"Use rally to exit PSBs, say analysts")

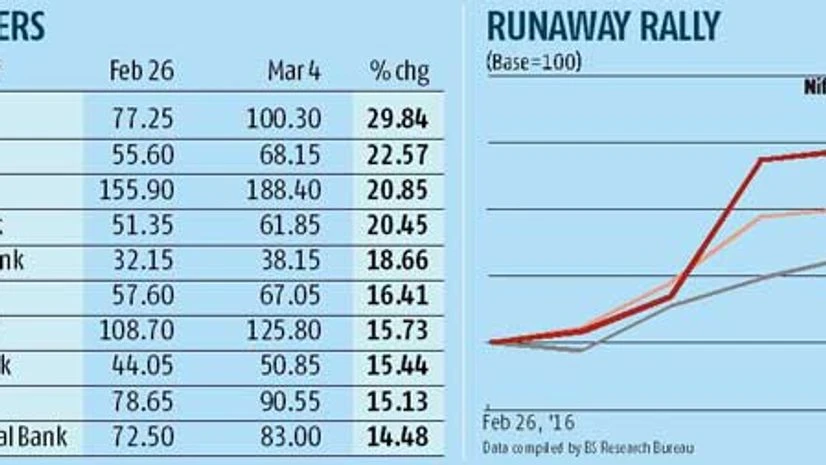

After touching a 52-week low of 13,407 in intra-day deals on February 29, the Nifty Bank index has bounced back nearly 13 per cent till date. The rally in the Nifty PSU Bank index has been even more spectacular with the index surging nearly 16 per cent during this period. By comparison, the Nifty 50 index has gained nearly eight per cent.

The rally comes on the back of a hope that the Reserve Bank of India (RBI) now has room to cut rates further, given that the Union Budget has stuck to its earlier fiscal deficit target of 3.5 per cent of the gross domestic product (GDP) for the next year.

Read more from our special coverage on "PUBLIC SECTOR BANKS"

Another key development, especially for the public sector banks (PSBs), has been the RBI's decision to alter capital adequacy rules allowing banks to count the value of their land holdings (at 55 per cent of current value, after revaluation) as part of Tier-I capital. That apart, foreign exchange reserves that arise from translation of foreign operations into rupees and deferred tax assets will be counted as Tier-I capital, subject to discounts.

The Budget, too, has provided Rs 25,000 crore to be pumped in as capital into PSBs. Though the figure is lower than the amount anticipated by the Street, it does provide some relief to weaker PSU banks. So, it this time to rejoice over a possible recovery in PSU banking counters?

Despite these measures, analysts believe that PSBs are not completely out of the woods. They still have to clean up their balance sheets and provide for non-performing assets (NPAs). Challenges will persist on the operational front, as their competitive prowess will be severely impacted, given the diversion towards clean-up coupled with capital constraints for growth.

Explains Nilesh Parikh of Edelweiss Securities in a co-authored report with Kunal Shah and Prakhar Agarwal: "This is a welcome move and positive for the banking system in general, more so for PSBs, which are already reeling under capital constraints. However, it must be followed up with effective steps on monetising non-core assets, which will reduce the imminent dilution risk at weak multiples for some of these banks, particularly small mid-sized PSBs."

Analysts thus still remain wary of making fresh investments in PSBs and suggest investors stay away from these stocks, at least for now.

Vaibhav Agrawal, vice-president, research - banking, at Angel Broking, on the contrary, says the upside in these stocks should be used to exit. "Overall, nothing much has changed for PSBs as regards their NPA situation. Even with the new RBI guidelines on Tier-I capital recognition, we are not too bullish on PSBs. While the money can be used for regulatory compliance, it does not improve the book value. What is required is equity capital, and this measure only takes away the urgent need to dilute at cheap valuations. It just gives more time to the banks and the markets to recover. Overall, I think it is a good time to exit these stocks," Agrawal says.

The downside risk, as some believe, is that the capital boosting option now available is an indication of the bad news likely to come in the form of March 2016 quarter results, wherein banks will have to fully disclose the quantum of bad loans on their books. These experts suggest that the capital boost from revaluation reserves will help banks to avoid further deterioration in their book values.

Dhananjay Sinha, head of institutional research at Emkay Global Financial Services, also believes that the recent rally in PSBs is purely on sentiment, and driven by rate cut hopes and the RBI's policy initiative as regards recognition norms for Tier-I capital.

There is another big risk that the market is perhaps ignoring. Short-term gilt yields have fallen, and may slip further, on hopes that the government has maintained fiscal discipline, which in turn will lead to sufficient liquidity and benign yields, thereby boosting banks' treasury incomes in the March and subsequent quarters. This might not materialise, however.

"I believe there is a high chance of slippage of as much as 50-100 basis points (a basis point is a hundredth of a percentage point) in the fiscal deficit. The markets have reacted to the headline number and have not read the fine print. I would definitely not buy into this PSB stock rally. While one can look at Axis Bank and ICICI Bank, I don't think one can consider PSU banks as a re-rating story just yet," Sinha of Emkay says.

"With most stressed metals assets recognised as NPAs in FY16 and limited exposure to infrastructure conglomerates, SBI remains our only Buy and preferred pick among PSBs," says Adarsh Parasrampuria and Amit Nanavati of Nomura in a recent sector review report. They recently downgraded Bank of Baroda to neutral, and maintain a neutral rating on Bank of India and Union Bank.