)

“Grasim’s cement (69 per cent of FY14 earnings before interest, tax, depreciation and amortisation, or Ebitda) should benefit from a pick–up in the sector utilisation rates driven by receding capacity surpluses, with an expected demand pick-up. This should drive strong earnings growth for its subsidiary UltraTech Cement,” CLSA’s Vivek Maheshwari and Bhavesh Pravin Shah said.

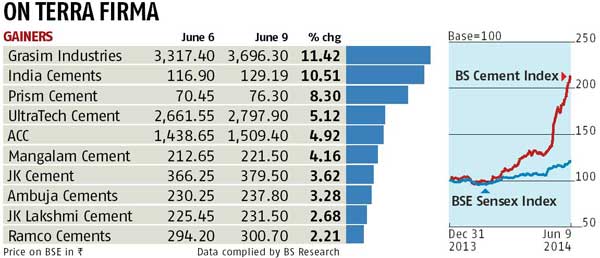

“Margin pressure, with higher capex across key businesses pulled down Grasim’s return on equity to 10 per cent in FY14. The improvement in margins, with higher asset turns, should expand return ratios to 14 per cent over three years. With peak capex behind, we expect Grasim to generate rising free cash flow over FY16-17.” The upmove in cement stocks has been triggered by a price rise reported from south-based companies, which analysts say, can be sustained in case demand improves. Sunil Jain, vice-president – equity research at Nirmal Bang, says: “Capacity addition in the south will be lower compared to the others in two to three years. So if the demand picks up, excess capacity in the south will get absorbed, which will give some pricing power to players. Prices can sustain at these levels and move up.”

Demand dynamics

Analysts expect the weakness in sector growth to continue for six months. Kamlesh Bagmar at Prabhudas Lilladher says the growth bottomed out in FY14, with the demand growth being the lowest since FY02, below the gross domestic product growth.

“In demand, the worst is behind us, with the easing of the sand-mining ban, clarity over the political uncertainty in Andhra Pradesh, the second-largest consumer state, and pent-up demand likely to drive growth. We expect gradual recovery in demand in FY15, with 7.2 per cent compound annual growth over FY15E-17E,” says Ritesh Shah at Espirito Santo Secutities.

Investing strategy

Analysts say one needs to be selective while making a fresh commitment since most stocks have seen a healthy upside. A look at Bloomberg data show many stocks are near or above their one-year target prices. Shah of Espirito Santo Securities retains ‘buy’ on UltraTech and ‘neutral’ on Ambuja Cements. “We have downgraded ACC to ‘neutral’ and Shree Cement to ‘sell’ on expensive valuations. We revise downward our fair value (FV) for ACC due to continued weakness in south. We expect UltraTech to grow on a par with the sector and it remains our preferred pick in the large-cap space.” For Ambuja Cements, Piyush Jain at Morningstar India pegs its FV at Rs 262 a share. Sunil Jain prefers UltraTech, India Cements and Dalmia Bharat in this space.