"Metals to fall further on oversupply")

Triggered by a sharp decline in global commodity prices since June, Moody's Investors Service has forecast prices of metals to remain weak in 2016. The reasons given are oversupply and subdued demand from China, the world's largest producer and consumer of metals.

Following weak prices, producers might cut production in 2016, which might help prices to rebound in 2017.

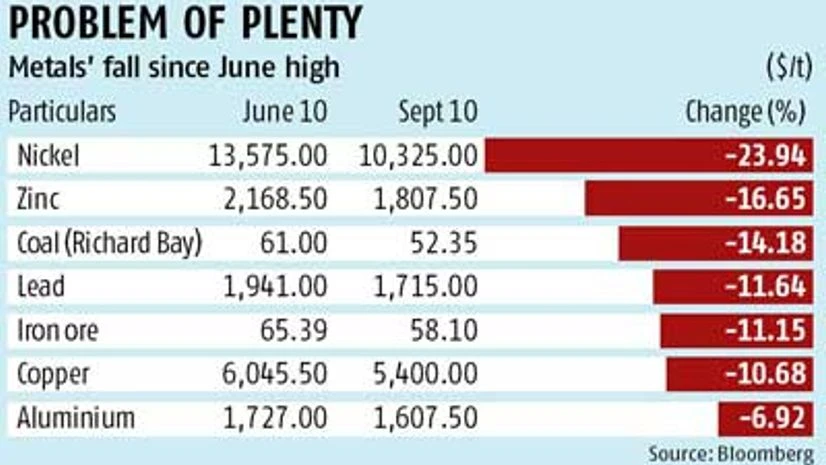

Moody's latest report says the contraction in base metal prices and related commodities, on a declining trend since 2013, has accelerated in recent months. This is dues to a culmination of macro and industry-specific factors. The price of nickel on the benchmark London Metal Exchange fell 24 per cent and of other base metals by up to 17 per cent in the past three months.

The fall in industrial commodities' prices indicate less new investments in infrastructure and housing, which drive industrial growth globally. Continuing of the weak demand trend might ring alarm bells on production and job cuts -a number of global analysts have already forecast this.

China's rate of growth, export levels and infrastructure investment are important drivers in metal demand expectations. Heightened uncertainty as to actual growth rates in China has caused sentiment towards base metals to turn more negative. While prices generally have shown a flat to declining trend since 2013, a more dramatic contraction has been in evidence since June this year, with August seeing significant downward movement.

As China consumes a significant amount of base metal production, growth expectations there and consequent demand for base metals plays a major role in the commodity price movement.

In fact, prices of many industrial commodities have reached their level of cost of production. So, any further fall would lead to cut in production. In fact, global aluminium majors, including India's Bharat Aluminium Company (Balco), are facing the heat of falling demand and thereby prices on oversupply. Consequently, Balco has announced retrenchment of around 1,000 employees.

"Between 20 and 25 per cent of global aluminium producers are currently selling their output with a cash loss. Depending upon their pocket size, they will continue. After that, however, they would have to cut their production, which might trigger a turnaround in global aluminium prices," recently said D Bhattacharya, managing director of Hindalco Industries.

Last month, Moody's revised downward the GDP growth forecast for China in 2016 to 6.3 per cent from the earlier 6.5 per cent. The perceived sharper than expected slowing of that economy, limited supply response from commodity producers, overcapacity in global steel markets, reduced energy costs and a strong dollar are creating unprecedentedly adverse conditions for these commodities, driving prices down to levels close to those seen in the 2008-09 financial crisis but perhaps with more protracted recovery prospects.

"As comparable economic drivers and the importance of China's steel production growth rates also apply to seaborne iron ore and metallurgical (met) coal prices, we have included our price assumptions for these minerals as well. Our base metal price assumptions for 2016 assume that conditions will remain relatively unchanged from current levels, although stabilising on announced and anticipated production cutbacks, while 2017 will show some improvement on a more balanced supply/ demand position and improving global economic fundamentals," said Cowan.

Met coal and iron ore prices have similarly evidenced sharply declining trends. Their price assumptions reflect expectations for a continued slower growth rate in Chinese steel production (down 1.6 per cent year-on-year through July), with further net increases in iron ore supply, which will maintain pressure on ore prices. The modest improvement in met coal assumptions anticipates unprofitable production coming out of the market in 2017.