"L&T, BHEL offer glimmer of rebound")

Capital goods production fell 30 per cent in July, a ninth straight month of decline. Since capital goods have 8.8 per cent weight in index of industrial production (IIP), the decline was bound to pull down IIP numbers, raising concerns. Analysts at IIFL said that continuous fall in capital goods production is a worrisome sign. While economists at Religare Institutional Research said capital goods production number has been distorted by a sharp fall in “rubber-insulated cables”, even excluding those, capital goods output rose only 1.5 per cent over year in July. Capital goods are goods such as factory machines that are used for producing other goods.

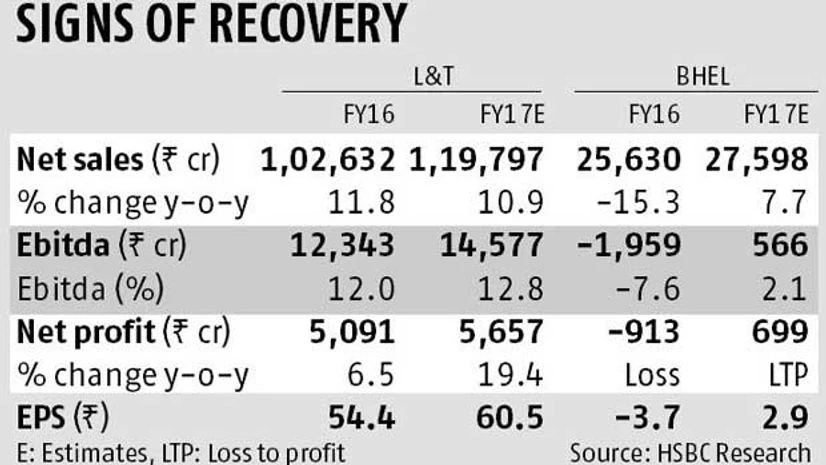

The capital goods sector has seen numerous challenges in execution and slower order inflows, leading to weak growth. The power sector, already having under-used generation capacities due to challenges on demand and realisations, was not providing many fresh opportunities for capital good firms Bhel (Bharat Heavy Electricals Ltd) and L&T (Larsen & Toubro). Also, construction, real estate, infrastructure, and oil and gas sectors remained subdued, adding to challenges for L&T. The country's largest engineering, construction, and infrastructure firm, L&T, had forecast for 15 per cent growth in fresh orders in FY16. However, it had to cut down the forecast to zero-five per cent by end of December 2015 quarter, which it still missed. L&T’s order flow during FY16 declined 12 per cent. Execution of projects (orders in hand) remained lukewarm and L&T ended the year with sales growth of 11.6 per cent and single-digit profit growth of seven per cent.

However, things seem to be changing for the better and weakness in capital goods production should reverse in the next few months. Since November 2015, it has been in negative territory, so at least a low base effect will kick in from November 2016. But the two bellwethers of India's capital goods sector — L&T and Bhel — are also showing signs of recovery.

For FY17, for instance, L&T has forecast for sales growth of 12?15 per cent, order inflow growth of 15 per cent, and operating profit margin improvement of 50 basis points. Although L&T has missed these forecasts in the past, the latest results provide comfort. During the June quarter, it reported sales growth of nine per cent over year and Ebitda (earnings before interest, tax, depreciation, and amortisation) margin improvement of 50 basis points, thereby profits were up 45 per cent over year. Order inflow improved 14 per cent over year to Rs 29,700 crore and execution increased 18 per cent. While this was largely driven by international markets and domestic market remained muted (execution improved only five per cent over year and order inflows were down eight per cent over year), analysts expect improvement in these.

Management attributed revenue growth to a strong focus on executing existing orders. While order inflows remained weak, management is confident of converting 7,000 megawatt (out of 12,000-Mw projects, for which it is the lowest bidder during FY17). Analysts, however, are awaiting sustainability of this performance in coming quarters, even as they have upgraded their forward estimates for Bhel. Analysts at HSBC have revised their execution pace upwards due to a strong June quarter, which has led them to upgrade revenues and Ebitda by 11 and 31 per cent, respectively.

While this performance by capital goods majors is encouraging, L&T and BHEL will have to maintain it in subsequent quarters for the confidence to improve, which should also reflect in better IIP numbers.