)

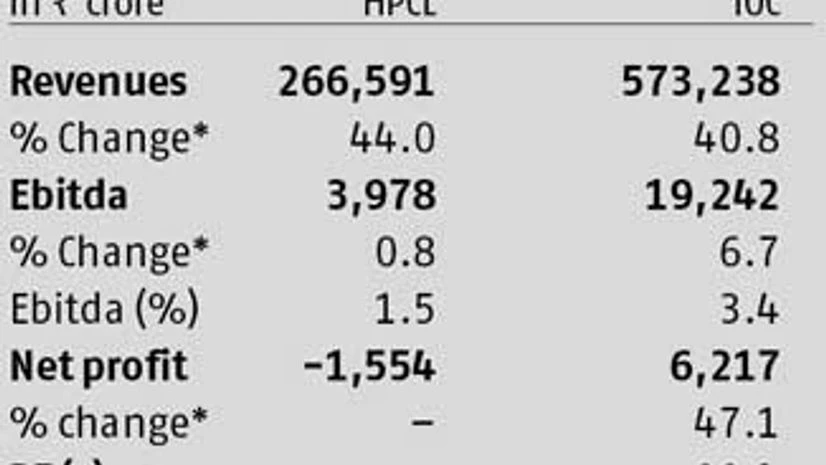

HPCL, IOC and BPCL respectively trade 23 per cent, 18 per cent and 15 per cent lower than their 52-week highs. HPCL has suffered the most, as it’s most sensitive to price reforms. While BPCL also lost heavily, it is sheltered to some extent by its exploration and production activity.

The prospects for HPCL and IOC will depend on faster oil pricing reforms, jeopardised by the government’s political compulsions. Thus, most analysts, of late, do not see much traction in these stocks, despite attractive valuations.

Slow reform an overhang

The government allowed oil marketing companies (OMCs) to raise diesel prices in small steps; thus, an initial one per cent rise on January 18 against the 20 per cent needed. After a rise each in January and February, the third one was skipped as the Budget session of Parliament was on. Political compulsions and the approaching general elections in FY14 raise doubts on the continuity of price increases at the desired pace.

Reacting to the current deferment of diesel price hikes, analysts at HSBC observe that “just after two increases, OMCs have taken a pause in March. This indicates that full deregulation of the diesel price is unlikely in the near term.” HSBC remains underweight on OMCs.

Analysts at IIFL observe: “We are currently factoring in only a Rs 4 a litre increase in diesel prices in the next year as against Rs 6 a litre if the price hikes continue at the current pace (12 rises of 50p each in the financial year). Even if the diesel price were hiked by Rs 6 in FY14, this would have led to under-recoveries for oil companies reducing by (only) Rs 36,000 crore, as for every rupee increase in diesel prices, the under-recoveries come down by Rs 6,000 crore.”

Further, raising the cap on subsidised LPG cylinder sales in a year from six to nine would increase subsidies further by Rs 9,700 crore.

There is, however, some benefit to OMCs on account of falling oil prices. Brent crude is down from $118 a barrel in February to $110 levels currently. However, analysts don’t see much decline from here on. Morgan Stanley analysts see Brent prices around $110 a barrel and the rupee at 54.5 to a dollar.

Sujit Lodha at Asian Market Securities does not see much downside in oil prices. Assuming Brent prices at $110 and the rupee at 53.5, he sees total under-recoveries for FY14 at Rs 110,000-120,000 crore. Though OMCs generally do not bear a major portion of the subsidy and the government does not allow OMCs to end the year in the red, a delay in reimbursement of subsidies by the government leads to increased working capital requirement and, hence, the interest outgo.

With subsidies on kerosene continuing and those on diesel not being reduced at a fast pace, analysts do not have a strong outlook for both HPCL and IOC