)

It's tough to be a steel maker but it's even tougher to be Tata Steel right now. A sharp decline in steel demand in China, the world's largest steel producer and consumer, and a corresponding decline in steel prices have battered the finances of steel makers all over the world.

Six of 18 of the world's top steel makers reported a sharp decline in net profit in the last financial year. Another three, including Tata Steel and the world's top steel maker ArcelorMittal, reported net losses. The steel industry's return on capital hit new lows with 16 of 18 companies in the Bloomberg index either reporting negative or low single-digit return on equity in the last financial year.

"The global steel industry is going through a deep cyclical downturn with supply outstripping demand globally. It will require a few years of growth to correct this supply-demand imbalance in the industry. Steel makers have little option but to wait out this downturn," says Sivarama Krishnan, partner and head of risk advisory at PwC India. According to him, this is normal in the commodity sector and this kind of cyclacity in growth and profitability is hard-wired into the DNA of commodity manufacturers.

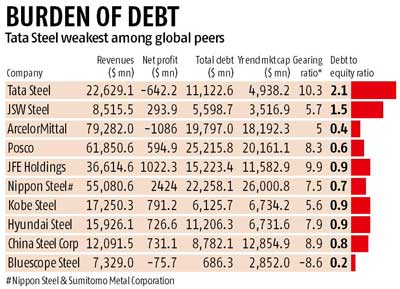

Tata Steel is more vulnerable as it is one of the world's most indebted steel makers and the group's overwhelming dependence is on its profitable operations in India to fund losses abroad. At the end of FY15, its consolidated debt was twice the equity (or net worth), and much higher than the industry average of 70 per cent. At 10, the company's gearing ratio (debt to operating profit) is also among the highest in the industry.

For the better part of the past seven years since 2007, when the Lehman crisis pushed Europe into recession, Tata Steel has been sustaining its loss-making global operations using cash from its profitable operations in India, besides some help from its parent, Tata Sons.

In FY15, Europe accounted for nearly 60 per cent of Tata Steel's consolidated revenues in FY15, while Indian operations were a third and the rest came from its operations in Southeast Asia. Tata Steel India, however, accounted for 80 per cent of the company's operating profit on a consolidated basis in FY15.

The company did not reply to an email questionnaire sent by the Business Standard.

The Chinese slowdown is now hitting Tata Steel's operations in India and Southeast Asia. "In the past, we only used to worry about the financial troubles of Tata Steel Europe, but it now faces headwinds (challenges) in Southeast Asia and India. This has complicated things for the company," says a steel analyst with a local brokerage firm on the condition of anonymity.

On the brighter side, Tata Steel Europe is showing signs of a revival on the back of growth recovery in the European Union. Tata Steel Europe reported higher operating profits in all the four quarters of FY15 over the previous year, despite a small decline in revenues in India and Southeast Asia. A good show by Tata Steel Europe will lessen the blow from the profit decline at its Indian operations and losses in Southeast Asia. Margins per tonne in Europe were, however, a third of that in India.

In FY15, Tata Steel South East Asia reported operating losses in all four quarters against profits in the previous year. The outlook is not bright either due to a spike in cheap imports from China, which accounts for half the world's steel production capacity. Chinese steel demand was down 4.2 per cent in FY15, forcing manufacturers there to dump their produce abroad as Southeast Asia is just the next door.

China's steel export was up 53 per cent in FY15 to an all-time high of 101 million tonnes, according to Tata Steel figures. This is more than what India consumed last year.

A bigger worry is the decline in the profitability of Tata Steel India. "Indian operations reported the lowest earnings before interest, taxes, depreciation, and amortization (Ebitda) per tonne in a decade, partially because of disruption in captive ore supply," wrote Bijal Shah of India Infoline, while analysing the company's results for the March 2014 quarter. Profits were also hit by an uptick in mineral royalty due to the recently-enacted Mines & Mineral (Development & Regulation) Act.

Steel imports doubled to seven million tonnes during FY15, accounting for nearly a 10th of the metal consumption in the country. "Relative stability in the rupee has made imports, especially from Russia, competitive," cautioned the Tata Steel management.

In all, Tata Steel India's net profit was down 23 per cent in FY15, falling to the lowest in seven years. Poor profitability in India will make it tough for the company to sustain losses in its foreign subsidiaries.

Now all hopes are hinged on a demand revival in Europe and incremental revenues and profits from its soon-to-start plant at Kalinganagar in Odisha. The first phase of the three million-tonne unit will increase Tata Steel India's capacity by a third and help it close production and revenue gap with market leader JSW Steel.

"As profit margins are much higher in India than either Europe or Southeast Asia, incremental revenues and profits from the Kalinganagar project will cushion the losses from abroad," says an analyst with a local brokerage on the condition of anonymity.

This, coupled with the expectation of a demand recovery in Europe, has made many analysts turn bullish on the stock. "Tata Steel profits are likely to gain from bottoming out of regulatory woes in India, while their European operations may continue to stay on course for further improvement in operating performance. Capitalisation of the Odisha project should bolster company's return ratios and should also help de-leverage the balance sheet," says Evan Kurtz of Morgan Stanley in a recent report on the company.

Others see some more pain for the company, given the extent of global over-capacity, but remain confident on the firm's ability to overcome this. "Tata Steel finances look stretched but its parent (Tata Sons) has more than enough resources to help the company weather the crisis," says a consultant working with the Tata group.

| Tata Steel Weakest among its global peers | ||||||

| Company | Gearing Ratio* | Debt to Equity Ratio | Revenues | Net Profit | Total Debt | Yr End Mkt Cap |

| ($ mn) | ($ mn) | ($ mn) | ($ mn) | |||

| TATA STEEL | 10.3 | 2.1 | 22629.1 | -642.2 | 11122.6 | 4938.2 |

| JSW STEEL | 5.7 | 1.5 | 8515.5 | 293.9 | 5598.7 | 3516.9 |

| ARCELORMITTAL | 5.0 | 0.4 | 79282.0 | -1086.0 | 19797.0 | 18192.3 |

| POSCO | 8.3 | 0.6 | 61850.6 | 594.9 | 25215.8 | 20161.1 |

| JFE HOLDINGS | 9.9 | 0.9 | 36614.6 | 1022.3 | 15223.4 | 11582.9 |

| NIPPON STEEL & SUMITOMO METAL | 7.5 | 0.7 | 55080.6 | 2424.0 | 22258.1 | 26000.8 |

| KOBE STEEL | 5.6 | 0.9 | 17250.3 | 791.2 | 6125.7 | 6734.2 |

| HYUNDAI STEEL | 7.9 | 0.9 | 15926.1 | 726.6 | 11206.3 | 6731.6 |

| CHINA STEEL CORP | 8.9 | 0.8 | 12091.5 | 731.1 | 8782.1 | 12854.9 |

| BLUESCOPE STEEL | -8.6 | 0.2 | 7329.0 | -75.7 | 686.3 | 2852.0 |

| Tata Steel India vs rest of the world | ||

| (Rs Crore) | ||

| Tata Steel India** | RoW | |

| FY08 | 4550.7 | 3007.1 |

| FY09 | 5201.74 | 2641.9 |

| FY10 | 5046.8 | -7534.8 |

| FY11 | 6410.58 | 343.2 |

| FY12 | 6349.28 | -959.5 |

| FY13 | 5464.35 | -11639.8 |

| FY14 | 6505.77 | -2897.6 |

| FY15 | 5008.21 | -7572.5 |

* Gearing Ratio is total debt divided by operating Profit

** Numbers refer to Tata Steel Standalone figures

RoW: Rest of the world; the difference b/w consolidated and standalone numbers

Source: Bloomberg, Capitaline

Compiled by BS Research Bureau