)

Banks’ decision to lower deposit rates might not augur well for depositors, but it has certainly offered borrowers a reason to celebrate.

“It is only a matter of time. I cannot say when but lending rates will certainly come down. It is not necessary that banks will wait for the next monetary policy (on February 3) before reducing base rates. We might cut our base rate even before (the policy), depending on market conditions,” Ranjan Dhawan, executive director at Bank of Baroda, told Business Standard.

HDFC Bank Managing Director Aditya Puri has indicated the private lender might pare its base rate in the next three months, while State Bank of India (SBI), the country’s largest lender, has hinted that interest rate on select loan products might be lowered before a reduction in the minimum lending rate.

“If deposit rates are coming down, there is no reason why base rates will not come down. Banks may cut lending rates sooner than later, depending on their deposit cost and liquidity position,” said Sidharth Rath, president (treasury), Axis Bank.

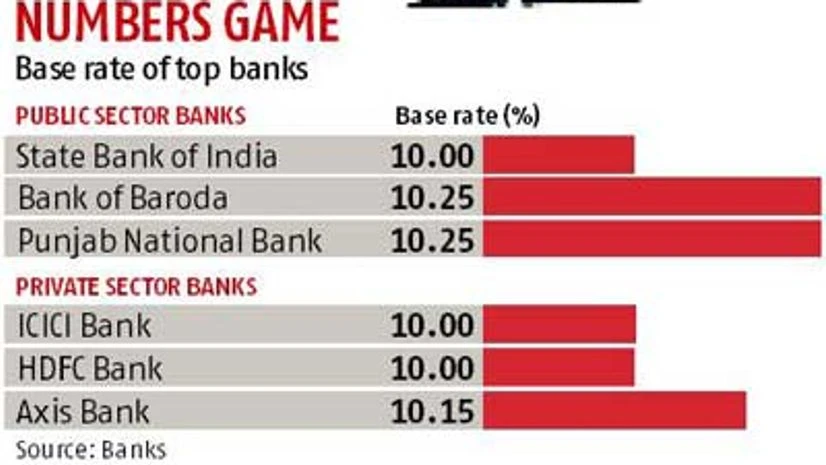

Bankers have always maintained that deposit rates need to be reduced before they can pare their lending rates. With deposit rates now being trimmed, borrowers might not have to wait long for loan rates to fall. SBI has already cut interest rate on select term deposits four times in the past three months. This triggered others, such as Punjab National Bank (PNB), Bank of Baroda, ICICI Bank, HDFC Bank and Axis Bank, to reduce deposit rates selectively since November.

Many, however, also say banks will probably not rush to cut base rates and borrowers might have to wait for a month or two before getting loans at cheaper rates. One of the reasons being deposit rate cuts by most banks have been selective — on certain buckets and not across maturities. ICICI Bank, for instance, has lowered interest rates only on retail term deposits with maturity of 390 days to up to two years by 25 basis points.

Bankers explained that selective deposit rate cuts lead to a marginal reduction in overall cost of deposits and as such, do not offer much room to bring down lending rates. “I believe some of the recent deposit rate cuts were primarily to correct asset-liability mismatches. This will not translate into a lending rate cut, else margins will shrink further. There is definitely a downward bias on lending rates but not many banks will cut base rate before March,” said an executive director of a public sector bank requesting anonymity.“It is only a matter of time. I cannot say when but lending rates will certainly come down. It is not necessary that banks will wait for the next monetary policy (on February 3) before reducing base rates. We might cut our base rate even before (the policy), depending on market conditions,” Ranjan Dhawan, executive director at Bank of Baroda, told Business Standard.

HDFC Bank Managing Director Aditya Puri has indicated the private lender might pare its base rate in the next three months, while State Bank of India (SBI), the country’s largest lender, has hinted that interest rate on select loan products might be lowered before a reduction in the minimum lending rate.

“If deposit rates are coming down, there is no reason why base rates will not come down. Banks may cut lending rates sooner than later, depending on their deposit cost and liquidity position,” said Sidharth Rath, president (treasury), Axis Bank.

Bankers have always maintained that deposit rates need to be reduced before they can pare their lending rates. With deposit rates now being trimmed, borrowers might not have to wait long for loan rates to fall. SBI has already cut interest rate on select term deposits four times in the past three months. This triggered others, such as Punjab National Bank (PNB), Bank of Baroda, ICICI Bank, HDFC Bank and Axis Bank, to reduce deposit rates selectively since November.

Many, however, also say banks will probably not rush to cut base rates and borrowers might have to wait for a month or two before getting loans at cheaper rates. One of the reasons being deposit rate cuts by most banks have been selective — on certain buckets and not across maturities. ICICI Bank, for instance, has lowered interest rates only on retail term deposits with maturity of 390 days to up to two years by 25 basis points.

Then there is the lag effect. “It is not as if I cut deposit rates today, my cost of funds will fall tomorrow. There is a lag. Base rate is calculated through a transparent mechanism taking into consideration banks’ cost of funds. Once cost of funds falls, base rate will also come down,” said Rakesh Sethi, chairman and managing director of Allahabad Bank.

Bankers are also not sure if a lending rate cut will lift the loan demand. The year-on-year growth in non-food credit moderated to 11.2 per cent (its lowest level since June, 2001) at the end of September 2014, putting stress on banks’ margins. High interest rates coupled with uncertain macro-economic environment and availability of non-banking funding sources have made corporate groups reluctant to borrow money from banks.

Analysts believe banks will start reducing lending rates once they are confident of the revival in loan demand.

“The decrease in cost (following deposit rate cuts) will happen gradually. Since the credit demand has not picked up, lowering base rate now will lead to further in erosion in margins, which are already under pressure. I believe loan rates will fall but not in this month,” said Dhananjay Sinha, head of institutional research, economist and strategist at Emkay Global Financial Services.