"Tax-shield your retirement corpus")

With increasing life expectancy, individuals now live over 25 years post retirement. That's why a person should start planning early for the golden years. Regularly investing small amounts can help to create a big corpus over time. Reaching this desired goal, however, is just half the battle won. It is equally important to allocate the retirement portfolio in a way that it not only generates sufficient returns but also proves to be tax-efficient.

A portfolio of a retiree is constrained by the fact that he cannot take undue risk. It needs to have four components-regular income investments, short-term instruments, medium-term products and, and long-term ones.

Regular income products

Though bank monthly income schemes (MIS) are the most popular investment option among those looking for guaranteed regular income, the interest is taxable as per the individual's tax bracket, and hence a senior cannot have a large portion of corpus in it.

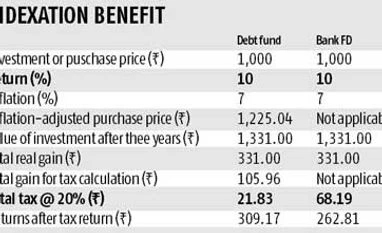

MIPs: Though not clearly an alternative to MIS, mutual fund Monthly Income Plans (MIPs) offer a more tax-efficient way of earning regular income. MIPs largely invest in debt instruments and have some exposure to equity. To make MIPs more tax-efficient, opt for the growth option as dividends on debt funds are taxed at 25 per cent. A person needs to keep the money invested for at least three years and then opt for the systematic withdrawal plan (SWP). Ask the fund house to give you a fixed monthly payout irrespective of the fund's performance. Returns after three years are considered long-term capital gains, which are taxed at 20 per cent after indexation (See table: Indexation Benefits).

SCSS: Another tax-efficient option under this category is the Senior Citizen Savings' Scheme (SCSS), available for individuals aged 60 or above. SCSS offers a higher rate of return than bank fixed deposits (FDs) and Public Provident Fund (PPF). There is a lock-in period of five years. At present, SCSS is offering 9.3 per cent compared to PPF's 8.7 per cent. The interest is paid quarterly and is taxable. It's clubbed with income.

But investment in SCSS is eligible for income tax deduction, which can help offset the tax on interest. For example, if you invest Rs 1.5 lakh in SCSS, and assuming you fall in the 20 per cent tax bracket, you save Rs 30,900 (including three per cent education cess). The total interest income during the year after paying the tax would be Rs 11,076. The effective interest rate comes to 9.23 per cent.

Usually, a short-term fund should be kept in the liquid investment option, so that it can be used for emergencies. This should not be more than 5-10 per cent of a person's corpus.

A part of short-term fund can always be kept in savings account, as interest income from savings account up to Rs 10,000 a year is non-taxable. Given a four per cent interest rate on savings account, an individual can always have up to Rs 2.5 lakh in bank.

If you are in the lower tax bracket, 10 per cent or 20 per cent, you can also keep a part of your emergency fund in liquid schemes, which invest in very short-term debt securities, and therefore, are low risk options. Any short-term capital gains from liquid fund are taxed as per an individual's tax slab.

Medium-term products

For medium term, a person could consider accrual-based debt funds. These funds typically follow the strategy of holding a debt security to its maturity. This way, the fund minimises the risk of drop in bond price due to increase in interest rates. Fixed maturity plans or FMPs with three years or more lock-in period are good medium-term investment options too. They offer better return than bank FDs and are tax-efficient.

Long-term products

It is recommended to keep 50-60 per cent of corpus in long-term (five years or more) instruments that not only offer higher returns but are also tax-free. This part of the portfolio helps the corpus grow faster and lasts longer.

Equity mutual funds: Invest in good equity funds - large or multi-cap schemes - with a long track record of consistent performance. Equity mutual funds have the pot-ential to consistently giving dou-ble-digit returns averaged over time. However, the best thing about investing in them is that the long-term capital gains and dividend payments are tax-free.

Balanced fund: Investors not comfortable with 100 per cent equity investments can opt for balanced funds, which invest in a combination of equity and debt instruments. The equity portion will always be 65 per cent or more of the portfolio. The remaining is put in debt instruments to provide cushion to investments in a falling market. They are taxed just like equity funds.

Tax-free bonds: These are long-term bonds with tenure of 10-15 years, issued mostly by government companies. Though the interest offered on these bonds is less than the bank FD rates, it's completely tax-free. If a bank FD offers 9 per cent interest and you fall in the 20 per cent tax bracket, your after-tax returns from the FD would be 7.2 per cent. However, if the tax-free bond offers 8 per cent interest, the effective rate would be same as the rate of interest.

PPF: It is safe, offers decent retu-rns (8.7 per cent currently), and is completely tax-free. Apart from this, the investment in PPF is eligible for income tax deduction. It has a long lock-in period of 15 years.

Managing money and making it work is not easy. However, with patience and planning, one can make the most of his or her retirement fund.

A portfolio of a retiree is constrained by the fact that he cannot take undue risk. It needs to have four components-regular income investments, short-term instruments, medium-term products and, and long-term ones.

Regular income products

Though bank monthly income schemes (MIS) are the most popular investment option among those looking for guaranteed regular income, the interest is taxable as per the individual's tax bracket, and hence a senior cannot have a large portion of corpus in it.

MIPs: Though not clearly an alternative to MIS, mutual fund Monthly Income Plans (MIPs) offer a more tax-efficient way of earning regular income. MIPs largely invest in debt instruments and have some exposure to equity. To make MIPs more tax-efficient, opt for the growth option as dividends on debt funds are taxed at 25 per cent. A person needs to keep the money invested for at least three years and then opt for the systematic withdrawal plan (SWP). Ask the fund house to give you a fixed monthly payout irrespective of the fund's performance. Returns after three years are considered long-term capital gains, which are taxed at 20 per cent after indexation (See table: Indexation Benefits).

SCSS: Another tax-efficient option under this category is the Senior Citizen Savings' Scheme (SCSS), available for individuals aged 60 or above. SCSS offers a higher rate of return than bank fixed deposits (FDs) and Public Provident Fund (PPF). There is a lock-in period of five years. At present, SCSS is offering 9.3 per cent compared to PPF's 8.7 per cent. The interest is paid quarterly and is taxable. It's clubbed with income.

But investment in SCSS is eligible for income tax deduction, which can help offset the tax on interest. For example, if you invest Rs 1.5 lakh in SCSS, and assuming you fall in the 20 per cent tax bracket, you save Rs 30,900 (including three per cent education cess). The total interest income during the year after paying the tax would be Rs 11,076. The effective interest rate comes to 9.23 per cent.

Usually, a short-term fund should be kept in the liquid investment option, so that it can be used for emergencies. This should not be more than 5-10 per cent of a person's corpus.

A part of short-term fund can always be kept in savings account, as interest income from savings account up to Rs 10,000 a year is non-taxable. Given a four per cent interest rate on savings account, an individual can always have up to Rs 2.5 lakh in bank.

If you are in the lower tax bracket, 10 per cent or 20 per cent, you can also keep a part of your emergency fund in liquid schemes, which invest in very short-term debt securities, and therefore, are low risk options. Any short-term capital gains from liquid fund are taxed as per an individual's tax slab.

Medium-term products

For medium term, a person could consider accrual-based debt funds. These funds typically follow the strategy of holding a debt security to its maturity. This way, the fund minimises the risk of drop in bond price due to increase in interest rates. Fixed maturity plans or FMPs with three years or more lock-in period are good medium-term investment options too. They offer better return than bank FDs and are tax-efficient.

Long-term products

It is recommended to keep 50-60 per cent of corpus in long-term (five years or more) instruments that not only offer higher returns but are also tax-free. This part of the portfolio helps the corpus grow faster and lasts longer.

Equity mutual funds: Invest in good equity funds - large or multi-cap schemes - with a long track record of consistent performance. Equity mutual funds have the pot-ential to consistently giving dou-ble-digit returns averaged over time. However, the best thing about investing in them is that the long-term capital gains and dividend payments are tax-free.

Balanced fund: Investors not comfortable with 100 per cent equity investments can opt for balanced funds, which invest in a combination of equity and debt instruments. The equity portion will always be 65 per cent or more of the portfolio. The remaining is put in debt instruments to provide cushion to investments in a falling market. They are taxed just like equity funds.

Tax-free bonds: These are long-term bonds with tenure of 10-15 years, issued mostly by government companies. Though the interest offered on these bonds is less than the bank FD rates, it's completely tax-free. If a bank FD offers 9 per cent interest and you fall in the 20 per cent tax bracket, your after-tax returns from the FD would be 7.2 per cent. However, if the tax-free bond offers 8 per cent interest, the effective rate would be same as the rate of interest.

PPF: It is safe, offers decent retu-rns (8.7 per cent currently), and is completely tax-free. Apart from this, the investment in PPF is eligible for income tax deduction. It has a long lock-in period of 15 years.

Managing money and making it work is not easy. However, with patience and planning, one can make the most of his or her retirement fund.

The writer is CEO, BankBazaar.com