"Funding costs, growth worries hit stocks of housing finance companies")

The stocks of housing finance companies (HFCs) are in a bear phase for the third consecutive trading session.

Adding to their earlier losses, HFCs shed between 5 and 24 per cent during Tuesday's session.

The key issues for the market are the ability of HFCs to maintain their margins and improve loan growth in the near term.

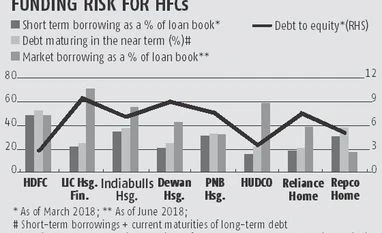

Firstly, shows that, on an average, 31 per cent of borrowed funds of eight HFCs will be maturing in the near term and this indicates the extent of elevated funding costs.

With higher interest and yields trajectory, cost of newly issued, renewed and rolled over funds would be higher.

Owing to stiff competition, HFCs would be forced to compromise on their profitability and take a hit on their net interest margin (NIM). NIM is the difference between interest earned and spent as a percentage of average loan book/interest-earning assets.

Also, HFCs are heavily dependent on market borrowings to fund their loan book. This is actually hurting them with the bond markets under pressure. As of June 2018, over 45 per cent, on an aggregate basis, of 8 HFCs' loan book is financed through non-convertible debentures and commercial papers, among others.

“Since cost of funds are increasing, market participants are selling their investments in the secondary market to recoup residual benefits of higher returns seen in the rally of past two years,” said Rajesh Gupta, AVP-retail at SBICAP Securities. Some experts believe that HFCs would have to bear 5-8 basis point cut in their margins for every 10 basis point rise in cost of funds.

Indiabulls Housing Finance’s issuance of commercial paper and bonds amounting to Rs20 billion is a positive development and will boost investor sentiment. The stock recovered at the end of Tuesday’s session. However, HFCs with low credit ratings could also find it challenging to avail financing, impacting their growth, say experts. Also, when interest rate is northward bound, debt investors typically keep their investment for the short term.

Hence, availing long-term funds from the debt market could be another challenge in the near term, indicating a possible asset-liability mismatch. "Either the funding cost will go up materially (under high interest rate situation) or one will run the risk of asset-liability tenure mismatch," said Prakash Agarwal, head-BFSI at India Ratings.

As of March 2018, an average 27 per cent loan book of eight HFCs was financed through short-term borrowings. However, experts do not see this as a serious concern.

On the flip side, the overall situation could propel retail market share of banks, mainly their housing book. Many public sector banks and private-corporate lenders are focusing on retail book amid asset quality issues from large corporate accounts. Moreover, they have strong low-cost deposit base, containing high cost pressure at relatively large extent.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in