)

Investors tend to be forgiving towards an occasional miss in quarterly performance if the company has a strong franchise. This same is true for Eicher Motors, which disappointed in the December 2014 quarter by reporting below-consensus margins and net profit. The market remains optimistic on the stock, thanks to the strong franchise of Royal Enfield. In the December quarter, the firm’s net profit grew 60 per cent year-on-year to Rs 154 crore but on a sequential basis, it fell seven per cent. The performance is below the Street's estimates.

The reason for the disappointment was largely higher marketing and research & development expenses, which should normalise. The consolidated operating margin improved 330 basis points to 13.2 per cent. The standalone margin at 23.6 per cent disappointed the Street as it was down 140 points sequentially. Analysts believe the company has chosen to front-load a lot of expenses during the quarter but the numbers would improve.

With new capacity in place, the company will address demand creation and boosting volumes. Eicher is looking at launching a new retail format across all Royal Enfield outlets and increasing number of dealerships to 500 by the end of 2015. The company is also setting up two R&D centres - in Chennai and the UK - to extend the product range.

ICICI Securities expects the company to track Harley Davidson's high growth phase in the coming years. Other than Royal Enfield, the company is also poised to capitalise on the recovery in commercial vehicles through the joint venture with Volvo. The company has not only extended the product range in the light and medium segment, but also in the heavy segment. The Volvo Eicher CV has increased market share in medium and heavy commercial vehicles segment to 12 per cent in FY14 from nine per cent in FY09.

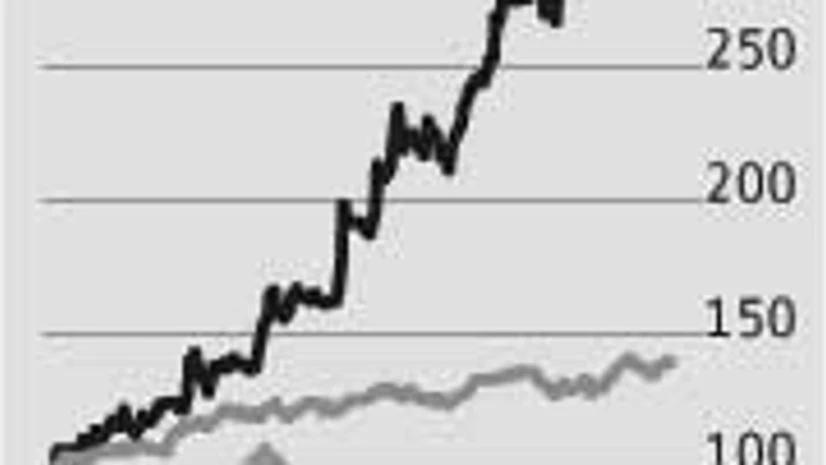

Based on strong catalysts such as strong volumes for Royal Enfield and margin recovery in VE Commercial Vehicles, Nomura has arrived at a target price of Rs 19,915 a share, indicating a 22 per cent upside.