In the past year, the net asset value (NAV) of direct mutual fund plans and the returns delivered by these have been better compared to regular funds. In the case of equity (large- and mid-cap) funds, the NAV of direct plans stood at Rs 290.57 on February 5, while that of regular plans stood at Rs 288.45 (on the higher side); on the lower side, direct plans' NAV was Rs 3.51, while that of regular plans was Rs 3.48. In this space, one-year returns have fallen 4.39 per cent for regular plans, while the loss in returns from direct plans was lesser at 3.3 per cent.

The highest NAV for equity (mid- and small-cap) funds stood at Rs 340.99 for regular plans, against Rs 343.78 for direct plans; on the lower side, these stood at Rs 8 and Rs 8.04, respectively. The range of NAV is very wide, as some funds might have been launched later and/or might not have fared well due to the volatile market conditions. Again, the erosion in returns for direct plans was less (3.19 per cent) compared to that of regular plans (3.79 per cent).

In the case of equity-oriented hybrid or balanced funds, the highest NAV stood at Rs 358.98 for direct plans, compared with Rs 356.67 for regular plans. On the lower side, these stood at Rs 10.73 and Rs 10.71, respectively. These funds have returned 5.06 per cent in the case of regular schemes and 5.69 per cent for direct ones (

Click for table 1).

Now, let's take a look at debt funds. For liquid funds, the highest NAV ranged between Rs 3,460.12 (regular plans) and Rs 3,085.38 (direct plans). The lowest NAV quoted Rs 13.05 for regular plans and Rs 13.88 for direct plans. At 8.87 per cent, returns were 0.46 per cent higher for direct plans.

In case of income funds, the highest NAV stood at Rs 1,558.51 and Rs 1,594.50 for regular and direct plans, respectively. On the lower side, these stood at Rs 9.76 for regular plans and Rs 9.79 for direct plans. For the latter, returns were 0.81 per cent higher.

For investors in fixed maturity plans (FMPs), the difference in NAVs and returns weren't substantial.

Direct plans came into existence after the Securities and Exchange Board of India (Sebi) asked fund houses to provide investors with direct access to mutual fund schemes, cutting distributors' costs. The total expense ratio of direct plans is lower than that of regular plans to the extent of distribution costs, which are ploughed back into the fund. Therefore, returns from direct plans are higher than that from regular plans.

According to Sebi rules, equity funds charge 2.5-1.75 per cent as annual expense ratio, while debt funds charge 2.25-1.5 per cent. One can save on this cost through direct plans.

Manoj Nagpal, chief executive of Outlook Asia Capital, says, "The benefit of investing in direct plans is around 40-50 basis points for equity. For liquid funds, it is lower at about five-10 basis points; it is 15-20 basis points for short-term debt funds and 20-30 basis points for long-term debt funds."

At a time when the National Stock Exchange's 50-stock Nifty has returned only 1.1 per cent through a year, a 0.5 per cent increase in returns could mean a lot, especially through the long term.

When does it make sense to opt for direct plans? Nagpal says in the long term, all investors - those who invest through systematic investment plans (SIPs) and lump sum - stand to record equal benefits. Only, benefit realisation will be recorded through a longer term in case of SIP investment. "A bulk investor will see the difference or benefits of direct investment in three-six months, while it will be apparent to an SIP investor in 18-20 months," says Pankaaj Maalde, head (financial planning) at Apnapaisa.

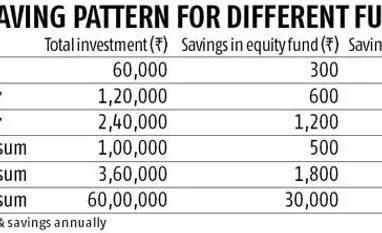

Say, you invest in debt funds through an SIP of Rs 5,000 a month. Your total annual investment will be Rs 60,000. This means you will save Rs 120 a year with direct plans. An SIP of Rs 10,000 a month will help you save Rs 240 a year, while an SIP of Rs 20,000 a month will help you save Rs 480.

"However, given the target returns for a debt scheme are eight-10 per cent, a gain of even 0.2 per cent looks better than a 0.5 per cent gain on equity. This is because the target returns on an equity fund are higher at 12-15 per cent," explains Hiren Dhakan, associate fund manager at Bonanza Portfolio.

If you take into account the smaller costs---the number of man-hours, travel costs, etc---in direct investments, a lump sum investment in debt schemes seem more sensible. If you invest a lump sum of Rs 1 lakh, you will save Rs 200; a lump sum of Rs 3 lakh will save you Rs 720 at a go. You will accumulate Rs 720 in savings through three years, in case you invest through an SIP of Rs 10,000 in a debt scheme. A lump sum investment of Rs 5 lakh will help you save Rs 12,000 a year. But through an SIP of Rs 10,000, it will take a very long time to record savings of Rs 12,000.

In comparison, as equity funds help you save more, investing through an SIP might not be a bad idea. An SIP of Rs 5,000 a month or a total investment of Rs 60,000 a year will fetch you Rs 300 more annually (as shown in table 2). An SIP of Rs 10,000 will fetch Rs 600 more a year. If you invest Rs 20,000 through an SIP, you will save Rs 1,200 a year.

Of course, a lump sum investment will fetch you much more than a lump sum investment in debt. However, even the small benefits over SIP investments will, in the long run, make a lot of difference to small investors.

The gains on equity-oriented hybrid funds will be similar or a tad lower than those on equity, as these funds include debt. And, the gains on debt-oriented funds will be similar or a little higher than on debt funds, owing to the equity component in it.

But not many individual investors have taken to direct plans. According to a study by CRISIL Research, direct plans, launched in January 1, 2013, are primarily attracting large investors, though average assets under management (AUM) of direct plans offered by mutual funds rose about 70 per cent to Rs 2.14 lakh crore during the June 2013 quarter from Rs 1.27 lakh crore in the March quarter. These accounted for 25 per cent of the overall AUM of the sector, against 15 per cent in the previous quarter. Debt-oriented mutual funds account for 98 per cent of the overall AUM under direct plans. In the debt category, liquid and ultra-short-term debt funds were the highest contributors to the average AUM of direct plans.

If you plan to switch to a direct plan from a regular one, you will have to pay an exit load, securities transaction tax (STT) and short-term capital gains tax, in case your investment is less than a year old. A number of fund houses have increased the exit load to three per cent. Therefore, if it is merely aimed at earning an additional 30-50 basis points, it doesn't make much sense to shift. If the investment in equities is more than a year old, there will be no capital gains tax or exit load; STT alone will be applicable.

"SIPs in direct equity schemes make sense")