"UDAY hinges on structuring of discom debt takeover")

Ninety per cent of the power distribution loans may be on course to being restructured, but the success of the Centre's ambitious Ujwal Discom Assurance Yojana (UDAY) scheme hinges on the manner in which the debt of power distribution companies (discoms) is eventually transferred to the state governments. Besides, banks will need to take a haircut despite UDAY's objective of bailing them out.

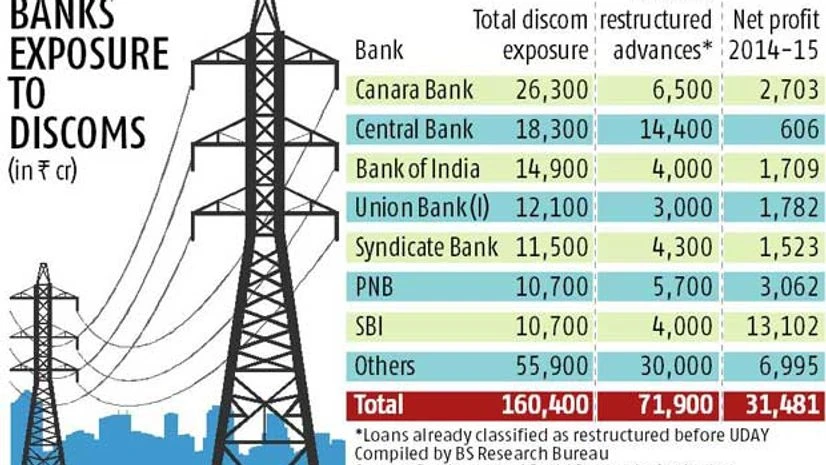

The situation is likely to be further complicated because the Reserve of Bank of India (RBI) is treating the balance debt as non-performing assets (NPAs). This will require banks to make higher provisions. "If this happens, banks will not benefit much from the discom restructuring plan. Banks will not be getting their money right away, but if 25 per cent of loans - roughly Rs 1 lakh crore - become NPAs, the banking sector will be under stress," said chairman of a bank who did not wish to be named.

Impact on state finances

Concerns have been voiced that this debt take-over will cause deterioration in the fiscal health of states. The impact will, however, be determined by whether the states convert the discom debt into equity and issue bonds against it or convert the debt to a loan from the state government.

Rajasthan is saddled with discom losses of Rs 80,000 crore, the highest in the country. Assuming the state takes over 75 per cent of the discom debt, as prescribed by the scheme, its fiscal deficit is expected to rise by 0.5 percentage points to 3.5 per cent in 2015-16 and by another 0.25 percentage points in 2016-17. Thus, by taking over 75 per cent of the debt, the state will breach the relaxed Fiscal Responsibility and Budget Management (FRBM) level set by the Centre at 3.25 per cent.

Officials said the memorandum of understanding (MoU) for UDAY provided innovative options to solve the breach of the FRBM target. The MoU template reviewed by Business Standard provides states with the flexibility to take over discom debt through loan, equity or grant.

According to analysts, most states will prefer to take over the debt in the form of a loan, in which case discoms will continue to pay interest to state governments, although at a lower rate. So, in those cases, a part of the states' interest payment will be covered by discoms, thereby lowering their fiscal deficit.

Senior power ministry officials confirmed this and added, "States that are not financially strong can take over the liability of the discoms in the form of a loan." Discoms, though, will prefer equity or grant as they will not have to make interest payments to state governments. In such cases, the state's fiscal deficit will be affected by the interest burden. Thus through innovative financial engineering - a combination of loan, equity and grant - states can lower their fiscal deficit, according to one official.

Further, the principal amount of the loan is not likely to be included in the fiscal deficit. "Typically, these bonds are paid back on maturity and there is no amortisation. So to that extent this will not figure in the state's fiscal deficit calculations, only the interest payments will," said Rajat Bahl, director, CRISIL Ratings. State governments will have to make separate provisions for repaying the loans.

To join UDAY, states are required to sign a tripartite agreement or MoU with the Union power ministry and discoms. "It is an invisible circle of the same debt. When discoms clear their books, they can look to the same agencies buying these bonds to finance them. The loan extended by the bank goes back to them," said a senior power ministry official seeking anonymity. Discoms can approach banks for fresh financing after meeting stipulated criteria as signed in the MoU.

Apart from existing lenders, Life Insurance Corporation (LIC) and the Employees Provident Fund Organisation (EPFO) have also expressed interest in buying bonds issued by states. An EPFO official confirmed its willingness to buy bonds, saying it was an active player in the state development loans (SDL) market.

Impact on discoms

For discoms, UDAY is an opportunity to clear their books and improve their technical and commercial efficiency. As interest costs are a drag on their balance sheets, removing them will improve their financial position. According to ICRA, the transfer of debt will lead to a relief in the cost of supply of about 50 paise per unit on an all-India basis by 2017-18. Add to this the benefits on account of the reduction in transmission losses and rationalisation of coal supplies and the savings are immense.

While the power ministry has projected transmission losses will come down to 15 per cent by 2019, this assumption is unrealistic, according to experts. ICRA assumes a one per cent reduction in transmission losses and savings of 24 paise by 2017-18. Add another 20 paise on account of rationalisation of supplies and the total reduction in cost works out to 90 paise. Despite this, discoms are still likely to be in the red as the gap between revenue realisation and cost of supply was higher at around Rs 1.15 per unit in 2013-14. This means these measures will have to be accompanied by necessary tariff hikes.

Thus, in addition to lowering distribution losses, "adequate and timely tariff revisions by SERCs (state electricity regulatory commissions) as well as timely and adequate subsidy releases by state governments remain extremely important for a sustainable turnaround in the financial position of state-owned distribution utilities," said Girish Kumar Kadam, vice-president of ICRA.

This is where the UDAY scheme runs the risk of being derailed. Political compulsions to provide subsidised power could likely cast a shadow on efforts to turn the discoms around.

Impact on banks

From the banks' point of view, the conversion of discom debt into state loans removes the uncertainty associated with repayment. "While the bonds issued are at a lower interest rate, the repayment uncertainty comes down," said Bah of CRISIL Ratings. But as existing loans to discoms have been extended at 13-14 per cent interest, banks are likely to take a hit because the restructured loans are likely to be issued at an interest rate of 8.5-9 per cent. Crisil estimates this will hit banks to the tune of Rs 4,300 crore each year. To put this figure in perspective, this loss is roughly 13 per cent of the net profits of exposed public sector banks.

On the flip side, banks will benefit from a one-time provisioning writeback of Rs 5,000 crore on restructured loans being converted into bonds. Further, as the new bonds will be issued by the state governments they will attract zero risk weight, as against 20 per cent now. According to Crisil, this will lower the capital requirement by around Rs 12,000 crore. Senior PSU bank officers said by removing the discom exposure from bank books, the lenders could free up their capital and could expand credit.

Assuming that banks are able to lend Rs 12,000 crore at 13-14 per cent, it will translate into an income stream of Rs 1,500 crore. Thus, the net impact on bank profitability on an annual basis is likely to be around Rs 2,800 crore. But the remaining 25 per cent of discom debt poses a problem. While power ministry officials contended these loans could be easily restructured at lower interest rates, Bahl said, "The remaining 25 per cent of the discom debt poses a challenge from the banks' point of view as it is a riskier asset class but banks do not earn any additional risk premium on these loans."