"Broad-based revival in investment cycle remains elusive")

If data published by the Department of Industrial Policy and Promotion is anything to go by, there is little evidence to support the government's claim of a revival in the investment cycle.

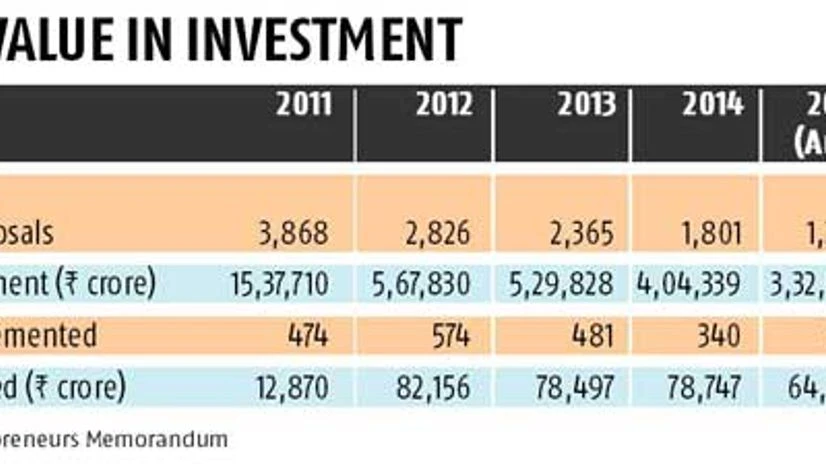

Actual implementation of projects filed through the Industrial Entrepreneurs Memorandum (IEM) in the current year (January-August) stood at a mere Rs 37,915 crore against Rs 64,276 crore over the same period in the previous year. This is a fraction of the peak of Rs 82,156 crore registered in 2012.

What is equally worrying is that proposed investments by industry have also fallen precipitously. Total proposed investment filed through IEM in the current year (JanuaryAugust) fell to Rs 2,36,423 crore from Rs 3,32,441 crore the previous year - a decline of roughly Rs 1 lakh crore. For the current financial year from April to August, CARE estimates that proposed investment is actually lower at Rs 1.48 lakh crore as against Rs 2.34 lakh crore the previous financial year.

While the government may well argue that several policy initiatives have improved the business climate, on the ground a broad-based revival in the investment cycle remains elusive. With demand continuing to remain subdued, the task of reviving the investment cycle is proving harder than anticipated.

Analysts contend that an immediate turnaround in the investment cycle is unlikely with a combination of factors holding back investments. While government capital expenditure (capex) has been ramped up in the current financial year, "the recovery in infrastructure remains limited to a few select sectors such as roads, railways and power transmission," says Aditi Nayar, senior economist at ICRA.

"On the private sector side, over-leveraged firms are holding back from launching fresh investments. Banks are also reluctant to lend as they are trying to repair their badly bruised balance sheets. Thus, chances of a meaningful revival on the private side seem low in the near term," says Devendra Pant, chief economist at India Ratings & Research. The hope that public sector investments would crowd in private sector investments does not seem to have materialised yet.

Concerns are also being voiced that the government's task of reviving the investment cycle could prove to be more difficult in the coming year. "The looming fiscal impact of the implementation of the recommendations of the 7th Central Pay Commission is likely to squeeze the fiscal space available to support a sharp growth in capex from the Budget in the coming financial year," says Nayar.

Add to this the outflow from government coffers on account of the implementation of the One Rank One Pension scheme and the fiscal space could potentially shrink further. This suggests that the availability of funding from extra-budgetary sources such as the national investment and infrastructure fund would be crucial to support a pick-up in investment activity. But it is doubtful that funding from these sources can be quickly ramped up to make up for the expected slack in government spending.

On the other side of the equation, household demand continues to sputter. Reserve Bank of India's own surveys show that capacity utilisation rates continue to hover around 75 per cent. With subdued demand, debt-laden companies are shying away from launching fresh investments as any sudden increase in demand could be easily met by utilising existing capacity. Industry thus, appears to be in a wait-and-watch mode.

According to economists, household demand could potentially get a fillip from three distinct sources in the near term. One, the sharp decline in inflation, which, if sustained, will boost real household incomes, increasing their capacity to spend on other items. Two, the transition towards a low interest rate regime could potentially trigger greater spending on interest sensitive items such as consumer durables and real estate. Three, a boost to household incomes via the implementation of the 7th Pay Commission could spur consumption.

But the impact of these sources on spurring household consumption is bound to vary. While the first two factors are already playing out and are likely to impact consumption over the medium term, there is hope that recommendations of the Pay Commission, if implemented in a timely manner, could improve household liquidity, thereby boosting demand in the short run. Nayar believes that the Pay Commission will have a "positive impact on sales of various consumer durables such as small cars, two-wheelers etc."

But, according to Pant, this time around the impact of the Pay Commission may not be of the same magnitude as that of the 6th Pay Commission. Last time a delay in implementation meant that arrears of two years had to also be paid. This put considerable amount of money in the hands of government employees which gave the economy a significant boost. But this time around, Pant believes that the government is not likely to take more than 4-5 months to implement the panel's report. This implies that the stimulus may not be of the same magnitude. Unlike last time, the Pay Commission bonanza may not be a tide that lifts all boats. Economists are therefore, ruling out a quick turnaround in the investment cycle. A broad-based revival in all probability will be a long protracted process.