"ITC Q4FY23 cigarette volume seen 13% up; Margin to see sharp yearly jump")

Analysts expect cigarette-to-hotel major ITC to deliver a strong operating performance in the March quarter (Q4FY23) amid firm growth across all its businesses, except agri.

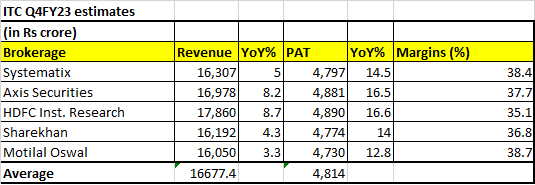

On a year-on-year (YoY) basis, the company could post a net profit growth of 14.9 per cent to around Rs 4,814 crore, as per an average of five brokerage estimates. Though sequentially, profit is expected to decline 3-5 per cent.

On the revenue front, it may report up to 9 per cent YoY growth to an average of around Rs 16,667 crore. SEE TABLE

{kind=link}

The major highlight will be the strong yearly EBITDA margin (earnings before interest, tax, depreciation and amortisation) gains of as much as 500 points to 38.7 per cent led by a fall in input costs, operating efficiency and a favourable product mix.

The core Cigarette business volumes are expected to grow 13 per cent YoY, as per three brokerages. The pace of increase was 15 per cent in Q3FY23.

The stock is up 28 per cent so far this year, as compared to a 1 per cent and 12 per cent rise in the Nifty50 and Nifty FMCG indices, respectively.

More From This Section

Key Monitorables: Investors will track commentary on consumer sentiment and demand outlook in both urban and rural markets, outlook on all businesses, competitive intensity and cues for demerger of the hotels vertical.

Here’s what brokerages expect:

Axis Securities: The brokerage sees cigarette segment revenue to grow 16 per cent YoY on a 13 per cent volume growth. FMCG vertical (non-cigarette) revenue is pegged to grow 14 per cent (on mid-volume growth) primarily led by price growth. The hotel business continued its strong momentum in the quarter and recovery was seen in the paper segment. Agri business is likely to decline on a high base. EBITDA margin is estimated to expand by 450 bps YoY on gross margin expansion, better mix, operating leverage and cost savings.

Sharekhan: Cigarette business revenues are expected to rise 13 per cent YoY led by 10-11 per cent volume growth, while the FMCG business is expected to grow 19 per cent. Sees a 70 per cent growth in hotel segment on sustained strong demand. The paper business is expected to grow 15 per cent, while agribusiness growth will likely decline 30 per cent. Gross margin and operating margin are seen expanding 335 bps and 320 bps YoY. Net profit is seen rising 14 per cent YoY in line with an equal growth in operating profit.

Motilal Oswal Securities: ITC is likely to post YoY sales growth of 3.3 per cent on a high base, continuing its healthy growth trend with an EBITDA and adjusted PAT growth of 18.9 per cent and 12.8 per cent, respectively. Sees a healthy 13 per cent volume growth in Cigarettes, maintaining the 4.5 per cent four-year average volume growth, and high average room rate in hotels. EBITDA margin to expand sharply by 500 bps YoY.

HDFC Research: The brokerage modelled a 16.8 per cent YoY growth in cigarette revenue, with volume growth of 16 per cent. The non-cigarette business is expected to grow 5 per cent YoY, which has been impacted by the agri-business. Sees 17 per cent YoY growth in the FMCG segment. Expects cigarette EBIT to grow 16 per cent YoY and sees FMCG EBIT margin at 7.3 per cent versus 5.7 per cent a year ago.

Systematix Institutional Equities: Sees Cigarette volume growth of 13 per cent, high growth in hotels and steady growth in the paper business. Sees limited possibility of valuation de-rating or earnings cuts in the stock.