)

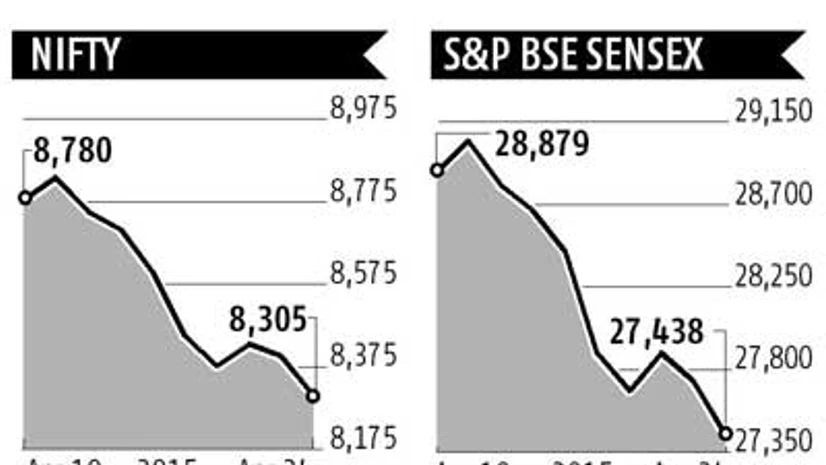

The stock markets continued their slide for the second consecutive week to end at 3-month lows on the back of worries regarding corporate earnings and fears of sub-par monsoons. The lingering tax uncertainties seem to have also dampened sentiment.

In the trading week ended April 24, the 30-share Sensex shed 1004.16 points or 3.53 per cent at 27,437.94 and the 50-share Nifty ended just above the 8,300 levels at 8,305, down 3.5 per cent.

In the broader markets, the BSE Mid-cap Index tumbled by 336.13 points or 3.12 per cent to settle at 10,435.64, while the Small-cap Index collapsed by 613.61 points or 5.28 per cent at 11,008.62. All the sectoral indices ended in the red for the week, with auto, banks, IT and metals indices slipping below their 100-days moving averages.

The benchmark Sensex, which was up as much as eight per cent at one point during the year (all-time closing high of 29,681.77 on January 29), has erased its entire calendar year gains. After two weeks of losses, the Sensex at its current value of 27,437.94 is slightly below 27,499.42, where it started the year.

A poor start to the fourth-quarter earnings season has rattled investors; the likes of Infosys, TCS and MindTree reported disappointing numbers, and RIL's results also failed to enthuse the market participants.

The Indian Meteorological Department has stated that monsoons could be below average in 2015 due to the El Nino effect. A below-average rainfall could be detrimental to the economy as agriculture, which employs around two-thirds of the population. Below-normal monsoons would also weigh on inflation, halting policy rate cuts by the RBI and thereby proving to be a dampener to growth.

Mr. Hitesh Agrawal - Head Research, Reliance Securities said, “The next week is expected to see a tug-of-war between the bears and the bulls. Many good quality companies across market-caps have witnessed a respectable correction making them ripe to be picked up by medium-to-long-term investors. As of now, 8,200 is an important strong support for the Nifty in our view. However, below this, a 250-300 points Nifty slide cannot be ruled out.”

Rupee

In the week ended April 24, the rupee ended the week at a three-and-a-half month low of 63.56 against the dollar on the back of month-end dollar demand and capital outflows from the equity markets.

It may be pointed out that the rupee was the third best performing currency in Asia in the March quarter, rising 0.85 per cent.

Sectors and stocks

The IT index led the loser’s pack on the BSE, registering a cut of 643.62 points or 5.7 per cent, on account of the disappointing March quarter numbers delivered by the IT heavyweights. In the IT space, Infosys dived by as much as 6 per cent on results day to end the week lower by 8.5 per cent at Rs 2184 on the back of a fall in profits and revenues on quarter-on-quarter basis;. Infosys disappointed with its fourth quarter numbers today.

The auto index tumbled by 850.99 points or 4.45 per cent at 18,262.01. In the auto space, M&M skid 4.4 per cent at Rs 1170.45, Tata Motors slipped 3.7 per cent at Rs 515.30 and Bajaj Auto shed 3.3 per cent at Rs 1996.85. In the auto-ancillaries space, Bosch nosedived by 14 per cent, while Apollo Tyres, Motherson Sumi and Exide shed between 7 per cent and 9 per cent each.

The oil and gas index slumped by 424.45 points or 4.33 per cent at 9,385.94. Index heavyweight RIL lost 5.1 per cent at Rs 879.40 despite reporting strong quarterly profits on the back of firm gross refining margins; ONGC, Petronet LNG and Oil India lost between 4 per cent and 9 per cent each.

The private sector lender ICICI Bank lost 0.64 per cent at Rs 308.10 and car manufacturer Maruti Suzuki shed 2.82 per cent at Rs 3539.80 ahead of their March quarter earnings to be announced on Monday.

Week ahead

Maruti Suzuki India, ICICI Bank, Idea Cellular, Bharti Airtel, Sesa Sterlite and HDFC are among the major companies scheduled to declare their numbers in the forthcoming week. Any earnings disappointments could drag the market further in the near term.

The movement of the rupee and foreign fund inflows will also dictate the trend on the bourses.

The April F&O expiry scheduled on Thursday would be an important factor in determining the near-term market trend.

There could be volatility ahead of expiry as the Nifty volatility index VIX has zoomed by 18.50% to 19.10 for the week ended April 24.

The market participants would also keenly watch developments on the GST front, given the fact that the bill has been introduced in the Lok Sabha.

On the other hand, there is a possibility of technical bounceback, given the fact that the technical indicators suggest that the markets are oversold at current levels. Moreover, the NSE could find support at its 200-day moving average of 8,250.

The markets would be shut for trading on Friday on account of May Day.