)

With trading up on Nifty futures in the Singapore Exchange (SGX Nifty), translating to a significant loss in the market share for the National Stock Exchange (NSE), a standing council of experts was constituted by the government in 2013 to suggest measures for enhancing the competitiveness of Indian stock markets. While the council is expected to come out with its suggestions shortly, improving of competitiveness and regaining lost market share will involve policy initiatives on a range of systemic issues.

"While there are a number of issues such as capital controls and the taxation framework that the committee could look into, they should also examine the loss of competitiveness on account of trading hours and lower costs incurred in trading SGX Nifty," says a market expert.

On the issue of trading hours, a Kotak Institutional Equities report points out that as Indian market timings do not overlap with US trading hours, SGX Nifty futures is the only hedging tool for market makers in globally listed exchange traded funds (ETFs). In fact, at least 15 per cent of SGX Nifty volumes are recorded after India trading hours.

According to market participants, the other reason SGX is more competitive is the high transaction costs involved in trading in India. Currently, investors trading on Indian stock exchanges incur various costs in the form of brokerage fees, exchange transaction charges, turnover fees, service tax on brokerage paid, stamp duty and securities transaction tax (STT). While some of these charges are towards various services provided by the members and the exchange, others are statutory and regulatory in nature.

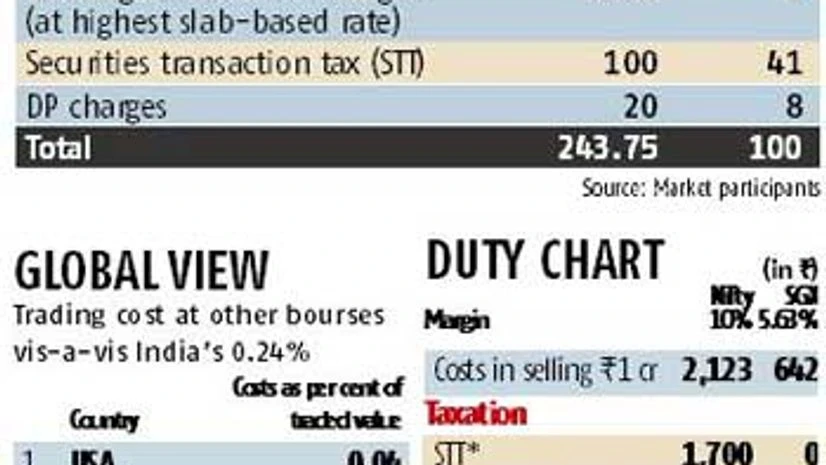

A detailed break-up of the comparative costs incurred in trading reveals the STT, levied at the rate of 0.01 per cent, accounts for a significant portion of the total costs. On a transaction of Rs 1 crore STT works out to Rs 1,000, while all other charges incurred add to Rs 423. Although removing the STT would make Indian markets more cost competitive, market participants feel "while the tax may not go, the committee could suggest lowering the rate". Merely lowering the STT could significantly reduce the cost differential between the markets.

Even in the cash market, trading in India is costlier than in other countries. Globally, the total cost of trading lies in the range of 0.02 per cent to 0.21 per cent of the traded value. In India, according to market participants, trading costs are at the higher end of the spectrum, at 0.24 per cent. Of the total cost, nearly 50 per cent is accounted for by various statutory levies. STT alone accounts for 83 per cent of the total of statutory taxes/levies.

With offshore instrument (SGX Nifty) now accounting for 70 per cent of cumulative open interest across both exchanges, according to the Kotak report, the biggest threat is in terms of "price discovery".

While the NSE will remain the price setter till domestic Nifty futures turnover exceeds that of the SGX Nifty, if trading volumes converge, "it is likely that NSE could end up following prices set on a US dollar denominated instrument trading on an offshore exchange", implying that in the absence of reforms to make stock markets more competitive, trading in SGX Nifty futures is likely to overshadow its domestic counterpart.