)

Pharmaceutical sector stocks -- including Aurobindo Pharma, Cadila and Wockhardt -- saw some selling last week due to profit-booking and due to concerns on premium valuations.

While the sector’s price to earnings (PE) ratio has earlier traded at a premium to the broader markets. this has further expanded in this financial year. From 41 per cent in 2012, the premium to the benchmark Sensex had risen to 53 per cent in September last year and has since crossed 60 per cent. The sector benefited from growth in the high-margin Indian formulation business and a strong presence in the US generics space during FY13 and FY14. In addition, a rupee depreciation of 11-14 per cent added to the gains.

Aided by a jump in volumes, the domestic pharma segment has of late been recording double-digit growth rates. February saw growth of 19 per cent over a year before, the highest in three years. About 70 per cent of this was led by volume gains, aided by new product launches; the rest was due to price increases. With the strong volume show, Surajit Pal of brokerage advisory Prabhudas Lilladher expects growth in the Rs 85,000-crore Indian market to sustain in FY16.

Analysts also expect growth in the US to remain resilient. What will contribute, they say, is higher realisations from product launches and a rising share of limited-competition drugs, leading to an improved product mix and margins. While an adverse US Food & Drug Administration scrutiny outcome for a few companies could lead to stock correction, the risk to longer term valuations are limited, say JPMorgan analysts. They point to India’s position as a low-cost supplier of generic drugs to the US, a market which remains the key driver for growth and investment for companies here.

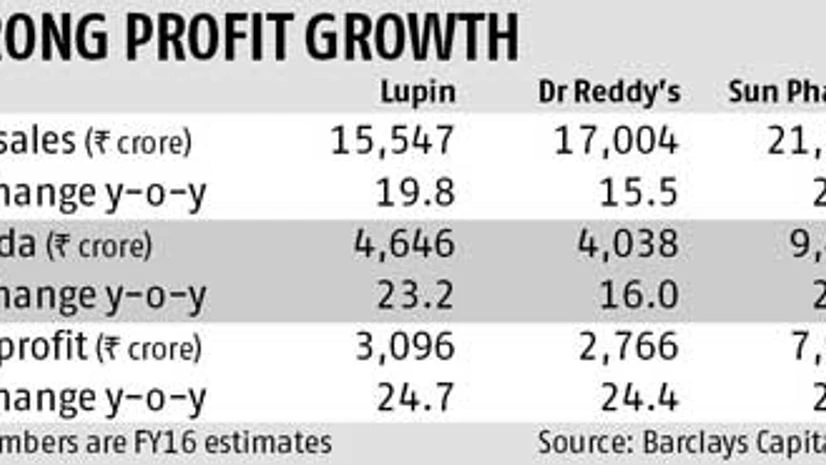

Most brokerages are positive on the prospects of large Indian generic makers but prefer names such as Lupin, Dr Reddy’s Laboratories and Sun Pharma. A closer look at these:

Lupin

Given the staggered entry of generic competition in the US for Nexium (an antacid) and increased product launches in the coming financial year, most brokerages have raised their earnings estimates. They expect Lupin's earnings to grow 22 per cent annually over FY15-17, against 19 per cent earlier. The stock now commands a higher one-year forward multiple of 23-25 times, against 21-22 times earlier.

The company has so far done better than peers on execution and cost. Analysts at Axis Capital expect growth to be powered by strong visibility on the Abbreviated New Drug Application (ANDA) pipeline in the US market (45 per cent of overall revenue in FY15), the growing India business, potential value-accretive mergers and acquisitions, and partnerships to build its speciality portfolio of dermatological, inhalation, injectables and biosimilar products.

Dr Reddy’s

While the stock is trading at a discount to larger peers due to near-term earning worries and regulatory challenges, analysts are positive on the company's prospects. They note its ANDA pipeline (43 per cent of revenue), market share gains for products (both here and in the US) and strength in research & development (R&D).

Of the 68 pending ANDAs, 60 per cent are complex generics, with injectables forming a third of the pipeline, and 20 per cent of sales, which should boost realisations and margins. Analysts say margin concerns, given the large investments in R&D (it has been one of the largest spenders), could come down as it brings some products to the market. Increased traction in its niche portfolio should also aid profitability.

Sun Pharma

Sun Pharma continues to take the inorganic route to growth (the latest acquisition being GSK’s opiate business), and given that it generates more cash than it can employ, analysts expect more acquisitions going ahead. However, given the complexity of the Ranbaxy merger and the focus on maximising synergies between the two companies, it will be some time before Sun Pharma will look at large acquisitions. Going ahead, the key catalysts would be sales momentum for anti-cancer drug Doxil and price hikes taken by Taro. On the domestic front, the company continues to grow at a steady pace recording a 16 per cent growth in February and that too on a high base. At the current market price, the stock is trading at 21 times its FY17 earnings.

Cadila Healthcare

The company saw strong earnings growth in the first nine months of FY15, on the back of a 61% year on year growth from the US business, plus margin expansion. Analysts expect margins to increase by 400 basis points, from 16.6% in FY14 to 21% by FY17, due to higher incremental filings in niche segments like dermatology, respiratory and complex injectables.

Given the strong performance expected from the US market due to the product pipeline and approvals, analysts expect annual earnings growth in the FY15-17 period to be 25-40%.