)

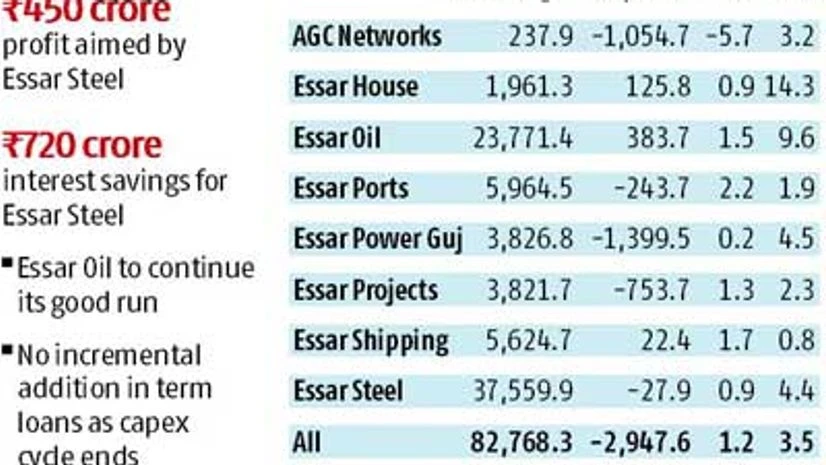

After almost three years, the Ruias of the Essar group are breathing easy. Key companies such as Essar Steel and Essar Oil are likely to report better metrics in the financial year ending March 2015, pulling the group out from the crisis it experienced in 2013-14. Backed by a ramp-up in production and higher capacity utilisation, the group expects its steel business to make a profit of Rs 350-450 crore in 2014-15 after four years of consecutive losses.

For a change, the market and investors seem convinced of the turnaround. Three of the four listed group companies — Essar Oil, Essar Ports and AGC Networks — have outperformed the broader market in the past one year. Essar Oil is up 80 per cent in past 12 months despite a poor show by the overall oil and gas index.

Essar Oil is expected to maintain its recent run of steady profits, buoyed by a global rise in gross refining margins. The company reported net profit of Rs 970 crore during April-December 2014. These two companies together account for 90 per cent of the group’s consolidated revenue and three quarters of its debt and liabilities. Its other businesses include ports, shipping, power, construction and information technology services.

“Essar’s capex programme is 95 per cent complete and assets are built at a very competitive cost. These assets will now generate cash flows and profits in line with the projections,” said V Ashok, group chief financial officer. He said the group’s long-term debt- equity ratio is 1.3.

At the end of March 2014, the group’s eight companies whose figures were available had total borrowings of Rs 82,768 crore, of which Rs 75,000 crore was term loans. Nearly 45 per cent of the debt is owed by Essar Steel, while Essar Oil accounts for another 29 per cent. The group’s debt is likely to remain around Rs 75,000 crore in 2014-15.

Capex completion

Essar Steel is completing its entire capital expenditure plan and now plans to ramp up production at its steel-making facility in Hazira and raw-material-processing plant in Odisha. This will increase the company’s revenues and operating margins.

Loss in the steel business was largely owing to inadequate production at Hazira, because of a lack of raw materials. Now, both raw material facilities in Odisha and Visakhapatnam are back on stream, allowing full capacity utilisation at Hazira. For 2015-16, Essar Steel expects its earnings before interest, depreciation, tax and amortisation (Ebidta) to increase to Rs 5,000 crore.

"With our steel business turning around since October last year, we expect the company's financial metrics to improve in the financial year 2015," said Firdose Vandrevala, executive vice-chairman, Essar Steel. Completion of the capex programme is likely to keep the group's long-term debt at last year's level, leading to improvement in debt-service ratios. Besides, the group has converted into dollars around $2 billion worth of rupee loans, resulting in annual interest savings of Rs 720 crore for Essar Steel.

The group's two flagship companies also witnessed fresh equity infusion from the promoter, leading to a rise in their net worth and decline in debt-equity ratio.

However, Ruia's steel plans are being challenged by a global slump in steel prices. According to a recent report by BNP Paribas, steel supply including imports in India grew by 13.3 per cent in 2014-15, while demand rose only 3.1 per cent, leading to sharp rise in inventories. This is likely to keep steel prices low, hitting Essar Steel's margins.

While the steel business is showing signs of a turnaround, Essar Oil, the group's biggest firm by revenues, reported decline in its debt and interest liabilities during the quarter ended December 2014. Debt declined to around Rs 17,500 crore from Rs 24,000 crore at the end of March 2014.

In the recent past, the oil giant came to the rescue of the loss-making Essar Power by buying out its assets. In 2014-15, it pumped in Rs 3,125 crore into Essar Power in two transactions. The company acquired 10.25 per cent cumulative redeemable preference shares of Essar Power, of the face value of Rs 1,025 crore, from Essar House, a promoter. It also bought equity and participating preference shares of Vadinar Power Company from Essar Power worth Rs 2,100 crore.

"Essar Oil is one of the better performing companies in the group and is expected to report steady profits for next few quarters due to steady gross refining margins of around $10 a barrel," said an analyst at a rating agency on condition of anonymity.

On the power business, a group official said the Mahan power project had tied up coal supplies from the Tokisud North coal block in Jharkhand after bagging the mine from the recently concluded auction. "We have taken possession of the mine and we expect coal supplies to start from next quarter-end. With the availability of coal from the mines, we expect to restart our Mahan power plant, lying idle for the last 18 months," said Sushil Maroo, chief executive and managing director of Essar Power.

On sale of assets, group officials said a decision had been taken by the management to induct strategic partners at the right valuation. The company wants to sell stakes in ports and oil refinery but company officials said they had not received any good offer as yet.