"Want to be cash-ready for financial emergency? Follow these rules")

According to the Reserve Bank of India's annual report, household savings in cash have risen to a peak level of 2.8 per cent. While households must have an optimal level of cash to meet their day-to-day requirements and emergency needs, holding too much cash can be detrimental for their financial health as cash in bank or liquid funds earns a lower level of return than in other instruments like equities.

Ideally, one should have one month of expenses as cash on hand. This money in the house will help you deal with emergency situations like the recent flood in Kerala, where people had money lying in their bank accounts but could not access them, because the ATM machines and bank branches were not working. It will also prove useful in dealing with health emergencies. This money should be kept at home in a secure place, such as a locker, and the whereabouts of the key should be known to more than one person.

Households also need to maintain a contingency fund. The amount of contingency fund you maintain should depend on the structure of your family. "If you are a double-income family, you should have three months of expenses in the contingency fund. One month of expenses may be kept in cash at home and two months may be kept in a savings account or liquid funds (1+2). If you are a single-income family, you should have a 1+5 saving structure, while entrepreneurs should maintain 1+11 savings," says Vishal Dhawan, chief financial planner, Plan Ahead Wealth Advisors.

Contingency funds may be kept in liquid funds, sweep fixed deposits, and ultrashort-term funds. If you have a sweep account, you don't need to keep money in savings accounts. Money above certain levels automatically gets swept into a fixed deposit in sweep accounts. Suppose that you issue a cheque of Rs. 100,000 and the balance in your savings account is only Rs. 10,000. The rest Rs. 90,000 will be automatically pulled from your fixed deposit. From the user's perspective, it is as good as a savings account in terms of liquidity, but it gives the returns of a fixed deposit (for so long as the money is lying in the fixed deposit).

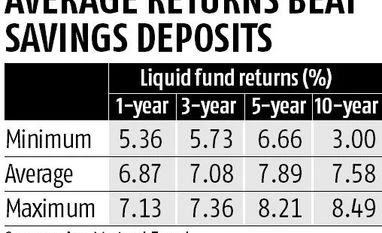

Liquid funds are another good option for keeping your contingency money. Liquid funds pay out money within 24 hours, provided you apply for redemption before the cut-off time, which is 2 PM. Invest in funds that have most of their exposure to AAA-rated paper, and A-1 rated paper. Simply going by returns will not capture the risks that the fund manager is taking. Also, look for liquid funds that have low expense ratios.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in