"Electrosteel Steels: A test case of RBI's debt rejig scheme")

The Strategic Debt Restructuring scheme introduced by the Reserve Bank of India is set to change the managements of the companies which have failed to repay bank loans despite repeated extensions. In a 10-part series, we find out what ails these companies and why

Kolkata-based Electrosteel Steels, the first company where lenders invoked the strategic debt restructuring (SDR) after the Reserve Bank of India (RBI) allowed banks to take management control of defaulting companies last year, is set to get new promoters.

Bankers have zeroed in on London-based First International Group (FIG), partnered by China’s Laiwu Steel Group, having a capacity of 25-28 million tonnes (mt). The Chinese firm’s association with Electrosteel Steels is not new. It was an equipment supplier to the steel plant and has receivables of Rs 100 crore, which would be converted into equity subject to necessary approvals.

However, there is a twist to the tale. While FIG was a unanimous choice for bankers, it sprang a surprise on January 27 at a lenders’ meet. The fund wants the change of management to be outside of the SDR mechanism.

If lenders don’t agree, then negotiations with other companies that had made offers, including Tata Steel, could be reopened.

Subsequent to the SDR mechanism introduced last June, RBI came out with another circular for a non-SDR mechanism. This allows banks to upgrade credit facilities for borrowers whose ownership had been changed outside an SDR to the standard category, provided the stress was due to operational or managerial inefficiencies.

The basic difference, as pointed out by bankers, is that the SDR mechanism is less flexible and lenders have a greater say. “The SDR route is always beneficial for the banks, as they have a greater say in the company as they are the majority shareholder,” Karan Sachdeva, analyst with RBSA Advisors, explained. Bankers are yet to decide whether it would accept the FIG proposal of going for the non-SDR route, but they are under pressure to make a success out of Electrosteel Steels.

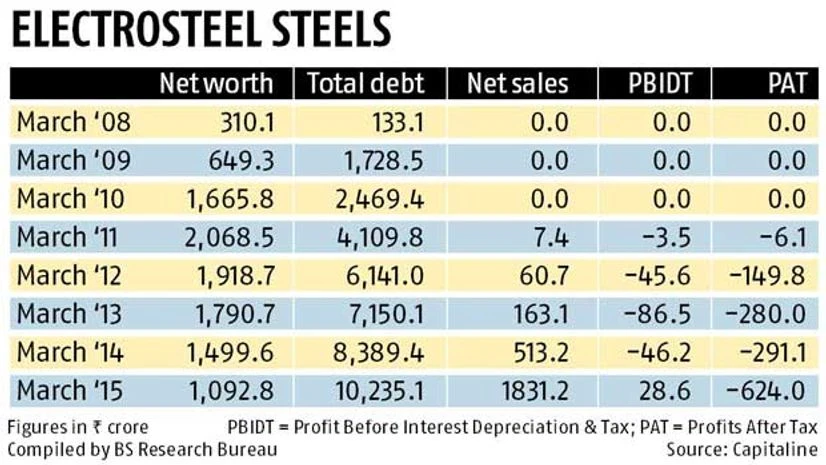

“It is extremely critical for lenders and new buyers to discover a price so that the haircut is minimal. If the new promoters are in the same line of business or a business of strategic importance, it is advantageous for the lenders as well as the new promoters,” said Vibha Batra, group head, financial sector rating at Icra. A Religare report suggested the haircut to attract a new promoter for Electrosteel could be around 65 per cent. Electrosteel has an outstanding debt of Rs 8,000 crore. Electrosteel Steels’ 2.51 mt integrated steel plant and ductile iron pipes project in Jharkhand was practically an import from China, with design and engineering all undertaken by Chinese companies.

The existing promoters, the Umang Kejriwal group, is, however, upbeat about the change of management. “We will support the new promoters in whatever way is required,” Kejriwal said about the FIG-Laiwu combine. Kejriwal is likely to handhold the new promoters with a minority stake.

A number of stumbling blocks had made Electrosteel Steels go haywire. Delay in project commissioning increased the cost by 20 per cent.

The Religare report said that Electrosteel Steels had been reporting losses since FY11 owing to inadequate installed capacity and nascent stage of operations. Net loss increased to around Rs 620 crore in FY15 due to lower realisations, higher interest cost and depreciation while debt/equity ratio increased to 9.4x in FY15 vis-à-vis 3.2x n FY12. In 2013, a consortium of 27 banks and financial institutions had supported a corporate debt restructuring proposal for the company that would have translate into cash generation of Rs 2,000 crore.

Banks supported the company largely due to the raw material linkages it flaunted. Electrosteel Steels was promoted by Electrosteel Castings, which had already secured Parbatpur coalmine having reserves of 231 mt. Plus, it had an iron ore mine and a non-coking coal mine in Jharkhand. Electrosteel Steels was to source iron ore and coking coal from Electrosteel Castings for a period of 20 years. But, then, the coal blocks of Electrosteel Castings were de-allocated in 2014 and Electrosteel Steels had to buy raw material at high prices from the market while finished product prices crashed.