)

Pricing power, once a powerful tool in Indian cement companies' hands, is now missing. This is despite the start of the peak consumption period. Demand remains poor, leading to 100 million tonnes (mt) of capacity, or 30 per cent, lying idle.

After initial rises after monsoon, prices are flattening or softening. Sector leaders say poor demand is here to stay. Things will be clearer once elections happen.

Consider this: This time, last year, the average all-India price was Rs 295 for a 50-kg bag, now Rs 282, a fall of 4.5 per cent.

A mismatch in the pace of consumption and capacity addition has disrupted pricing power. Even ACC, Ambuja and UltraTech, with a pan-India presence, have been affected.

H M Bangur, managing director, Shree Cement, told Business Standard, “Hopes are not there. Nobody wants to spend money.

So, how would demand rise? Against estimates of seven-eight per cent, the sector is growing three-four per cent.”

In the north, a bag is Rs 252, a fall of Rs 5 against September-end's price. In the south, prices have slipped from Rs 318 to Rs 298; and in the east, rates are Rs 315 against Rs 340. The west has seen a tepid rise of Rs 2 to Rs 287.

In Mumbai, India's largest cement consumption market, a 50 kg bag is Rs 310, a rise of Rs 10.

Analysts say costs are on the rise. They do not rule out a further price fall of Rs 5-10, but add volatility in prices would continue.

“Such losses are unsustainable. Companies may be forced to cut capacity or shut shops,” added Bangur.

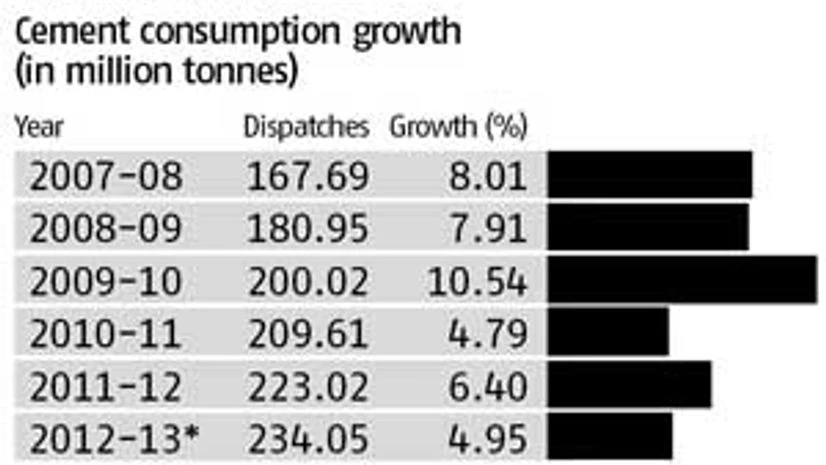

The sector doubled capacity since 2007 from 180 million tonne per annum (mtpa) to 360. However, in consumption, it is likely to remain a little less than 250 million in the current financial year. This means there is an overcapacity of 110 million.

Capacity use has been dropping for the last few years. If the situation remains grim, possibility of a reduction to below 70 per cent may not be ruled out. In the south, usage has dropped below 60 per cent.