)

Power Finance Corporation (PFC) and Rural Electrification Corporation (REC) posted good operational performance for the December 2014 quarter. Healthy loan growth and stable asset quality were the key positives.

Although provisioning was up 100 per cent on a year-on-year basis for both and impacted profit growth, this was to comply with the Reserve Bank of India (RBI)’s guideline, of five per cent provisioning on restructured loans by March 2018. Both will need to provide 2.75 per cent of restructured assets by March 2015 and the rest by March 2017. To achieve this, they will need to provide another Rs 120 crore each in this March’s quarter, estimate analysts at Kotak Institutional Equities. Thus, profit growth in the current quarter, too, might get impacted to that extent.

Asset quality trends, though, remained largely stable in the quarter. Both PFC and REC's gross non-performing assets ratio remained miniscule at one per cent (flat sequentially) and 0.8 per cent (down three basis points sequentially), respectively. Going forward as well, both stand to gain from power sector reforms, the coal auctions being in that direction. This will address the key bottlenecks faced by the power sector and rub off favourably on both credit demand and debt servicing abilities of power sector borrowers.

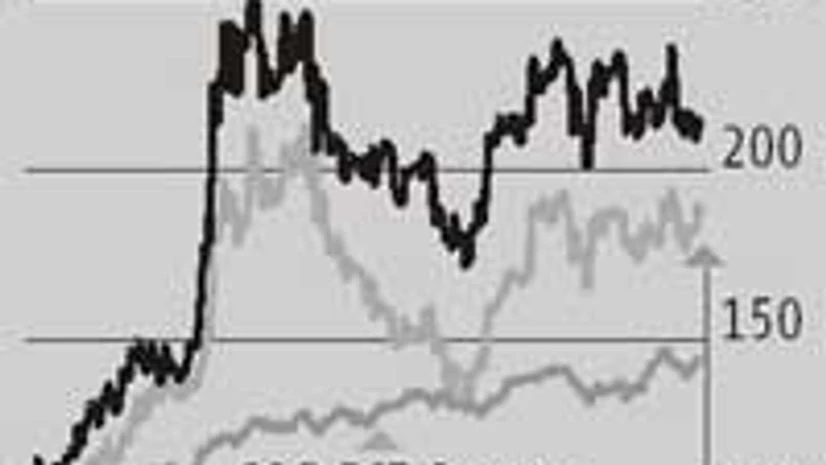

While the PFC scrip is trading 18 per cent lower than its 52-week high, that of REC is trailing this metric by about 12 per cent. Most analysts polled by Bloomberg in 2015 are bullish on PFC and REC. Their average target price indicates an upside of 20-21 per cent for each of these stocks.

Loans to the private sector grew at a healthy clip of about 31 per cent for REC and 30 per cent for PFC. Analysts estimate this metric to grow at a decent 10-15 per cent annually over the next two years and it could get accelerated with implementation of power sector reforms.

On the funding side, lower borrowing costs rubbed off favourably on the net interest margin (NIM), largely stable at five per cent for PFC and 5.2 per cent for REC. However, over the next two years, analysts believe the yield on loans to state electricity boards might come down and, thus, lead to some compression in NIM for both.