"Trump era and return of the NRI: Tips for people shifting back to India")

With President Donald Trump ordering a review of the H1B visa programme in the US, there are widespread fears among Indians working in the IT sector there that they may have to return home. For those who have migrated to West Asia, too, obtaining citizenship is difficult, necessitating a return at the end of their work tenure. Whatever the reasons for returning, non-resident Indians (NRIs) need to plan the shift meticulously. Besides finding a job that does justice to their skills and getting their children admitted into the right schools and colleges, they also need to handle the financial aspects of the transition well.

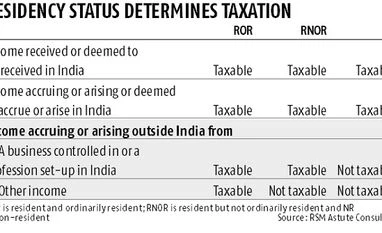

Tax residency status: Upon his return, an NRI first needs to determine his residency status for the purpose of income tax. This depends on the number of days he has been present in India. “India follows a physical presence test as the sole criterion for determining an individual’s residential status for income tax purpose,” says Suresh Surana, founder, RSM Astute Consulting. An individual can fall in any of these three categories: resident and ordinarily resident (ROR), resident but not ordinarily resident (RNOR, an intermediate stage for returning NRIs), and non-resident (NR). His residency status will determine how he is taxed (see table).

Re-designate bank accounts: Upon his return, an NRI must inform his bank about the change in his residential status. He will need to get his NRI accounts re-designated into resident accounts. “An NRI should re-designate his non-resident ordinary (NRO) savings account into a resident savings account. The balances in non-resident external (NRE) accounts should be re-designated to resident rupee accounts or to resident foreign currency (RFC) account. The foreign currency non-resident (FCNR) deposits may be allowed to continue till maturity at the contracted rate of interest,” says Pralay Mondal, senior group president, retail and business banking, YES Bank.

Also, a resident demat account should be opened and shares or units transferred to it from his NRI demat account. An NRI needs to approach his bank and submit requests for carrying out these changes.

Taxation of interest earned on savings account will also change once they are re-designated. Interest on NRE accounts, which has been re-designated to resident rupee account, will become taxable. Interest on NRO account was taxable earlier and will be taxable after re-designation, too. During the period that an NRI has the status of an RNOR, interest on RFC and FCNR accounts will be exempt.

The policies that a returning NRI needs to buy depends on what he is able to bring back with him. “The life insurance policy he had bought abroad may cover him even after he moves to India as their coverage is worldwide. But the health policy may not work in India since it operates only within a certain geography,” says Arvind Laddha, deputy chief executive officer, JLT Independent Insurance Brokers. Returning NRIs will have to buy an appropriate health insurance policy for themselves and their family.

Don’t rush to buy real estate: Give a lot of thought to whether you should buy a house immediately upon return or wait for some time. “If someone has been coming back to India regularly and likes a particular city, has friends in it, or had lived in it prior to moving abroad, he may find it easier to decide on the city. If not, an NRI should first settle into a rented house, find his bearings, and then buy after some time,” says Lovaii Navlakhi, founder and CEO, International Money Matters.

Verify the developer’s credentials before purchasing from him. Visiting his past projects and speaking to people living in them will give him an idea of the quality of construction and the likelihood of timely delivery. If in doubt, opt for a ready-to-move-in property. “Get information on the infrastructure planned in the region. Connectivity to key areas and central markets should be a key consideration. If an NRI is not well versed with the local realty market, he should avail the services of a reputed consultant,” says Anupam Rastogi, principal partner, Square Yards. The real estate market in India is in the midst of a slowdown. Any purchase for investment purpose should only be done with a sufficiently long horizon of 7-10 years.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in