"Analysts upbeat on UPL stock")

Recent upgrades from foreign brokerages have helped the stock of UPL, maker of agro-chemicals and other chemicals, add to its gain over the past three months. The scrip has risen 22 per cent in this period.

Analysts believe there could be more re-rating, on account of lower competitive pressure in key global markets, due to ongoing consolidation. The recent Bayer-Monsanto global deal is an example. Further, market share improvement and growth in Brazil, a key market, should help strengthen its revenue and earnings growth profile.

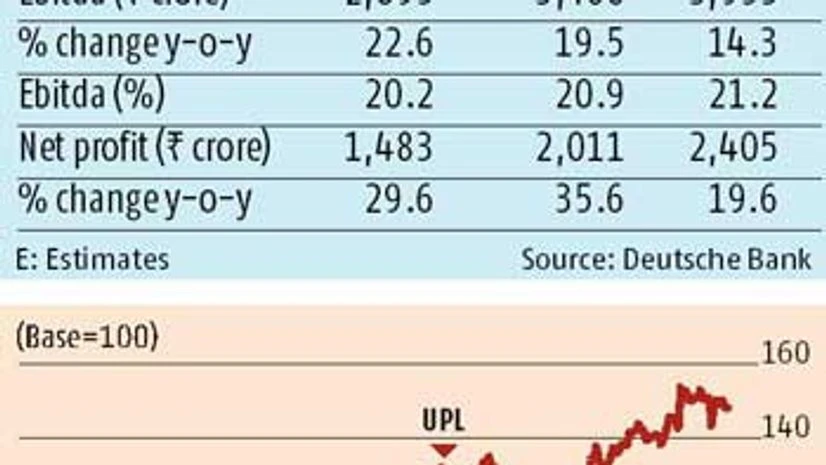

Morgan Stanley, HSBC, Citi and Deutsche Bank believe, given the triggers, that there is more outperformance in the stock, up 50 per cent over the past year.

Deutsche Bank analysts expect Brazil revenue (a fifth per cent of UPL’s consolidated revenue) to grow by 50 per cent in FY17. The soyabean acreage in Brazil, according to the US department of agriculture, is expected to rise by 3.3 per cent and the price of soy is up 14 per cent for the year-to-date period. Further, the Brazilian currency (the real) has seen a sharp 21 per cent year-to-date appreciation as compared to last year, a further positive.

The company’s agrichem portfolio, especially Unizeb, which has been a huge success, should help it gain market share in this geography. In FY16, the performance in Brazil of 84 per cent revenue growth, helped the company post double-digit growth at the consolidated level.

The company is also focusing on increasing the share of new products to over 15 per cent this year. Sales from products launched in the past five years have increased from 2.5 per cent of total revenue in FY14 to 14 per cent in FY16. Further, the share of high-margin branded products in revenue had increased to 85 per cent in FY16 from 79 per cent in FY14; UPL’s global market share was up by 60 basis points to 3.6 per cent in this period.

In addition to Latin America (including Brazil), the other region expected to deliver double-digit growth for the company is India (19 per cent of overall revenue). Analysts at HSBC expect sales growth in India to be 15 per cent in FY17, led by a good monsoon and above-normal sowing. While the company’s market share is pegged at 14 per cent, just below Bayer CropScience’s 15 per cent, UPL is gaining market share at a faster pace than its larger peer. Given the largely generic nature of the Indian market, the company is gaining market share from smaller generic sellers. HSBC analysts say there will be consolidation in the Indian market as smaller players continue to lose share, due to lack of innovative products and investment in distribution and marketing.

Globally, with $6.5 billion worth of products going off-patent, largely in the fungicide and herbicide space, the company is looking at increasing its product portfolio in these segments. Comparing the situation with that of Indian generic pharma companies which got re-rated by 106 per cent between February 2003 and August 2015 as they started gaining market share globally, Morgan Stanley analysts say UPL is in a similar position. They expect net profit to double and earnings to hit average annual growth of 22 per cent over FY17-19.

While sales growth will come from the Indian and South American markets, margin gains could come from rest of the world, 45 per cent of UPL’s sales and 65 per cent of its operating profit. An improving product mix is expected to help raise its margins by 60-100 basis points over one to two years.

At the current price, the stock is trading at 17.7 times its FY17 estimate. Investors looking at taking an exposure to the unfolding growth of crop protection could buy into this stock on dips, with a holding period of two to three years.