"Pharma firms to go for more big buys in US")

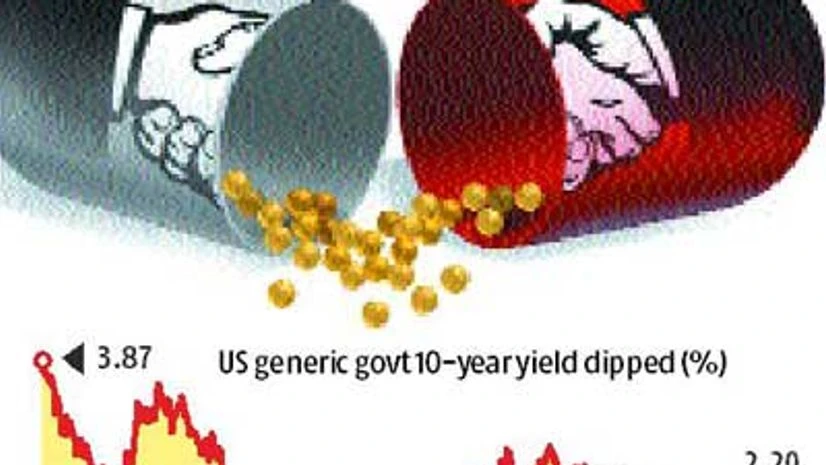

At the end of the past financial year, the top-10 Indian pharmaceutical companies had free cash flow of Rs 15,666 crore, more than double the Rs 7,195 crore reported five years ago. In the same period, the 10-year US treasury yield dropped to 2.18 per cent from 3.87 per cent, bringing down the cost of finance for doing acquisitions in the US substantially.

This explains how the two most valued acquisitions by Indian pharma companies in the US were achieved in the past couple of months. First, Lupin acquired US-based Gavis Pharmaceuticals and Novel Laboratories for $880 million in July, followed by Cipla with its $550-million acquisition of InvaGen and Exelan earlier this month.

“Indian pharma companies have gone to the US market with different strategies at different times. After getting the US FDA’s (Food and Drug Administration) approval for their domestic manufacturing facilities, they have largely explored with having front-end and distribution tie-ups, beside making mid-size acquisitions,” says Amitabh Malhotra, managing director at global investment banking firm Rothschild. “Now, they have evolved in their life cycle and come to a stage where their risk appetite allows them to make big-ticket acquisitions.”

The US is the world’s largest market for generic products with an estimated value of $35 billion in annual sales, compared with India’s $14 billion annually. Cipla’s acquisition will add 32 products to its portfolio that are in the market and 30 more are expected to be launched in the next four years.

Cipla and Lupin had recorded free cash flow of Rs 1,338 crore and Rs 2,536 crore, respectively, in the past financial year. “Besides, interest rates in the US are so low that the cost of fund becomes really cheap. Eventually, it helps in making these deals instantly EPS (earnings per share)-accretive,” adds Bakhru.

While the aggressive acquisition makes financial sense, there are other compelling reasons, too, for Indian companies to take this route. “One reason is also that getting US FDA’s approval for a new plant is much longer and harder now, so the time to market is also getting impacted. Therefore, taking the aggressive inorganic route is making sense,” says Pramod Kumar, managing director and head advisory at Barclays in India, who advised Cipla for the acquisition.

Free cash flow at the top-10 Indian pharma companies grew at a compounded annual rate of 21 per cent in the past four years. Besides, eight of the 10 companies, barring Glenmark and Jubilant Life, have their debt equity ratio below one, indicating room for leverage.

Dr Reddy’s Labs, Torrent Pharma and Aurobindo Pharma are the three other companies that generated high free cash flow in the past financial year — Rs 2,090 crore, Rs 2,022 crore, and Rs 1,330 crore, respectively. This gives them the financial strength for making big acquisitions in the US market.