)

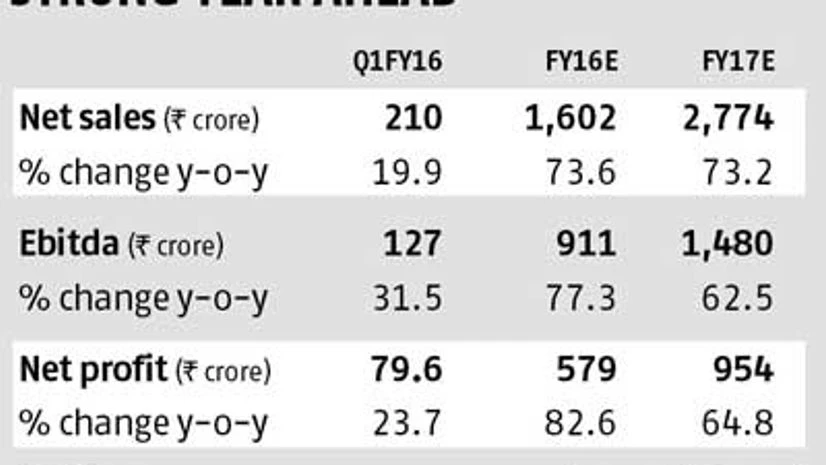

Oberoi Realty’s quarterly results were a bit below expectation, with revenue growing 20 per cent from a year before to Rs 210 crore, despite a low base and high-value project sales.

One reason could be that most of the revenue in the housing segment has come from the Exquisite project. Revenue recognition from other projects such as Esquire hasn't started, expected to begin from the current or next quarter. Both these are in Goregaon (Mumbai), which accounts for about half of its total area under development across locations (including commercial assets), and is the single largest contributor to the company’s asset value.

Given the recent sales of flats in the Exquisite project, realisations from here were higher at Rs 24,000 a sq ft as against overall realisations of Rs 21,179 a sq ft. Aided by this, margins were 60.6 per cent, about 500 basis points higher than the year-ago quarter.

Going ahead, the key trigger is the launch of a million sq ft at its Borivali project in the Mumbai suburbs in the current (September) quarter and 0.5 mn sq f of phase-2 of its Mulund (also in Mumbai) project by October. Toward the end of the year, launch of its Oasis project in Worli (Mumbai) will be an additional trigger; this super-luxury development with an area of 0.7 mn sq ft is its second largest in asset value.

An uptick in sales collection in the quarter, as well as the recent preferential issue, should, according to analysts at IIFL, help the company be debt-free at the end of the September quarter. The company had debt of Rs 469 crore at the end of the June quarter.

On Monday, the stock slipped marginally by 0.6 per cent to close at Rs 279, trading at 16 times its FY16 estimates. Most analysts have a 'buy' rating, with target prices of Rs 325-372, translating to a return of 16 per cent at the lower end of the band.