)

If you were expecting a recovery in the market after a nearly 10 per cent fall in the BSE Sensex in two months, this might come as bad news to you. Corporate earnings have failed to keep pace with the market rise in the past two years, and restoring parity between markets and underlying earnings could require another 10-15 per cent fall in the Sensex.

Despite the recent decline, the Sensex's rise since January 2013 stands at 38 per cent, compared with only 22 per cent growth in the Sensex companies' underlying earnings per share (EPS) during the period. This has created a wedge between valuations and earnings, against a near-parity in the two years before that. In fact, the companies' underlying earnings are down 7.5 per cent from the high reached in September last year.

In the past 25 years (since 1991), there has been a close correspondence between the value of the Sensex and the underlying EPS of its constituent stocks - a correlation coefficient of 0.97. In the past, whenever the market has run ahead of earnings (2006, 2008 and 2010), it has seen a correction.

For some time, the rally has been supported by record dividend payouts by India Inc, as many companies have stepped up their payout ratios to maintain historic buoyancy in their dividends, despite declines in earning growth. For example, mortgage lender HDFC, one of India Inc's top dividend payers, will distribute around 47 per cent of its post-tax profits as equity dividend among its shareholders in 2014-15. This is higher than its five-year average payout of 38 per cent.

Similarly, the country's top cement maker, Ultratech Cement, plans to maintain its dividend outgo in FY15, despite a drop in profits.

Sensex earnings and dividend per share are derived by inverting the index valuation ratios, price-to-earnings multiples and dividend yield provided by BSE.

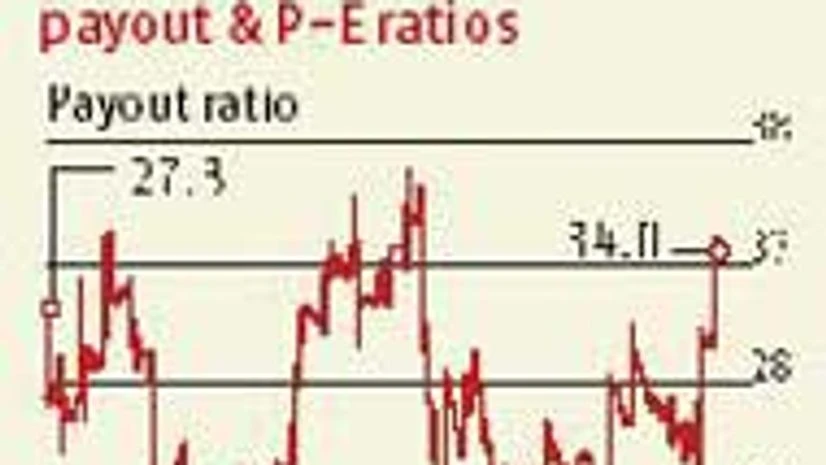

Valuations have also been aided by large special dividend payment by cash-rich companies like Coal India and Tata Consultancy Services. Overall, Sensex companies are expected to distribute a little over a third of their 2014-15 net profit as dividend to shareholders, higher than the 25-year median payout of 26.5 per cent.

Historically there is a 96 per cent correlation between the Sensex and underlying growth in dividends per unit of the index. Currently, one unit of the Sensex provides dividend income of Rs 459 and translates into a yield of 1.7 per cent.

In the past five years, dividend payout by Sensex companies has grown at a compound annual rate of 18.7 per cent, at double the pace of growth in earnings (9.8 per cent) during the period.

This has resulted in dividends keeping pace with the rise in valuations at Dalal Street and more than compensated for lower-than-expected profit growth.

Analysts, however, say it's tough to sustain buoyancy in dividends without a matching growth in earnings. Not surprisingly, many analysts find market expensive, even at current levels.

"If you consider the underlying growth and earnings, the market is still quite expensive. Despite the recent fall, the market is discounting a far higher GDP (gross domestic product) growth and corporate earnings than what seem plausible in the current context," says Dhananjay Sinha, head of institutional equity at Emkay Global Financial Services. He expects the Sensex companies' earnings to grow 5-7 per cent in 2014-15 and 2015-16, much lower than market expectation of 15-20 per cent.

At its current level, the Sensex is trading at 20 times the combined 12-month trailing earnings of its constituent companies, higher than its 25-year median valuation ratio of 18.5 times.

The trajectory suggests the earning upside that India Inc got from the rupee's depreciation in 2013 and early 2014 has stalled; a relatively strong rupee is now hurting India Inc. "For a while, defensives and export-intensive companies supported corporate earnings. But a negative earning surprise from IT exporters has turned the table," says G Chokkalingam, founder & chief executive, Equinomics Research & Advisory.

A market rally from here will require earning support from domestic demand and investment-related stocks like capital goods makers, power generators, public-sector banks, metals & mining, cement, oil marketing companies and telecom firms.

Bulls are hopeful of this happening sooner than later. "Manufacturing and cyclical companies have reported encouraging results during the March quarter so far, and future outlook is positive. I believe the market has bottomed out and it will bounce back by at least five per cent from its current level," says Chokkalingam.

Bears might, however, look for the first whiff of bad news - whether it's poor corporate earnings or global macro headwinds - to try and push the market to fresh lows.