)

Driven by the robust growth in exports and higher realisations, Bharat Forge notched up a 14 per cent year-on-year (y-o-y) jump in revenues to Rs 1,128 crore. Exports, which form 60 per cent of standalone revenues, grew a strong 21 per cent y-o-y and offset the muted six per cent growth in the domestic segment for the company. Going ahead, incremental growth in revenues from exports is expected to come from passenger vehicles, railways, and aerospace.

The June quarter results beat analyst estimates at the operating profit and net profit levels. While operating profits were higher at Rs 359 crore, up 23.5 per cent against the consensus number of Rs 345 crore, net profit was up 35 per cent at Rs 195 crore against the expectation of Rs 192 crore.

The firm has a capital expenditure plan of Rs 1,000 crore over FY15-17, which will be incurred on de-bottlenecking, improving capacity of machining, forging as well as research & development. The capex outlay for FY16 is pegged at Rs 350 crore.

While its non-auto verticals such as railways and aerospace are picking up, given the falling oil prices and a lack of offshore activity, the pressure point remains the oil & gas space, which accounts for 10 per cent of revenues. Any improvement in this vertical will add to revenue momentum for the company, which is looking to improve its performance by sweating its assets further and this would include using existing facilities to execute orders from aerospace and passenger vehicle segments.

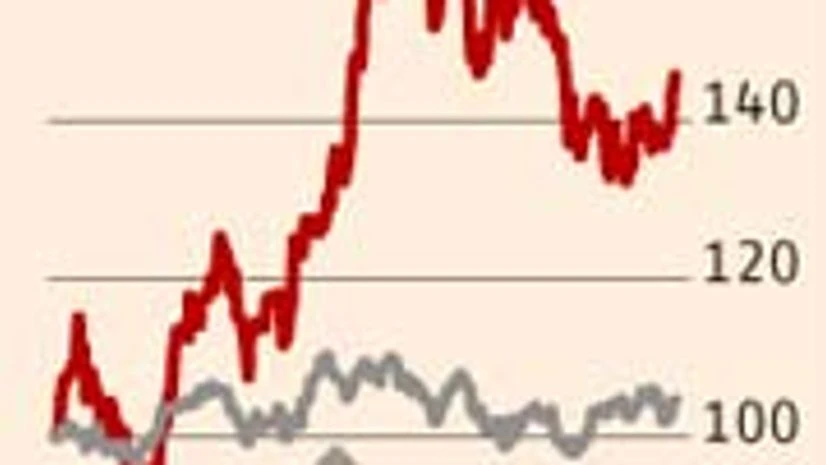

Most analysts covering the company have a ‘buy’ rating with a consensus target price of Rs 1,352, which translates into a 16 per cent return from the current levels. Given that some of the non-auto verticals (40 per cent of revenues) will take time to reach scale, investors with a two-three-year time frame can take exposure to the stock.