avail the opportunity provided by law to rectify mistakes in the tax return.

To illustrate, ‘A’ filed his original tax return for the FY 2015–16 on July 20, 2016, ie, within the due date (July 31, 2016). Later on, while going through his banking records he realised that he had inadvertently missed reporting interest income from a fixed deposit. In this scenario, since his tax return was filed within the due date, ‘A’ has the option to rectify the aforesaid error by filing a revised tax return on or before March 31, 2018. If he hadn’t filed his original return within the due date, he would have lost the right to revise his return.

For FY 2016-2017, if ‘A’ files his original tax return on August 10, 2017, which is after the due date (July 31, 2017), he will still be entitled to revise his tax return on or before March 31, 2019, since the law has been amended to allow revision of a belated return for that year. Therefore, from FY 2016–17 even if the tax return is filed after the designated due date, one has the option to revise his tax return as per the earlier mentioned timelines for the respective financial year.

Challenges for expatriate employees

With the change in the timeline for revision of tax returns, expatriate employees will face several challenges while claiming tax credit for taxes paid in overseas country. One, the reduction in time limit for revising the tax return may deny the benefit of such relief, especially where overseas tax returns are not filed or are not available by the end of the time lines as discussed in the above table. Two, filing of Form 67 will also be a challenge in the absence of documentation substantiating the claim of such relief.

These challenges are elaborated with an example. ‘A’, an Indian citizen, goes on an assignment to the US on December 1, 2017 and his residential status for FY 2017–2018 in India is Resident and Ordinarily Resident. Hence his global income is chargeable to tax in India for the aforesaid financial year.

He files his original return on the basis of his income information available before the due date, which is July 31, 2018. The return can be revised up to March 31, 2019. In order to offer his actual US income and claim the credit of the US taxes on the same in his India tax return, he requires his US return for the year 2017 and 2018.

Since the US follows the calendar year and has a due date of April 15 for filing the return, which can also be extended, it is unlikely that his US return for the year 2018 would be available before March 31, 2019. Therefore, A will be unable to claim the accurate or complete credit of foreign taxes for the year 2018 by the due date of March 31, 2019. Given the above challenge, one will have to wait and watch if the government provides any relief for this class of individuals.

While it is always better to be cautious and have all information available so that accurate details are reported while filing tax returns, one can still avail the opportunity provided by law to rectify mistakes in the tax return.

The writer is partner, Deloitte Haskins and Sells. The company’s Manager Bhavin Rajput and Deputy Manager Monish Satra contributed to the article

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in