Fight over soured deal in Asian Genco

PEs say promoter is taking police action to avoid arbitration in Singapore

)

In 2010, when marquee private equity (PE) firms led by General Atlantic, Goldman Sachs, Morgan Stanley, Norwest Partners and Everstone Capital invested close to $425 million in India-focused infrastructure firm Asian Genco, they never expected to, within four years, have the Hyderabad police on the watch to book them on charges of cheating.

This was after Asian Genco's main Indian promoter, Vijaykumar T V, filed a police complaint in this regard against the other directors, after relations between the PE funds and the Indian promoters had worsened. The PEs were unhappy over the delay in commissioning of the projects as promised when they invested in 2010. At present the PEs own majority shares in Singapore-based Asian Genco but do not have voting rights in the company. Asian Genco, in turn, owns stake in various projects in India.

When asked, an Asian Genco spokesperson said: “Certain inter-shareholder commercial issues are currently the subject of arbitration in Singapore. Since these are shareholder matters, it would not be appropriate for us to comment, other than to express the hope that they will be sorted soon. However, this has no impact on the project activities and their respective schedules.”

A spokesperson of the PE companies declined to comment.

Hyderabad police say Cobalt Power, a company owned by Vijaykumar, had invested Rs 200 crore in a Seemandhra thermal power project, promoted by Asian Genco. As Cobalt did not get back its money or get any share in the company, it approached the local court. The court directed the police to probe the cheating complaint against all directors of Asian Genco, which included the nominees of the PE entities.

Ravi Varma, the assistant commissioner of police investigating the case, says he has asked all Asian Genco directors to present themselves for questioning. However, of the eight, “only one or two” have met him so far and the police has given another 15 days for the directors to appear. He refused to give further details, saying “investigation is in progress”.

The PEs say the action by Vijaykumar was in retaliation for arbitration proceedings started by them in Singapore courts for management control and to recover their funds. The PEs were not happy with the progress in the power projects and as the costs shot up substantially due to delays in land acquisition in Andhra and an earthquake in Sikkim, returns from the projects also dried.

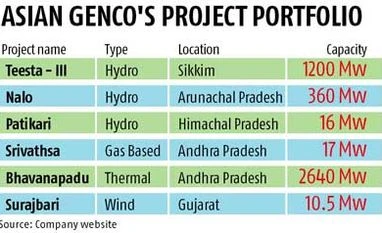

The PEs wanted to invest in the Indian infrastructure sector and were attracted by the projects set up by Asian Genco, which had a capacity of close to 4,000 Mw. These assets included the largest hydro project in the private sector in India, Teesta-III of 1,200 Mw, and a coal-fired, supercritical thermal project in Andhra Pradesh, the East Coast Energy phase- I of 1,320 Mw.

However, most of its projects have been delayed considerably and face massive cost overruns. Allegations of bending of rules to get a power project from the government of Sikkim have further delayed commissioning. Its Andhra project was facing opposition from locals over land acquisition. Vijaykumar was reportedly close to Jagan Mohan Reddy, son of the late Andhra chief minister, Y S Rajasekhara Reddy, and former Union power secretary R V Shahi, helping it to bag projects. As Jagan fell out of favour with the Congress party, the fate of Asian Genco’s projects are hanging, resulting in PE money stuck or down the drain.

The company faced a lot of problem in its Sikkim project as it was alleged the government allotted the projects to a non-descript company called Athena, with no background in the sector, with delay in offering the mandatory stake to the Sikkim government. Athena later promoted a special purpose vehicle called Teesta Urja, with investments by Asian Genco, to enter into a joint venture with the Sikkim government later and become eligible for the project. The company had to offer 26 per cent stake to the state government for Rs 296 crore in July 2012.

The company also blames an earthquake in 2011 for its woes and the dispute with the Sikkim government over the allocation of shares. The project cost has shot up to Rs 8,600 crore from its original Rs 5,700 crore. Then followed the fight between the shareholders, which led to the projects now becoming almost unviable, say bankers.

(With inputs from Prashanth Reddy Chintala)

Don't miss the most important news and views of the day. Get them on our Telegram channel

First Published: May 22 2014 | 12:11 AM IST