"Premiums may go down for good drivers, low car usage")

The insurance regulator wants to reward car owners with good driving skills. It has come up with a discussion paper on lowering premiums of those auto insurance customers who display good driving behaviour, don’t use their car often or have limited usage each day.

If the Insurance Regulatory and Development Authority of India (Irdai) implements this (the discussion paper has been put up on the website currently), a person would need to fit an on-board diagnostic (OBD) device that tracks driving behaviour, car health and usage. “The data will be relayed to your insurer in real time. Using the information, the insurance company can offer you a customised insurance,” says Gaurav Malhotra, vice-president–actuarial, Bajaj Allianz General Insurance.

Known by different names — telematics insurance, black box insurance, GPS car insurance and smart box insurance — the product is best suited for those with a second car that is not used much use or those who usually drive over the weekends with family. The less you drive, the less risky a customer you are.

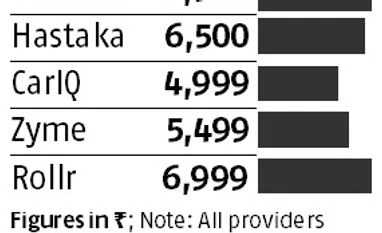

Source: Company websites

The OBD device costs around Rs 7,000 at present. But Ved says prices have been falling and if the insurance product gets the regulator’s nod, the cost of the device could come down further. To relay the information, the device needs a SIM card. There would be a running cost, too. At present there are some service providers that sell such devices with a pre-installed SIM card and charge a monthly annual subscription fee. The customer doesn’t need to bother about spending money on data recharges.

The insurers are also expected to offer additional benefits and features when a customer opts for such a telematics insurance product. Explains Tarun Mathur, co-founder and director,policybazaar.com: “The device can reduce car theft and break-ins. It can be used to immobilise vehicles remotely. An owner can also track vehicle movement. Such devices also inform you on the health of the car — whether the oil needs to be changed or if the vehicle is due for servicing and so on. During accidents, messages can be relayed from the device.” Insurers can build benefits around these.

The regulator has asked the insurance industry to suggest if alternative methods or devices, such as a mobile app, can be used as an alternative to the expensive OBD device.

The telematics device can track reckless driving by capturing parameters such as maximum and average speed, acceleration, braking, cornering, latitude and longitude, distance travelled, journey time, road type, G-force (impact detection), number of other cars on the road, weather circumstances, and so on. Such data can tell insurers the driving behaviour of the person behind the wheel and the segment under which the driver falls. Lower car usage is a sure way to get you a lower premium. But the regulator is concerned that if a good driver uses a car more often, he could end up paying a higher premium.

As the product evolves, you can also expect policies you can take for a fixed duration. Say, you have the mandatory third-party insurance. But need a comprehensive cover for a road trip. Insurers would be able to offer you a policy with a duration of as low as a fortnight.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in