"Nalco rides on London Metal Exchange gains, sees room for more price hikes")

Hindalco’s acquisition of US-based Aleris remains a positive for the domestic integrated aluminium producer. But it comes at a time when the world economy is in severe stress and hence, the benefits of the buyout may take more time than earlier anticipated.

The Street had started factoring in the completion of Aleris acquisition after approval from authorities, with one caveat — Aleris’ Duffel plant must be divested.

While it still allows Novelis (Hindalco’s US subsidiary) to enter the high-end aerospace segment, besides making it the leader in building and construction segment in the US, it now requires that Hindalco/Novelis also sell the US auto plant (Lewisport). And, this takes the sheen off the deal.

“The benefit of the acquisition appears significantly diluted without auto assets and bleak outlook for aerospace in the medium term,” say analysts at Kotak Institutional Equities, who value Aleris at negative Rs 15 per share in their sum of the part valuations for Hindalco.

Also Read

Novelis’ completion of Aleris acquisition at a final price of $2.8 billion is also about $200 million higher than the earlier announced price of $2.58 billion. The increase, however, is largely on account of additional working capital debt, and an additional payment of $50 million due to better-than-expected 12-month (trailing) performance of Aleris.

The implied enterprise value/earnings before interest, tax, depreciation, and amortisation (Ebitda) of 7.2x its 2019 financials is attractive, according to analysts, but it also increases debt.

After acquisition, net debt-to-adjusted Ebitda is about 3.3x, according to the company, but some analysts see it spiking to 4.4x in 2020-21 as divestment of auto plant may take some time in the current environment.

The debt is manageable, but discomforting, given the economic downturn, says a fund manager at a domestic brokerage, who sees stress on the company’s profitability in the near term.

Novelis being a converter had not seen much stress on the operating front in a low-aluminium-price environment. But, demand reduction can impact profitability, as all players are likely to push for higher volumes.

The demand for beverage cans remains intact, but the automobile sheet business is likely to feel the heat.

However, analysts also believe that most of the concerns due to the coronavirus disease (Covid-19) impact on demand, debt, realisations, and soft India business are factored in Hindalco's stock price.

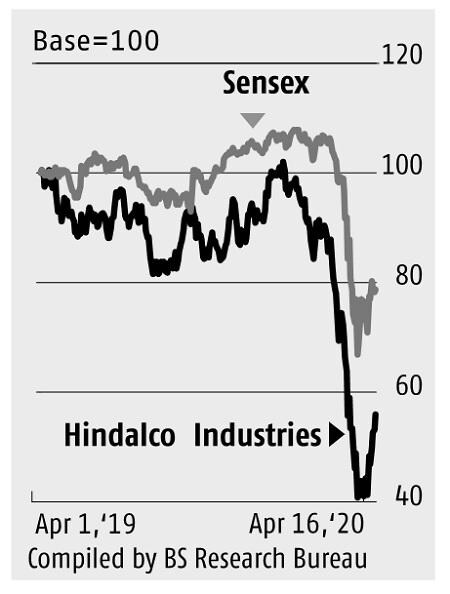

The stock has recently rebounded from closing lows of Rs 88.9 on April 3 to Rs 120.65, led by positive newsflow for metals, especially from China.

While one-year target price of analysts goes up to Rs 225, for further gains, the positive newsflow has to sustain.