"Ramsarup group wilful defaulter 'by mistake'")

The promoter of three Kolkata-based entities, which owe about Rs 410 crore to various banks, has claimed the group's name has found its way to the list of wilful defaulters by 'mistake'. But, the bankers insist these are indeed wilful defaulters and have been declared so after following all the applicable norms.

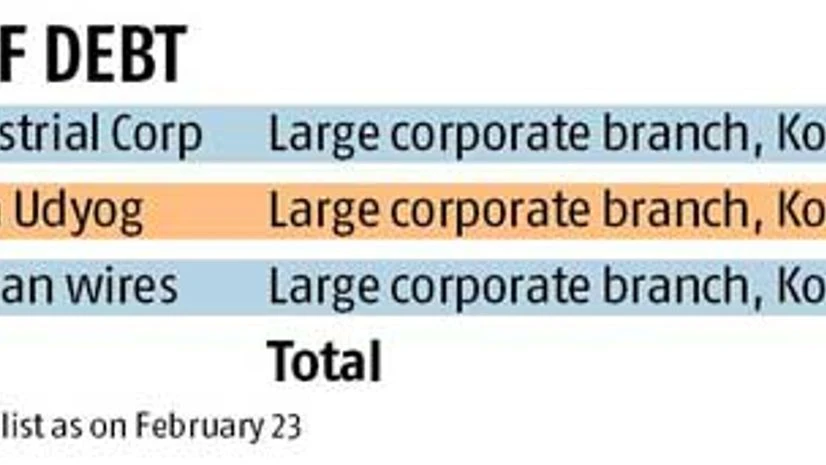

Last month, Delhi-based lender Punjab National Bank (PNB) published a list of 905 wilful defaulters who had defaulted on loans of Rs 11,467 crore. Ramsarup Industrial Corporation (RIC), Ramsarup Lohh Udhyog (RLU) and Ramsarup Nirman Wires (RNW) were named in the list with dues of around Rs 100 crore each.

According to ministry of corporate affairs (MCA) records, the status of RLU, which had dues of Rs 129.34 crore, was shown as amalgamated. RIC and RNW, which owed Rs 133.19 crore and Rs 148.09 crore, respectively, did not figure in MCA suggesting these were not incorporated. All three were described as units of listed firm Ramsarup Industries and had given the same address in central Kolkata. Apart from PNB, UCO Bank, Vijaya Bank, Federal Bank, Axis Bank and ING Vysya were listed as lenders to the Ramsarup trio. Asset reconstruction companies such as Arcil and Pegasus ARC are on the group's case. Aashish Jhunjhunwala, Shambunath Khairi and Pradip Kumar Das were the common directors of these entities named on the PNB list.

When contacted by Business Standard, Jhunjhunwala, chairman and managing director of Ramsarup Industries, said, "There is some mistake with PNB regarding declaring us as wilful defaulters. We have received no communication from them; there was no discussion on this and we weren't given a hearing which is mandatory before declaring anyone wilful defaulter. We have written to them after we came to know about this mistake on PNB's part. But so far, we haven't received a revert from them." However, the bank has said due process has been followed before making these names public. "Borrowing companies stated in your communication have been identified and subsequently declared as wilful defaulters by following all the guidelines and procedures prescribed by RBI (Reserve Bank of India) in this regard," said a PNB spokesperson said in an email response.

The five-decade old group was engaged in manufacturing wires, TMT bars and steel. It had also developed interests in the power sector, before it ran into trouble. Ramsarup appears to be the victim of the crisis that has hit the steel industry. Its three plants in West Bengal have shut down as domestic demand fell and the office staff down-sized to cater to only official file-handling operations.

In its annual report for the year ended March 2015, Ramsarup Industries said, "A number of litigations have been filed by some of the lender banks and creditors of the company against which primary liabilities stand provided in the books except for other claims and interest thereon."

The financials for 2014-15 showed falling revenues and increasing operating losses. Total revenue from operation of the company is Rs 4.38 crore against Rs 10.30 crore in the previous year. Operating loss grew to Rs 5.97 crore against Rs 1.86 crore in the previous year. Loss before taxation was Rs 179.91 crore against Rs 489 crore in the previous year. "The company has incurred substantial losses due to non-operation of all the manufacturing units and day-to-day administrative expenses. Interest for the year on funds borrowed has been debited till June 2014 and subsequently, the company has not debited interest on borrowed funds as accounts of the company had turned NPA (non-performing asset) in the earlier years. This has led to lower losses to the extent of Rs 395.84 crore," the annual report said.

The group was founded in 1966 and had grown substantially in the first four decades. In 2005, it had sold shares in an initial public offering at Rs 60 apiece. "Our Group turnover was Rs 2,000 crore ($385 million) in 2008-09 with a net worth of Rs 450 crore ($82 million)," its website says in an undated entry. But, things went downhill beginning with the cancellation of major orders during the global financial crisis that followed the collapse of Lehman Brothers in September 2008. By FY12, the net worth of the company had eroded substantially and the firm had become a 'sick industrial company' under the provisions of Sick Industrial Companies (Special Provision) Act 1985 and "the Company was required to make reference with the Board for Industrial and Financial Reconstruction," according to the annual report.

In 2013, the Securities and Exchange Board of India (Sebi) had imposed penalties on two group entities controlled by Jhunjhunwala for alleged insider trading offences. Securities Appellate Tribunal had later upheld this order. A five-year graph of the share prices on the BSE showed that from a high of Rs 23.35 touched in April 2011, Ramsarup has dived 90 per cent to Rs 2.15 apiece on the BSE on Wednesday.

Downsizing has meant there are not enough people to even dust the files piled up across the office. Empty workstations without computers or operators tell the story of how this company has declined over the years.

Located in the shabby building in central Kolkata, the company now has only 30 people on its rolls, while the directors do not come to office regularly. "Only if a meeting is scheduled do the directors come," said an office staff.

Asked if the company is able to service its finances raised, an executive said, "From where are we going to earn money to pay for the loan? The steel crisis has taken a toll on us."