)

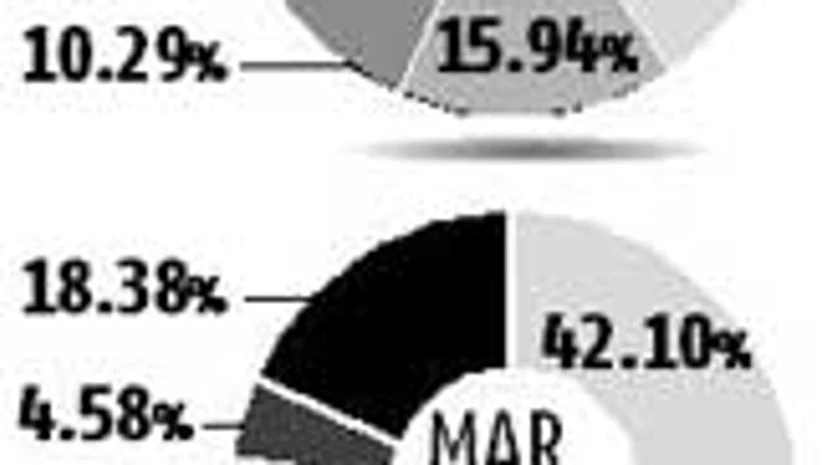

Foreign institutional investors (FIIs) have continued to remain bullish on the Narayana Murthy-led Infosys, taking their holdings to record levels, despite a weaker revenue forecast for the financial year 2013-14. During the recently concluded March quarter, these investors raised their holdings in the software major by 145 basis points (bps) to 42.1 per cent, an all-time level. This has come amid a lesser financial performance and continued high-profile exits at the top and middle level management at Infosys.

The number of FIIs with shareholding in the company rose to 984 from 897 at the end of the December 2013 quarter, shareholding data on exchanges showed. FIIs have increased their holding in the company by nearly 300 bps since the Infosys board appointed N R Narayana Murthy as executive chairman in June 2013. At the end of the June quarter, they’d held 39.55 per cent stake. On the other hand, the shareholding of India-based mutual funds and insurance companies has declined by about 200 bps during this period.

Analysts said the exits of nine top-level employees in the second half of 2013 could have a bearing on Infosys’ performance in the medium term.

The company itself indicated it could miss the top end of its 2013-14 revenue growth forecast of 12 per cent. The company has underperformed its larger peer, Tata Consultancy Services’ (TCS) financial performance consistently in the past. The Infosys stock trades at a steep discount (nearly 20 per cent, to 15.4 times the 2014-15 estimated earnings) to TCS (19 times FY15 estimated earnings).

In the March quarter, Infosys shares fell six per cent, underperforming the benchmark Nifty, which rose 5.7 per cent.

However, most analysts remain positive on the stock (given the low valuations). Of the 16 analysts polled by Bloomberg in April so far, 11 have a ‘buy’, four have a ‘hold’ and one brokerage has a ‘sell’ rating on the stock. Their average target price is Rs 3,801 a share, a 16.9 per cent upside from Wednesday’s closing price of Rs 3,253.

Shashi Bhusan, an analyst with Prabhudas Lilladher, remains confident of an improving demand environment and an increased focus by Infosys to win large deals. He expects this to start yielding results in FY15 and retains a ‘Buy’, with a target price of Rs 4,550.

Analysts at JP Morgan maintain an ‘Overweight’ rating on the stock, with a December 2014 price target of Rs 4,000.

“We continue to believe Mr Murthy’s diagnosis of Infosys’ problems is fairly accurate. Hopefully, he can also administer the right medicine/solutions, which might just take longer to heal than we expected,” said an analyst in a report dated April 1.