"Bad debt recovery may get PSU muscle")

The Banks Board Bureau has proposed a deadline for promoters of debt-laden companies to sell their assets for paying off loans to public sector banks. Under the proposal, given to the finance ministry, promoters who have agreed to sell their assets to pay off loans will receive counter-offers from public sector companies. These offers will have the backing of public sector lenders.

The counter-offers will be the base level price at which the assets will be bought out by the public sector companies within a specified timeframe. Promoters will have to sign on the dotted line unless they are able to work out a deal with a third party within the deadline.

“It is a bit drastic but makes sense,” said a government official. The finance ministry is considering the proposal.

To make the proposal foolproof, the seven-member Bureau has also got in-principle clearance from the two anti-corruption agencies of the government — the Central Vigilance Commission and the office of the Comptroller and Auditor General.

The Bureau has made the suggestion to the finance ministry in respect of a Mumbai-based business group which has become one of the largest defaulters. The group, with interests in oil and power, has been in talks with potential buyers for quite some time but with no results. “The deadline that will be mutually agreed upon by banks and the buyer will not allow the non-performing loan to continue on the books of the banks indefinitely,” a source familiar with the developments said.

“One of the power plants with the group is rather new and can be turned around soon,” the source said. Once the plant comes into the hands of a public sector entity, the bankers will have a larger degree of comfort with the turnaround plan, he added.

When contacted, Vinod Rai, the head of the Bureau and the former Comptroller and Auditor General of India, declined to comment. Among other things, the Bureau’s mandate is to help banks develop strategies to raise capital through innovative financial methods and instruments and also steer eventual consolidation. Its members include Anil Khandelwal, a former chairman of Bank of Baroda; HN Sinor, a former joint managing director of ICICI Bank, and Roopa Kudva, a former managing director of rating company CRISIL. Then, there are three ex-officio members — N S Vishwanathan, a deputy governor of the RBI; Anjuly Chib Duggal, secretary, department of financial services, in the ministry of finance; and Ameising Luikham, secretary, department of public enterprises. Sections within the government and the Reserve Bank of India suspect that several business groups have been delaying sale of assets in the hope that the banks would go slow on bad loan recovery.

| PLUGGING THE LOOPHOLE |

|

The latest proposal gives banks an option to deal with errant promoters who have massive dues but whose assets can only by seized by invoking the Sarfaesi Act or, in the case of delinquency, by invoking the recently promulgated Insolvency and Bankruptcy Code, 2016. The formula offered by the Bureau will instead offer a buyout of a sound asset as a going concern but within a timeframe. Since the only alternative is to pay up, the Bureau reckons it can be used wisely to unlock idle investments and make other business houses see reason to hasten their sale of properties.

Naresh Makhijani, head of financial services at KPMG said there is no legal problem if a public sector company wants to step in. “After all, if the board of a listed public sector company feels the asset sits well within the company’s plans, there should be no hitch.” He, however, added that such a proposal would be more like ‘writing on the wall’ for the promoters who have been delaying asset sales.

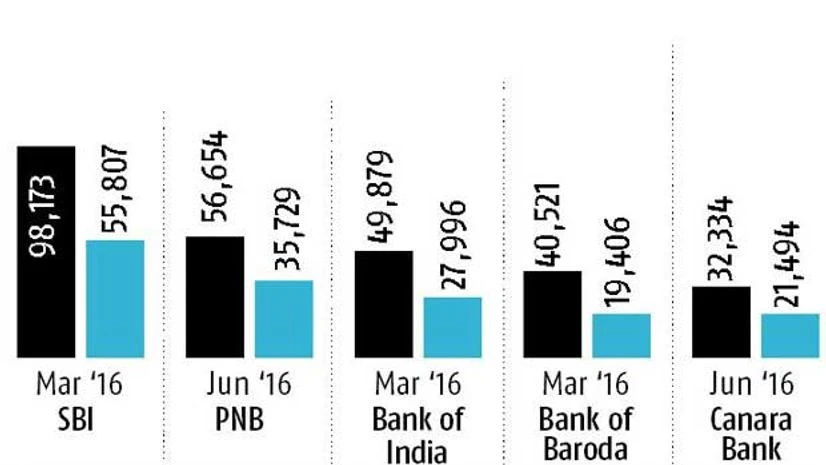

By current estimates, the total bad loans or NPAs of Indian banks are about Rs 6,00,000 crore. An India Ratings report dated July 19 notes, “the current capital position of ARCs (asset reconstruction companies) can at most take care of 10 per cent of the bad debt in the Indian banking system”. The company quoting its parent Fitch Ratings observes: “Currently, India is classified as a Group D country by Fitch Ratings with 30-50 per cent recoveries expected given the level of creditor-friendliness of its insolvency regime.”