)

Marico, the hair oil and cooking oil maker, reported lower than expected results for the March quarter on sales, as well as net profit (excluding exceptional items).

While consolidated net profit grew 20.3 per cent over the previous year to Rs 84 crore, excluding the exceptional income of Rs 11.6 crore, net profit was up just one per cent year-on-year, at Rs 72 crore. The total operating income of Rs 999 crore also came in lower than the expectation of Rs 1,058 crore. Lower growth in international business (22 per cent of FY13 revenue) and a 74 per cent fall in its profits to Rs 3.4 crore impacted the consolidated numbers.

Overall volume growth of eight per cent, though, was in line with expectations driven by the fast-moving consumer goods (FMCG) India business. However, even in these, the company saw a slowing in both value and volume growth, compared to the first nine months of FY13. It is now focusing on volumes and had cut product prices under key brands such as Parachute and Saffola by three to eight per cent in March. It hopes the current quarter onwards will bear the fruits of these moves.

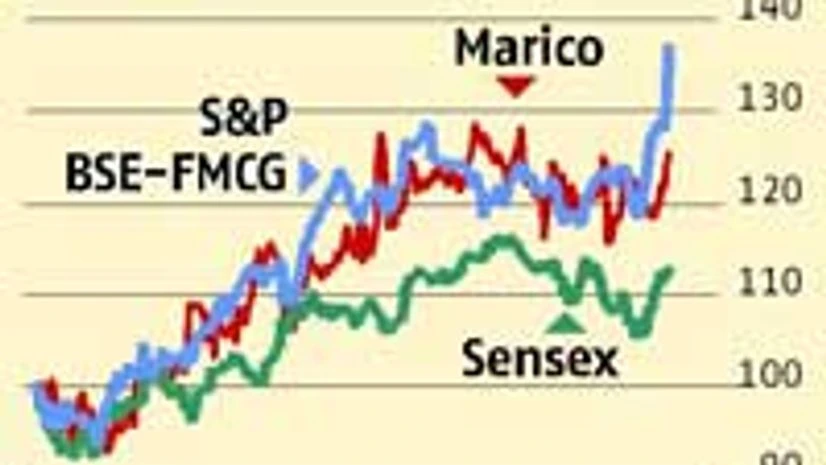

Nevertheless, some brokerages trimmed their earnings estimates after the results. On valuation, too, many analysts believe there is little room for upsides, given the current price of Rs 225.30.

“We trim our FY14 and FY15 earnings estimates by 2.5 per cent and three per cent to factor in lower top line growth and cut our target price to Rs 215 (from Rs 220). Investors can buy the stock on dips to around Rs 190-200 levels. We expect Marico to resort to increased promotions/price cuts to improve volume growth in its key brands, Parachute/Saffola, which could cap margins in the near term,” says Varun Lohchab, FMCG analyst at Religare Capital Markets.

As on May 1, by Bloomberg data, the consensus price target was Rs 235. And, of the 17 analysts who made a recommendation in April, only five have a buy/accumulate rating on the stock; the others have a hold/sell rating.

Marico’s earnings before interest, taxes, depreciation and amortisation (Ebitda) margins remained flattish, despite a decline in raw material prices on a year-on-year basis, as ad spends and employee costs rose. The average price of copra and coconut oil, the key inputs, were marginally down and helped offset the rise in prices of sunflower and safflower oil, up 10 per cent year-on-year. Positively, from the lows seen in October 2012, input prices had run up sharply going into January 2013. However, these have fallen about 10 per cent and have been stable for a little over two months. Taking advantage, Marico has cut prices in key products (especially of Parachute coconut oil, which has seen slower volume growth) to shore up volumes. However, this could hurt its margins.

“Despite excluding the loss-making business of Kaya in FY14, we expect pressure on Ebitda margin during FY14, on account of price cuts on key brands and higher A&P (advertising and promotion) spending (additional 50 basis points of sales) for achieving volume growth. We expect a 50-60 bps year-on-year decline in the Ebitda margin in FY14 as compared to FY13 (ex-Kaya),” says Naveen Trivedi, FMCG analyst at Karvy Stock Broking.

While the smaller contributor, the breakfast category (Saffola oats and muesli) should continue to grow fast. The value-added hair oils (Parachute Advanced, Nihar and Hair & Care, which posted strong volume growth of 24 per cent) are also expected to grow strongly. This segment accounts for a sixth of turnover and earns higher margins; these should support top line growth and margins in FY14. Similarly, Marico’s youth brands (Set Wet, Zatak, Livon ; some acquired in 2012) are expected to clock average growth of around 25 per cent and aid growth.

Although the domestic business outlook appears to be looking up, the international business remains a concern and will take a few quarters to gain pace.