"Rajiv Gandhi Equity Savings Scheme: Too complex for little rebate")

Imagine this: The rising stock market index – the Bombay Stock Exchange Sensitive Index (Sensex) at 20,000 has caught your fancy. And you want to invest in equities for tax saving for the first time. The options: Equity-linked savings schemes (ELSS) and the newly introduced Rajiv Gandhi Equity Savings Scheme (RGESS) by some mutual funds. What should you choose?

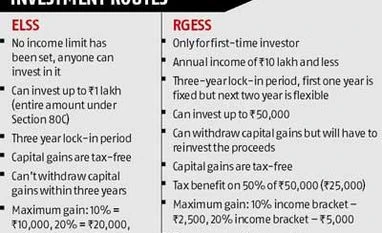

The answer is simple — ELSS —because through this option, you can save more tax. RGESS, which was launched in the Union Budget 2012-13, is getting operationalised now with some houses such as LIC-Nomura, IDBI Mutual Fund and others allowed to launch these schemes.

Under RGESS, there is a direct investment option as well for investors who wish to take that route. But given that the scheme is only meant for first-time investors, financial experts advise that it is better if one takes the mutual fund route.

The benefits under the two schemes are mutually exclusive, because one gives benefits under Section 80C and other under Section 80CCG. However, from a sheer tax-saving perspective, ELSS works out much better. Sadly, when the direct taxes code is going to be implemented, ELSS is expected to go out of the section.

“Hence, the one-time exemption defeats this purpose. It should be allowed every year like ELSS. The focus should be on channelising long-term serious money into the capital market.”

The process is also complicated. Investors will have to open a special RGESS designated account where no trades have been done before the notification. The investing options are many: You can buy shares that are in the BSE-100 or NSE 100 indices or invest in the listed shares of Navratna, Maharatna and Miniratna public-sector undertakings (PSUs). There is the initial public offering (IPO) option as well, where you can invest in PSU IPOs with turnover of more than Rs 4,000 crore. And then there are mutual funds.

Financial experts feel that if the objective is to spread equity cult, index funds of mutual funds should also be included in the options. “In fact, it will be better for new investors simply because a new investor is risk-averse and index funds cap the losses in some ways,” says a fund manager.

The maximum amount you can invest is Rs 50,000. But the tax benefit is on 50 per cent of the amount, Rs 25,000. The deduction will be, according to your slab, which will be either 10 per cent or 20 per cent (given the Rs 10 lakh income limit). So, the benefit for the person will be Rs 2,500-Rs 5,000.

This is the simple part. The complexity begins from the second year. While the scheme allows you to book profits and sell shares, the RGESS account has to be replenished with shares purchased with the proceeds. If the conditions are violated, the benefits under Section 80CCG will be withdrawn.

This is quite complicated. Because on the one hand, the scheme is getting liquidity due to the option of profit booking. But a new investor could always get into trouble if he tries to take too many decisions on his own.

“The lock-in period should be on the lines of ELSS. Why allow new investors to make changes after one year, especially when the investment universe is restricted to large cap stocks?,” asks Rustagi. Also, if someone buys more shares and does not want to them to be locked-in, he will have to declare it within a month in Form B. All these tiny additions make it complicated.

In comparison, ELSS is simpler. For one, there is no income limit that is set – anyone can invest in it. The benefits are not additional, and they come to you under Section 80C. That is a limiting factor because of the long list of instruments under this section, which includes ELSS, employee provident fund, public provident fund, life insurance premiums, pension plans of mutual funds, five-year fixed deposits, principal payment of home loans and others. So, most people end up exhausting this limit.

But if you have not exhausted the limit, benefits of investing through ELSS are significantly higher. For instance, if you invest Rs 1 lakh in this instrument, the benefit would be Rs 10,000-Rs 30,000, according to the slab.

Yes, RGESS is an option for investors who want additional tax benefits. If you really want to take advantage of this scheme, treat it like ELSS. Invest and forget for three years. Otherwise, all the tiny clauses will give you ulcers.

The answer is simple — ELSS —because through this option, you can save more tax. RGESS, which was launched in the Union Budget 2012-13, is getting operationalised now with some houses such as LIC-Nomura, IDBI Mutual Fund and others allowed to launch these schemes.

Under RGESS, there is a direct investment option as well for investors who wish to take that route. But given that the scheme is only meant for first-time investors, financial experts advise that it is better if one takes the mutual fund route.

The benefits under the two schemes are mutually exclusive, because one gives benefits under Section 80C and other under Section 80CCG. However, from a sheer tax-saving perspective, ELSS works out much better. Sadly, when the direct taxes code is going to be implemented, ELSS is expected to go out of the section.

“Hence, the one-time exemption defeats this purpose. It should be allowed every year like ELSS. The focus should be on channelising long-term serious money into the capital market.”

The process is also complicated. Investors will have to open a special RGESS designated account where no trades have been done before the notification. The investing options are many: You can buy shares that are in the BSE-100 or NSE 100 indices or invest in the listed shares of Navratna, Maharatna and Miniratna public-sector undertakings (PSUs). There is the initial public offering (IPO) option as well, where you can invest in PSU IPOs with turnover of more than Rs 4,000 crore. And then there are mutual funds.

Financial experts feel that if the objective is to spread equity cult, index funds of mutual funds should also be included in the options. “In fact, it will be better for new investors simply because a new investor is risk-averse and index funds cap the losses in some ways,” says a fund manager.

The maximum amount you can invest is Rs 50,000. But the tax benefit is on 50 per cent of the amount, Rs 25,000. The deduction will be, according to your slab, which will be either 10 per cent or 20 per cent (given the Rs 10 lakh income limit). So, the benefit for the person will be Rs 2,500-Rs 5,000.

This is the simple part. The complexity begins from the second year. While the scheme allows you to book profits and sell shares, the RGESS account has to be replenished with shares purchased with the proceeds. If the conditions are violated, the benefits under Section 80CCG will be withdrawn.

This is quite complicated. Because on the one hand, the scheme is getting liquidity due to the option of profit booking. But a new investor could always get into trouble if he tries to take too many decisions on his own.

“The lock-in period should be on the lines of ELSS. Why allow new investors to make changes after one year, especially when the investment universe is restricted to large cap stocks?,” asks Rustagi. Also, if someone buys more shares and does not want to them to be locked-in, he will have to declare it within a month in Form B. All these tiny additions make it complicated.

In comparison, ELSS is simpler. For one, there is no income limit that is set – anyone can invest in it. The benefits are not additional, and they come to you under Section 80C. That is a limiting factor because of the long list of instruments under this section, which includes ELSS, employee provident fund, public provident fund, life insurance premiums, pension plans of mutual funds, five-year fixed deposits, principal payment of home loans and others. So, most people end up exhausting this limit.

But if you have not exhausted the limit, benefits of investing through ELSS are significantly higher. For instance, if you invest Rs 1 lakh in this instrument, the benefit would be Rs 10,000-Rs 30,000, according to the slab.

Yes, RGESS is an option for investors who want additional tax benefits. If you really want to take advantage of this scheme, treat it like ELSS. Invest and forget for three years. Otherwise, all the tiny clauses will give you ulcers.