"Want regular dividends? Balanced funds may not be your best bet")

Has a mutual fund distributor tried to sell a balanced (equity-oriented hybrid) fund to you with the promise of a regular dividend each month? According to industry insiders, distributors are promising one per cent tax-free dividend each month (12 per cent a year) on these funds. While balanced funds are well suited for first-time investors in equities and for conservative investors, buying them to obtain a regular dividend would be a mistake.

Experts say that, technically, the promise of a one per cent dividend each month might not be false. "It is possible that a person who has invested Rs 100 may get Rs 12 as dividend payout. But if the fund hasn't appreciated 12 per cent in a year, it will pay dividend out of its accumulated reserves. Its net asset value (NAV) will then take a hit," says Rajeev Thakkar, chief investment officer and director, PPFAS Mutual Fund. Later, if the customer complains about the decline in NAV, the distributor is likely to offer the excuse that the NAV does fluctuate in a market-linked instrument.

In the current market environment, when interest rates on bank fixed deposits have plunged to 6.5-7 per cent and fixed-income investors are looking for alternatives, balanced funds are being offered as a relatively safe investment that can pay regular dividends. However, the basic nature of interest and dividend income is different. "Generally, interest income is fixed in nature while dividend is variable. Any advisor promising you a one per cent fixed return while using the word dividend is mis-selling," says Kunal Bajaj, founder and chief executive officer, Clearfunds.com, a Sebi-registered online investment advisor.

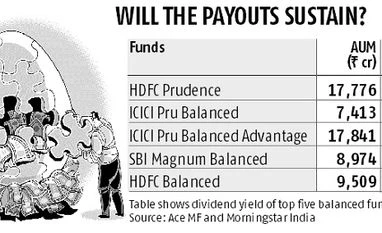

Balanced funds invest around 65-70 per cent of their portfolios in equities. This makes them volatile, though less than pure equity funds. "If the markets are down, fund managers will not want to sell securities at a loss. The fund may not generate capital gains at all in such times and hence not pay a dividend," says Kaustubh Belapurkar, director-manager research, Morningstar Investment Advisor India. If the fund has gathered reserves over time from capital gains, it may pay a dividend out of those reserves. "The AUMs (assets under management) of most of these funds have grown only recently. Their reserves are likely to be limited. Once the reserves get depleted, the fund will stop paying dividend," adds Belapurkar. Hence, the promise of a fixed rate of dividend is a sales gimmick that could play out for some time, but can’t be sustained.

Most investors should opt for the growth option in balanced funds to enjoy the capital growth that an equity-oriented fund can offer. "Only investors looking for income should go for the dividend option. But they should be fully aware that these dividends, while tax free, may come at irregular intervals," says Bajaj.

Balanced funds offer several advantages. They follow an in-built rebalancing model, so investors don't have to worry about over or under allocation to equity or debt. They also offer a tax advantage. While only 65-70 per cent of the portfolio is in equities, the entire portfolio (including the 30-35 per cent in debt) gets tax treatment at par with equities. If you want these advantages, invest in balanced funds by all means. But if you want a product that is likely to offer regular dividends, you should go for a monthly income plan, an ultra short-term fund or a liquid fund, though in their case too there is no promise of a regular return.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in