)

The financial results of the just completed December 2014 quarter, compiled by IndiaSpend, point to a worsening crisis in India’s public-sector banks.

This crisis—caused by ballooning unpaid loans from sectors supposed to revive India’s economy—is not just an indicator of continuing economic woes, but a warning that the means of revival are being further damaged.

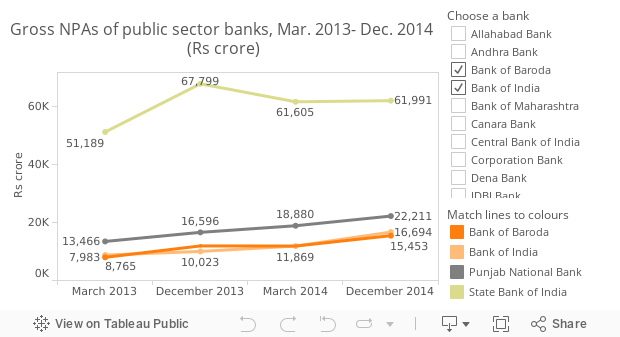

Bad loans, termed Non-performing Assets (NPA), already high in March 2014, have risen 20% over the past nine months in India’s public-sector banks (refer table below), which account for 72% of all commercial lending in India.

Indiaspend has highlighted this issue in the past, and the problem has since worsened.

Gross NPAs, or loans that have gone bad, add up to Rs 2.73 lakh crore ($44 billion) for public-sector banks.

The picture would be much worse if not for corporate debt restructuring (CDR), which usually involves tinkering with interest rates and repayment periods, to help companies in temporary financial distress. A loan under CDR is not grouped with NPAs.

The total value of loans in CDR stood at Rs 2.72 lakh crore ($43.9 billion) in December. Most of the outstanding loans under CDR, are from public-sector banks.

Put together, NPAs and CDR, amount to Rs 5.45 lakh crore ($87.9 billion).

Gross NPAs for public-sector banks stood at 5.33% of their total outstanding loans in September. The value of NPAs has since gone up, so this ratio should have also worsened.

The government says that infrastructure (including power, telecom, airports, roads, ports & rail), iron & steel, textiles, mining and aviation “contribute significantly to the level of stressed advances”.

Source: Bank financial statements, IndiaSpend research

Five sectors—infrastructure, iron & steel, power, textiles and construction—account for 64% of all loans currently under CDR.

Why the torrent of bad loans is a bad sign

The high levels of NPAs indicates that India’s economy is not in great shape, and the recent upward revisions in India’s GDP growth should be taken with a fistful of salt.

The weak balance sheets of public-sector lenders imply that their ability to give out loans may be reduced, with implications for national economic recovery.

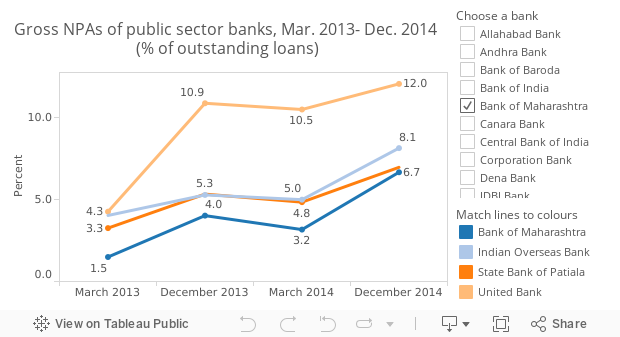

Of 26 public-sector banks (nationalised Banks and the SBI Group), 19 reported Gross NPAs of 5% or more in the latest quarter (refer table below).

Source: Bank financial statements, IndiaSpend research

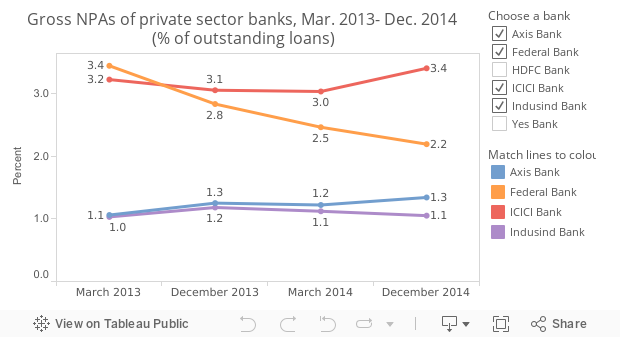

In comparison, private-sector banks seem to have done a much better job of managing risks: gross NPAs for all private sector banks together were 2.05% in September. For the December quarter, the six largest private-sector banks have NPAs ranging from 0.42-3.4%. (refer table below).

Private-sector lenders operate in the same space under the same economic factors as the public sector banks. Emulating their risk-management practices would appear to be top priority for government banks.

Source: Bank financial statements, IndiaSpend research

These bad loans represent a financial setback for India at three levels.

First, the bad loans represent a financial loss to shareholders; the Government of India is the majority shareholder in all these banks, therefore, this is an indirect loss to all citizens.

Second, banks are supposed to maintain sufficient capital to absorb business losses, such as these NPAs. High NPA levels eat up into the capital of these banks, restricting their ability to make additional loans.

Third, to grow, banks need to raise fresh capital. High levels of NPAs mean weak fundamentals and poor valuation in the stock market, hurting their ability to raise funds for growth. This, again, means insufficient capital to make additional loans.

If the ability of public-sector banks to lend freely is impaired, there is likely to be an impact on the larger economy, which is gearing up for a big round of private and public spending to boost growth.

Yet, countries that tried to borrow and spend their way out of trouble have likely failed in these expensive stimulus efforts, as this warning from economist Ruchir Sharma explains.

“A stimulus mindset is the opposite of a tough reform mindset, and governments can rarely do both as the contrasting experience of the 1990s showed,” wrote Sharma. “By the end of that decade, most emerging nations had no money to burn, no lenders they could turn to. They were forced instead to reform, cleaning up bad debts and pushing to make companies more competitive.”