)

When Finance Minister P Chidambaram urged Indians to contain their “uncontrolled passion” for gold at a function here last week, he was probably airing his disappointment over the rush to buy the precious commodity in April, despite a price decline. This was the opposite of what many had predicted.

When international gold prices fell 16 per cent in April to $1,348 an ounce, quite a few economists had rushed to lower their estimates of the current account deficit (CAD), the gap between our imports and exports. The logic was that the fall would take away some of the metal’s charm and volumes would decline, too.

The price fall enthused even C Rangarajan, chairman of the Prime Minister’s Economic Advisory Council, to say on April 24 that gold imports would fall 20 per cent in value to $45 billion in FY14, and the CAD would narrow as a result of this.

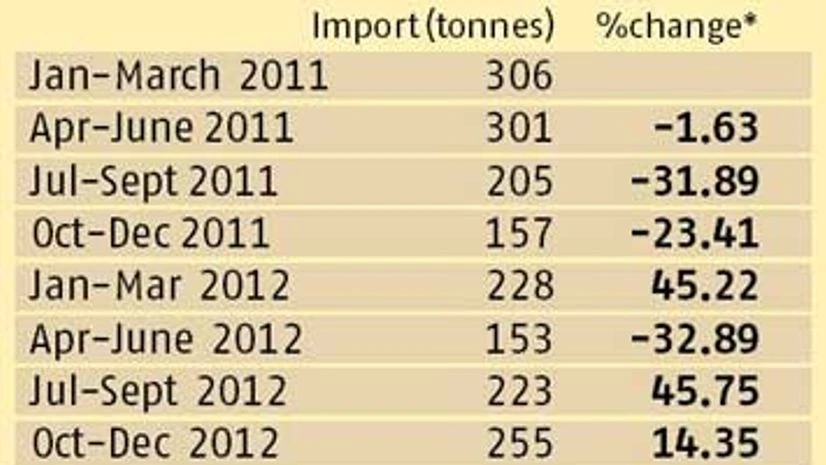

But this has not happened either in investment demand or in the demand for jewellery. The World Gold Council anticipates India’s gold imports to be 300-400 tonnes in the July-September quarter, a 200 per cent year-on-year increase and almost half of total shipments for all of last year. This helped gold prices recover three per cent in May.

Indians have always loved gold but the April figures show how this obsession has spiralled over recent years, taking the CAD to unsustainable levels. Over recent years, the CAD has widened substantially and touched 5.7 per cent of gross domestic product (GDP) in FY13. It touched a record 6.7 per cent of GDP in the third quarter of FY13.

Gold analysts say April’s fall in gold prices might have weakened investment demand but consumption demand has bounced back. Sugandha Sachdeva of Religare Commodities believes investors bought gold thinking it was a great bargain.

Jewellers and retailers were seen accumulating the yellow metal in April, leading to a tight supply scenario and physical premiums were seen rising to multi-year highs in the market, she adds.

Shubhada Rao, chief economist at YES Bank, says Indians have a natural affinity for gold and the fall in prices has fuelled consumption demand. This would result in sustained gold imports in terms of volumes.

<B>No dramatic improvement</B><BR>

Presuming the rupee averages at last year’s levels, the gold import bill would merely decline in value terms by 13 per cent (equivalent to the fall in gold prices) in FY14 so far, to about $50 bn, again not considered sustainable. So, Rao is not expecting the CAD to improve dramatically in the current year.

When it comes to gold, the behaviour of Indian consumers has even defied the rules of price elasticity.

Sinha believes contrary to Rangarajan’s estimates of the CAD falling to 4.5 per cent of GDP, it could be close to five per cent of GDP. Sinha expects India’s gold import bill to be $50-55 bn.

A weak rupee could also wreak more havoc with the CAD, believe economists. If the monsoons are good, then the demand for gold will remain elevated. The central bank seems to be aware of the scenario, which is why it is continuing to tighten norms so that gold imports slow down.

Gold has been the bane of India’s external sector for long now, as imports of the precious metal have risen nearly 115 per cent between 2000-01 and 2012-13. In value terms, gold imports have risen from $4 bn in 2001-02 to $54 bn in 2012-13, translates into a 14-fold rise over a decade.