"JSW Energy an outlier in the power space")

In the past five years when most electricity producers saw their market capitalisation erode by 16 to 70 per cent, JSW Energy’s grew 1.45 times. The sector has seen worries aggravate, as demand remained soft and realisations continue to reel under pressure. Thus, in challenging times for the business, stock prices of various producers also faced the heat.

JSW Energy, however, has maintained profitability and has continuously added to capacity. While some experts have raised concerns on its inorganic growth at a time when outlook for the sector remained grim, JSW’s moves have yielded positive results.

For instance, when it announced the acquisition of the 1,391-Mw Himachal-based hydro power assets of JP group in November 2014, some experts had raised concerns on JSW venturing into a seasonal business and not having experience with hydro assets. But, during FY14-16, revenues have risen and profits nearly doubled.

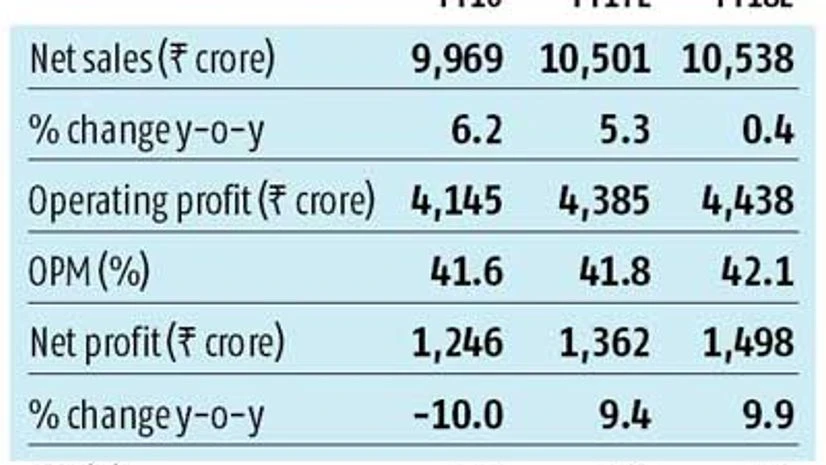

During the June ’16 quarter, too, revenue grew 16.9 per cent year-on-year, to Rs 2,450 crore, aided by increased generation capacity despite lower average realisation of Rs 3.61 per unit vis-a-vis Rs 4.16 per unit in the June ’15 quarter. Net generation increased by 43 per cent, primarily due to hydro power plants acquired in FY16 and improved performance of the Ratnagiri unit, despite shutdown at the Bellary and Barmer plants, due to maintenance and lower demand. Margins grew 669 basis points, while net profit was up 18.7 per cent over a year. Evidence that new capacities have helped drive growth.

During the recent annual general meeting, chairman Sajjan Jindal said the highest-ever net power generation of 22.06 billion units in FY16, as against 20.31 billion in FY15, was primarily driven by acquisition of the hydro power plants (from September 2015).

Analysts, too, seem convinced of JSW’s strategy. Says Misal Singh at Religare Institutional Equities: “JSW Energy has continued to deliver regular growth and there is not much stress on the balance sheet. Its debt-equity that stood at 1.7 in FY12 stands at 1.55 at the end of FY16.”

The growth might continue as JSW improves operational efficiencies and ties some loose ends. Analysts at IDFC Securities, in response to JSW’s acquisition of the 500 Mw Bina (Madhya Pradesh) unit in July, said any tie-up of the balance power will create huge value for shareholders. “In addition, the gearing is likely to be comfortable at below 1.7 times, on completion of the acquisition. And, JSW Energy’s portfolio will be diversified, in terms of geography and fuel.” Thus, they maintained an ‘outperformer’ rating on the stock.

The current capacity is 4,531 Mw — thermal 3,140 Mw and hydel 1,391 Mw. This is likely to reach 6,031 Mw once the two announced acquisitions of JP’s 500 Mw Bina thermal assets and Jindal Steel & Power’s 1,000 Mw thermal assets in Chhattisgarh is completed. The company plans 10,000 Mw capacity by 2020.

Sanjay Sagar, joint managing director at JSW Energy, says: “In our strategy to grow, we have targeted (growth) ensuring normative returns. The company has been selective while taking the inorganic route and has only gone for acquisitions when revenue visibility through Power Purchase Agreements (PPA) was there. The company has given time to JSPL to ensure PPAs before acquisition is complete. Today, we have PPAs for more than half our power production.”

The latest agreement to acquire 500 Mw of thermal assets because of available PPA (70 per cent of produce) has also been looked at in positive light. Analysts at Ambit said the deal would be value-accretive to the extent of Rs 600 crore (Rs 3.7 a share).

However, while analysts remain positive, there are near-term worries, including concerns on a new PPA for it’s most profitable Vijayanagar (Karnataka) plant getting delayed and expectations on rates for new PPAs being lower. Also, integration of the southern grid with the national grid in 2017, might add to the challenges. But, Sanjay Sagar says this year they’d also get the full-year benefit of hydro assets’ integration that will help mitigate any demand softness.

Analysts at Edelweiss say a month’s delay in signing of the PPA will entail a four to five per cent earnings cut, while five per cent higher coal prices will lead to a four per cent cut in FY17 earnings. Coal prices have risen recently and need to be monitored. “At current levels we find the risk-reward balanced and, hence, maintain ‘hold’ ratings,” they add.

Overall, the stock is now trading close its one-year target levels. Long-term investors could consider it on corrections.

MAJOR ACQUISITIONS BY JSW ENERGY

-

Nov 2014: Agreement for acquisition of 1,391-Mw JP hydro assets

-

Sept 2015: Completes acquisition of 1,391-Mw JP* hydro assets

-

May 2016: Agreement to acquire 1,000-Mw of JSPL’s** thermal assets

- July 2016: Agreement for acquiring 500-Mw JP thermal assets

Source: Company