"Premium valuations of Gruh Finance look sustainable")

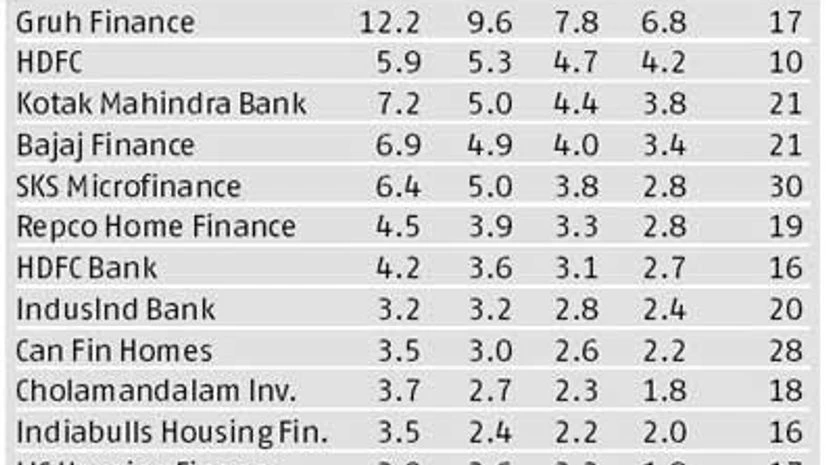

The stock of Gruh Finance, an affordable housing company, occupies top slot in the valuation table of the country’s leading banking and non-bank financial companies. Of the 61 banking and financials’ stocks in the S&P BSE 500, it trades at 7.8 times the FY17 estimated book value (P/BV).

This is not only more than double that of peers such as Repco Home Finance (3.3 times), CanFin Homes (2.6 times) and Indiabulls Housing Finance (2.2 times). It is also visibly higher than the 4.7 P/BV multiple (standalone) of Gruh’s 58.6 per cent parent, Housing Development Finance Corporation (HDFC).

Trading at 4.4 times the FY17 estimated book, Kotak Mahindra Bank figures at the number three slot in this list. Followed by Bajaj Finance at 4 times FY17 estimated P/BV. The top names in this list suggest the Street is rewarding companies with healthier asset quality and high potential to grow their businesses, as well as earnings.

But, Gruh has been the highest valued stock in Indian financials space for FY15 and FY16 as well. Strong earnings growth of 28 per cent in each of the past three years, along with healthy return ratios, has led to a sharp re-rating of the Gruh stock. Notably, its one-year forward price to book ratio has leapt from three times in FY11 to the current level of about eight. Gruh is largely focused on the affordable housing loan segment in western India; its average loan size (smallest among its peers) is Rs 8 lakh. It has a diversified client mix, with a little over 60 per cent of loans given to employees. The company has penetrated over 90 per cent talukas in Maharashtra and Gujarat and is now looking to replicate this penetration in other markets as well.

Are Gruh’s premium valuations sustainable? Analysts seem to think these are. Sunesh Khanna at Motilal Oswal Securities says, “We expect it to continue to trade at premium multiples, due to a track record of financial/operating performance, immense potential of scalability due to massive opportunity in the affordable housing segment, strong parentage of HDFC, best-in-class return ratios, efficient use of capital (no dilution in 10 years) and healthy asset quality.”This is not only more than double that of peers such as Repco Home Finance (3.3 times), CanFin Homes (2.6 times) and Indiabulls Housing Finance (2.2 times). It is also visibly higher than the 4.7 P/BV multiple (standalone) of Gruh’s 58.6 per cent parent, Housing Development Finance Corporation (HDFC).

Trading at 4.4 times the FY17 estimated book, Kotak Mahindra Bank figures at the number three slot in this list. Followed by Bajaj Finance at 4 times FY17 estimated P/BV. The top names in this list suggest the Street is rewarding companies with healthier asset quality and high potential to grow their businesses, as well as earnings.

But, Gruh has been the highest valued stock in Indian financials space for FY15 and FY16 as well. Strong earnings growth of 28 per cent in each of the past three years, along with healthy return ratios, has led to a sharp re-rating of the Gruh stock. Notably, its one-year forward price to book ratio has leapt from three times in FY11 to the current level of about eight. Gruh is largely focused on the affordable housing loan segment in western India; its average loan size (smallest among its peers) is Rs 8 lakh. It has a diversified client mix, with a little over 60 per cent of loans given to employees. The company has penetrated over 90 per cent talukas in Maharashtra and Gujarat and is now looking to replicate this penetration in other markets as well.

Given the smaller base and the huge growth potential, it is not surprising that most analysts expect the loan book to grow at a healthy 25 per cent annually over the next two to three years. One might contest this, looking at the growth in unsold inventories in the larger housing space, forcing developers to go slow on new launches. However, analysts say the affordable housing segment remains an exception. A key reason is the various incentives from the central government, including interest rate subsidy, and the significantly low penetration.

Take the Pradhan Mantri Awas Yojana, where the government aims to provide housing for all by 2022. The aim is to construct three million houses annually over the next seven years for the urban poor. Even if half of this is achieved, it would still mean a significant jump as compared to the 0.9 million houses constructed during the 10 years of the Jawaharlal Nehru National Urban Renewal Mission. Then, individual states have various schemes to promote affordable housing.

In a report, analysts at Antique Broking say, “Small-ticket housing would be the big theme for the next five years, given the huge latent demand and the measures by the government and the regulator to fulfil it.” Gruh Finance and Repco Home Finance, they believe, are well placed to benefit from this and continue to remain their favourite bets in the segment.

Rising competition from existing and new peers, the coming Small Finance Banks, among others, would be a key monitorable. While Gruh's consistent record and strong parentage (handy in terms of best business practices) provide some comfort on this front, analysts believe the company’s net interest margin could soften as it tries to compete efficiently. Analysts on an average expect this metric to remain 4-4.3 per cent; it is now 4.2 per cent.

The other risk is if the company falters on growth expectations, which could substantially hurt the valuations. For now, most analysts remain positive on Gruh and expect the stock to deliver about 17 per cent return from the current level.