)

Slowing discretionary demand and stricter norms on sourcing of its key input, gold, pulled down Titan Industries’s performance for the quarter ended September. The performance, however, is reasonable, given the external environment and restrictions on gold imports, etc. With the management indicating that gold sourcing issues would ease and given that it is focusing on profitable growth, the market was impressed.

Titan’s stock, which has lagged the Sensex in the last few months, jumped 4.2 per cent to Rs 266.30 on Thursday. It trades at 28.6 times FY14 estimated earnings, and most analysts remain positive on the company and believe it is best placed to gain from revival in discretionary demand.

“We believe Titan is well-equipped to brace the regulatory headwinds. It is sourcing gold from old jewellery, local refineries, copper mines (gold is a by-product) and State Bank of India (SBI)’s Gold Deposit Scheme. It is also evaluating the gold exports option to meet the 80/20 norm. Titan remains one of the best plays on discretionary consumption over longer term as it explores new under-penetrated high growth segments,” says Abneesh Roy, Consumer analyst at Edelweiss Securities.

Q2: Largely in-line

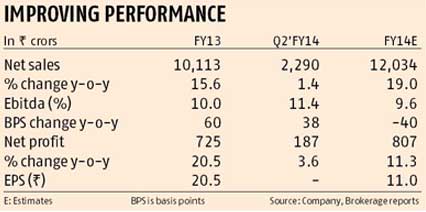

Though net sales, which grew 1.4 per cent year-on-year to Rs 2,290 crore, were short of Street expectations of Rs 2,535 crore, net profit at Rs 187 crore (up 3.6 per cent) was in line with expectations of Rs 190 crore.

To comply with RBI guidelines, Titan discontinued sale of gold coins from July 15. Adjusting for the same, total sales growth was at 8.4 per cent year-on-year, though still lower than consensus expectations of 12 per cent growth. Ebitda margin though came in higher at 11.4 per cent (up 38 basis points) against expectations of 10.3 per cent, aided by higher proportion of studded/diamond jewellery.

By the management, Dussehra sales were not very exciting. However, they have seen an improving trend in walk-ins since the past week and is hopeful of a pick-up on Dhanteras as well as the coming wedding season.

“Given the good monsoon across the country and a likely change in consumer sentiment, driven by stock market movement, we are hopeful of a good second half", says Bhaskar Bhat, managing director.

In line with the slowing demand, Titan has reduced the pace of store additions and is focusing on improving same-store sales growth. The new store additions will be calibrated with a higher focus on store profitability. However, it will not reduce advertising activities.

Jewellery segment revenues (contributed 75-80 per cent to topline and 80 per cent to profits) grew 4.3 per cent to Rs 1,798 crore. Though growth was below analysts’ expectations of eight-10 per cent, excluding gold coins, sales increased 13.6 per cent, helped by 10.4 per cent grammage growth. Studded jewellery growth remained strong, aiding segment margins, which expanded 93 basis points to 13.4 per cent.

The watches business was hit on multiple fronts, namely, slowing discretionary demand, higher input cost and unfavourable exchange movements, resulting in highest volume decline of 22 per cent (year-on-year) in the watches business. Consequently, this segment’s sales fell 6.2 per cent to Rs 442 crore. Price rises, however, helped restrict the contraction in Ebit (earnings before interest and tax) margin, the same fell 109 basis points year-on-year to 10.5 per cent in the quarter.

Though small, other businesses (eyewear, precision engineering and accessories) grew 17.2 per cent year-on-year to Rs 114 crore; this segment’s Ebit loss declined 94.2 per cent to Rs 25 lakh.

After stricter RBI norms around gold sourcing, Titan’s borrowings increased Rs 604 crore in the quarter to fund working capital needs of the jewellery business. This resulted in a 64 per cent surge in finance costs to Rs 20 crore. While the management remains confident on procuring gold supplies, the easing out of 80-20 scheme (domestic/export) is key to sustainable inventory levels. The company, which has received the go-ahead to import gold directly, expects to do so in the December quarter, which should ease sourcing issues.

A sharp rise in interest costs more than offsets higher other income (up 27.4 per cent to Rs 30 crore), restricting net profit growth to 3.6 per cent.