"Amend MSMED Act to ensure faster payments to MSEs")

Delays in receipt of dues from corporates remain a major challenge for micro and small enterprises (MSEs) in India, along with high cost of working capital finance and collateral requirements of lenders.

The Micro, Small and Medium Enterprises Development (MSMED) Act, 2006 stipulates that receivables of MSE suppliers must be paid within 45 days and accordingly disclosed in the buyer company's annual financial statements.

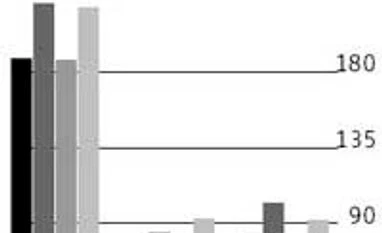

However, CRISIL's study of receivables of its rated MSEs in four large industries - engineering & capital goods, chemicals (including pharmaceuticals), electrical components & equipment, and steel products - reveals that receivables are nearly twice the stipulated period. MSEs constitute three-fourths of the working enterprises in these industries and face the common challenge of sizeable working capital requirement because of their high receivables and inventory positions, accentuated by low bargaining power with principal customers.

Once the credit terms are mutually agreed by the buyer and their MSE supplier and adhered to, the predictability of cash flows becomes easier to assess for lenders. This should help banks to shift to cash flow-based funding from balance sheet or collateral-based MSE funding.

The Micro, Small and Medium Enterprises Development (MSMED) Act, 2006 stipulates that receivables of MSE suppliers must be paid within 45 days and accordingly disclosed in the buyer company's annual financial statements.

However, CRISIL's study of receivables of its rated MSEs in four large industries - engineering & capital goods, chemicals (including pharmaceuticals), electrical components & equipment, and steel products - reveals that receivables are nearly twice the stipulated period. MSEs constitute three-fourths of the working enterprises in these industries and face the common challenge of sizeable working capital requirement because of their high receivables and inventory positions, accentuated by low bargaining power with principal customers.

Once the credit terms are mutually agreed by the buyer and their MSE supplier and adhered to, the predictability of cash flows becomes easier to assess for lenders. This should help banks to shift to cash flow-based funding from balance sheet or collateral-based MSE funding.